Macquarie Bank has lifted its China steel production forecast from -1.3% to 0.4% today and with it comes some interesting insight into the Chinese steel short squeeze:

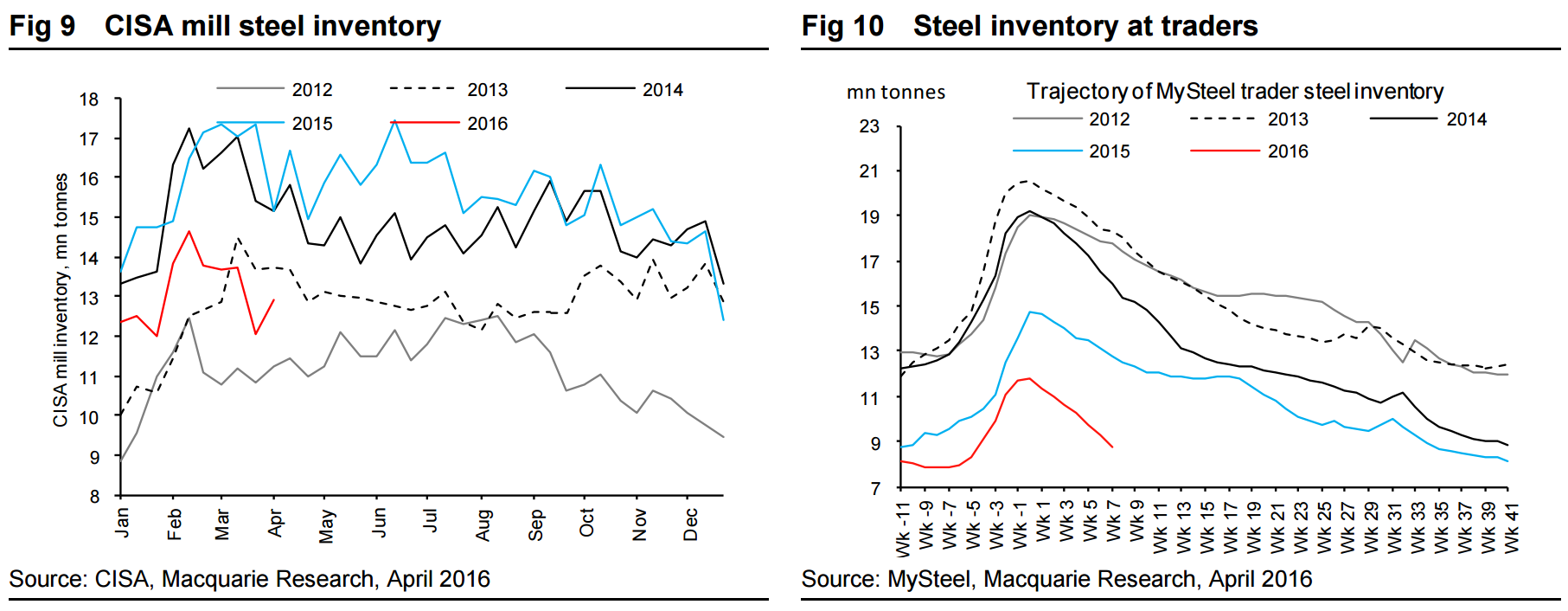

…on restocking, inventory still appears low at steel mills and steel traders (Figs 9 & 10), so restocking through the supply chain should add some extra demand in months ahead, but as liquidity conditions in the economy stop getting looser or even start to become tighter, demand from restocking will also fade at some point in 2H16.

Besides the sequential improvement in end-user demand, mills’ difficulties in resuming/increasing production has also been a reason for the price rally. The main problem seems to be continued financing difficulties at small steel mills after the severe losses they undertook in 2H15. That some blast furnaces have been idled for months has also made it technically harder to restart them. Finally, as a result of the horticultural exhibition held right now in Tangshan (the largest steel producing city in China with a capacity over 100mtpa), the local government there has also forced mills to idle some sinter and coke production lines, which will effectively cap production and tighten the northern Chinese market. Even on Tuesday, the local government in Hebei messaged that currently idle facilities would not be allowed to restart (which does feel like closing the door after the horse has bolted).

Therefore, mills seem to have been slower than in history in resuming production, and according to our survey, capacity utilisation still hasn’t reached historical peaks. This is why we find the NBS figure for crude steel production in March too high, which should imply a much higher capacity utilisation rate than our survey (and other surveys) suggest. As a result, we still see the potential for production to get higher in April, which would add downward pressure to spot prices.

Pretty much the MB view. Throw in the mad Chinese speculator and, voila, Straya fixed!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.