Macro Hopes Continue, But Fundamentals Are Setup to Slip

“Close your eyes and buy” seems to be the mantra for now. While fundamentals don’t justify a cyclical recovery in oil yet, the market continues to move higher. The primary driving force has been macro funds, index money and CTAs. Technicals and momentum have only added to it, and there is a sense from some of investors that they need to buy for fear of missing out. Also similar to 2015, we see a confirmation bias where any bullish data point is embraced (e.g. supply outages, weekly US production, etc) and bearish data points are dismissed or spun as a buying opportunity (i.e. the worse is behind us).

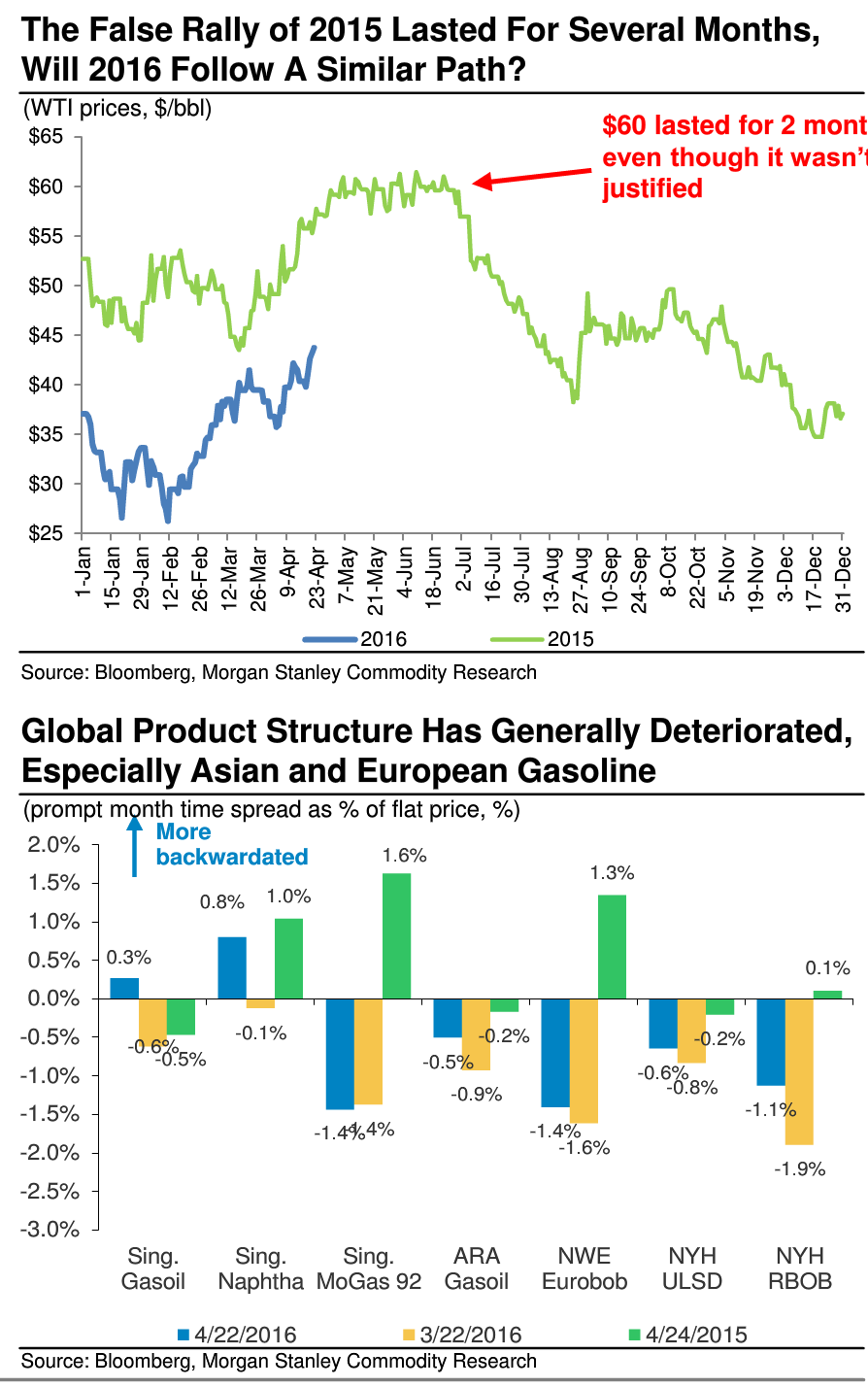

Non-fundamental rallies can last for several months before the physical market pushes back.

In 2015, the rally to $60 WTI lasted for over 2 months. Yet, unlike other assets, there is a physical market behind commodities. If prices move too early, there are real world implications, even if those facts are slow to play out. It’s one reason why expectations investing is less effective in commodities. Nothing happens until it happens.

Fundamentals are poor and set to deteriorate.

The macro/CTA players are mostly generalists and quants expressing a macro view. Yet, the market impact underscores how macro and technical oil trading is at the moment. The problem is that prices are approaching important fundamental levels, and the fundamental trends look worse.

A significant number of supply outages are set to resolve in the coming weeks/months.

OPEC production could rise nearly 1 mmb/d from Mar – June, and Doha’s failure could setup a market share war with many producers now calling for growth.

Prices above $45 WTI will start to impact the rate of decline in US supply and should attract much more producer hedging. We are also already seeing increased appetite for energy lending after this move – a reversal from Jan, which excited the market.

Gasoline trends in Asia look quite poor with tankers of product floating off Asia. EM ex. China oil demand has also been underwhelming, which is the key area of growth.

Near-term catalysts may be lacking, but a macro unwind could cause severe selling pressure. The extreme long spec positions from many of these funds could prove problematic. Realization of the MS economics and FX views could setup for an unwind in 2H16 given their sensitivity to macro trends.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.