The Bank for International Settlements (BIS) – the central banks’ central bank – has released a wonkish new working paper examining how bank capital affects the supply of new mortgages, drawing from evidence from a randomised control experiment using the mortgage market in Italy.

Below are the key extracts.

…the academic and policy debates currently center on the effects of bank capital on lending and risk-taking. Indeed, both macroprudential and the microprudential regulatory reforms propose to raise bank capital ratios and strengthen bank capital buffers, with the aim of preventing “excessive” lending growth and increasing the system’s resilience to adverse shocks…

Yet, there is only a limited degree of consensus on the effect of higher bank capital on lending… On the one hand, higher bank capital increases both the risk-bearing capacity of banks and incentives to screen and monitor borrowers, in this way boosting lending… On the other hand, as debt creates the right incentives for bankers to collect payments from borrowers, lower debt and higher capital may reduce banks’ lending and liquidity creation…

In this paper we study the effect of bank capital on banks’ propensity to grant mortgages and on their pricing. We also explore how bank capital affects the selection of borrowers and the characteristics of offered mortgages, deriving implications for risk-taking…

We focus on mortgages, whose relevance for both macroeconomics and financial stability has been unquestionable following the 2007-2008 financial crisis… Understanding how bank capital affects mortgage originations and the way banks select the risk profiles of borrowers is thus critical to evaluate developments in the mortgage market and the potential accumulation of both idiosyncratic and systemic risks…

Results:

…banks with higher capital ratios are more likely to accept a mortgage application. The effect is economically significant: a one percentage point increase in the capital ratio raises the likelihood of acceptance by about 20 percentage points, ceteris paribus…

…banks with a higher regulatory capital ratio are more likely to approve a mortgage application. In particular, a one percentage point increase in the regulatory capital ratio increases the likelihood of acceptance by about 10 percentage points, ceteris paribus…

Differently from other studies that found that liquidity and cost of funding are the main variables driving the banks’ decision to accept an application, our paper points to bank capital as the leading variable affecting it. In our sample period, liquidity is abundant and conditions on wholesale markets are not tense, so neither the liquidity position, nor the relative importance of wholesale and retail funding appear as key drivers of credit supply…

Overall, these findings indicate that on average banks are less likely to grant a mortgage to borrowers more exposed to negative shocks to their income, which make them more likely to default. Banks try to reduce default risk also by selecting mortgages that are smaller and faster to repay…

The bank capital (either the simple leverage ratio or the regulatory capital ratio) has a negative and statistically significant coefficient if bank controls and bank fixed effects are included (Columns 2 and 4). The effect is economically significant: a one percentage point higher capital ratio leads to a 29 basis points lower offered APR…

Overall, our results show that banks with lower capital ratio are less willing to take risk in the mortgage market. Their acceptance and pricing strategy is oriented to select borrowers that have a lower risk of getting into arrears and, possibly, default. This finding is consistent with the view that capital is a determinant of the risk bearing capacity of banks…

Conclusion:

On the one hand, we find that banks with higher capital ratios are more likely to accept mortgage applications and to offer lower APRs. On the other hand, banks with lower capital ratios accept less risky borrowers. However, we cannot rule out that less well-capitalized banks take more risk on other assets (business loans, securities).

We also provide a quantitative estimate of the effect of bank capital ratio on the supply of mortgages, using a nonparametric approach. We find that the capital ratio has a non-linear effect on the probability of acceptance, stronger at low values of the ratio, almost zero for higher values. This non-linearity is more pronounced when the borrower or the contract are riskier.

So, according to this study, banks with higher levels of capital are more likely to approve mortgages and extend credit than those with lower levels of capital.

The result seems fairly obvious since those banks with higher capital also have more headroom (regulatory capacity) to lend, whereas those with lower levels of capital have already exhausted their capacity.

The bigger issue that is unfortunately not discussed directly in the paper is the impact on systemic mortgage supply of raising the overall minimum level of required capital.

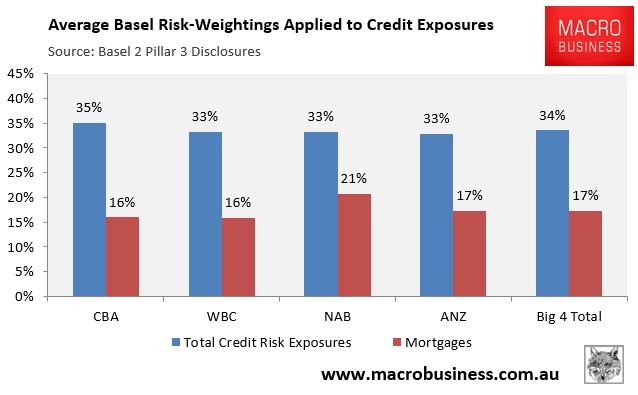

In Australia’s case, we know that following the recommendations of the Murray Financial System Inquiry, APRA announced an increase in capital requirements for Australian residential mortgage exposures under the Internal Ratings-Based (IRB) approach used by the big four banks and Macquarie.

From later this year, the average risk weight of residential mortgage exposures using the IRB approach is to increase to at least 25% from an average of around 17% currently (se next chart).

Logically, at least, this increase in the regulatory capital floor should reduce the amount of funds that Australia’s banks can lend towards housing (off a given capital base) by reducing average leverage against the big banks’ mortgage books to 40 times capital versus 72 times currectly.

unconventionaleconomist@hotmail.com