From the usually better Jessica Irvine:

Indeed, according to economist Saul Eslake, there are four main reasons not to worry about our foreign debt.

First, while the trillion dollar figure might sound significant, in reality, our net foreign debt has been growing more slowly in recent times. Many mining companies have been able to finance huge investments by raising new equity from shareholders or from their retained earnings.

Second, more of our debt today is written in Aussie dollars than in the 1980s when we worried about such things. All government debt is all written in Aussie dollars, of course, and an increasing share of corporate debt is too. That’s good because, in the event of a credit markets crash, we would only have to repay in Aussie dollars, not in US dollars which would be more expensive.

Third, more of our debt to foreigners is written over longer time periods than previously. One of the main risks in having debt is that you may need to get a new loan during a time of market volatility. Debts are written over a certain time period, leaving you vulnerable when it comes time to refinance.

The global financial crisis really highlighted how reliant our banks had become on borrowing in offshore wholesale funding markets. They have since reduced their offshore borrowings and finance an increasing share of their funding from deposits, leaving them less exposed.

The fourth reason to be less concerned about our foreign liabilities is the seldom noted but extraordinary phenomenon – unusual in all our history – that Australia has become a net owner of foreign equity. That means we own more foreign assets than they own of ours. That’s mostly due to our large and ever growing pool of superannuation money, much of which is invested directly offshore.

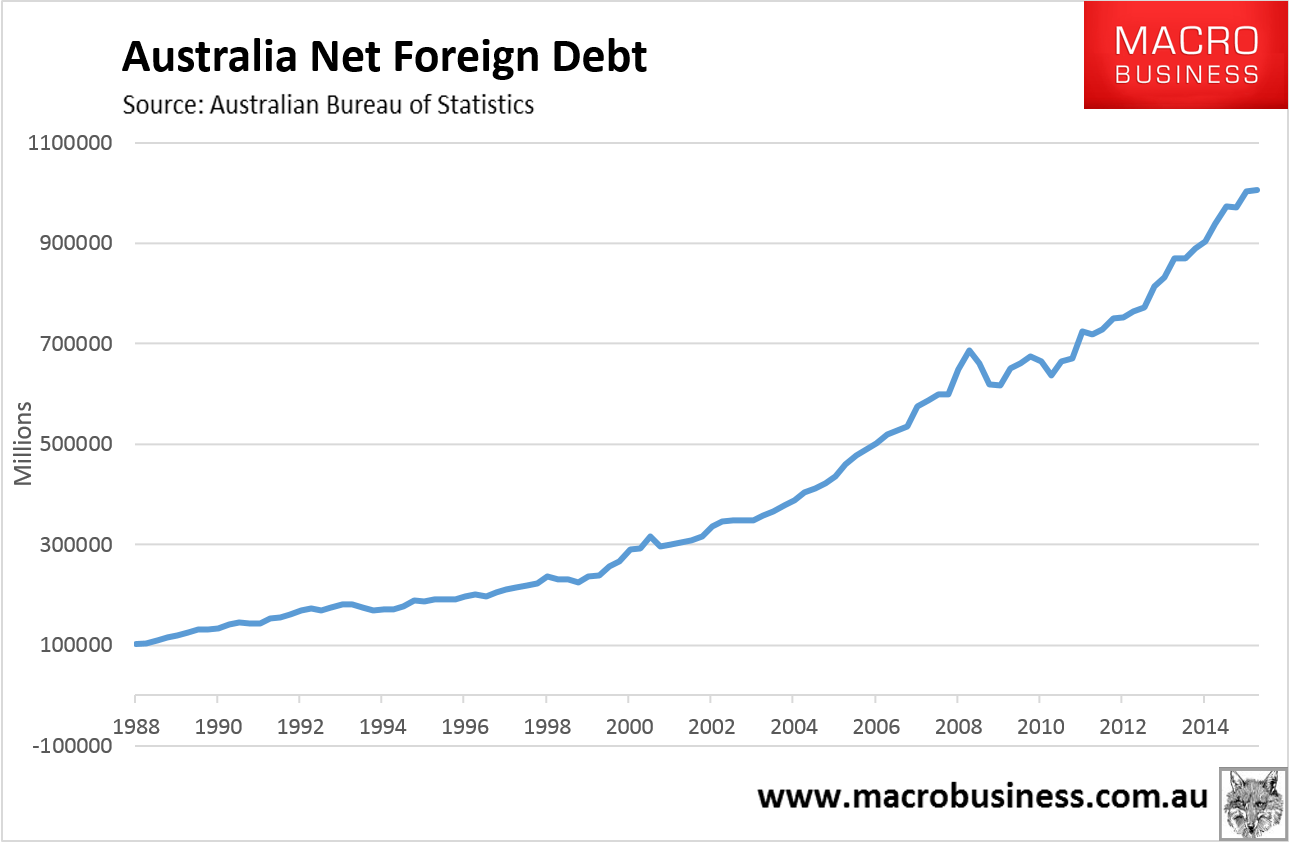

Deary me. First, foreign debt is not “growing more slowly”, indeed it is growing at its fastest rate in history:

Second, yes the debt is written in Australian dollars or, more precisely, swapped into Australian dollars. And that has allowed the borrowing to go on, and on, and on. But the act of swapping it is not free, it costs money, and that adds to the interest rate the banks charge as a result of the insured currency risk. All of that debt flowing in adds further upwards pressure to the exchange rate and you get Dutch Disease that hollows out your industrial base (think Holden and Arrium). As well, you can’t insure the liquidity risk except through implied guarantees from the national Budget if things freeze up overseas and that results in a severe constraint on public spending and massive moral hazard. In short, over time it chokes the incentives that underpin a healthy economy, overly concentrates your economy in services, standards of living fall with government services and governance itself becomes increasingly unstable.

Does anyone recognise Australia there?

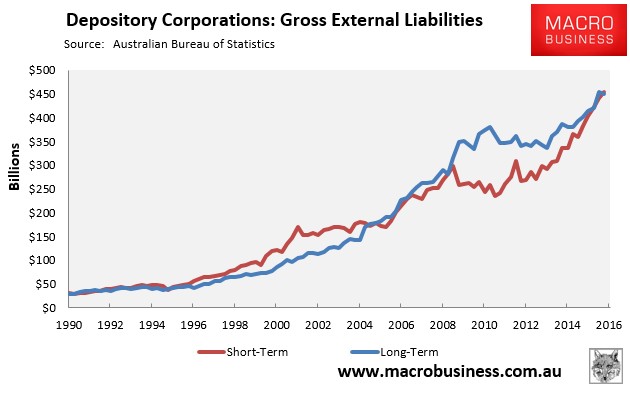

Third, yes, the funding profile of banks has improved since the GFC in the sense that it makes up a smaller proportion of overall borrowing but, as APRA warned just this week, the mix of that is still far too short-term oriented leaving us very vulnerable to the liquidity risk, not least because of the recent final dumb bubble blowoff:

Fourth, net foreign debt is “net” because it has already accounted for foreign assets. Double-counting does not reduce the risk. Gross foreign debt is a bowel-shaking $2 trillion. And if you think that that’s normal then go ask Canada, which has a similarly structured and sized economy, but only gross foreign debt of $600bn.

We might still decide to go ahead and run our economy like it’s a giant poker machine but let’s not kid ourselves that it’s normal, safe, sustainable or without cost.