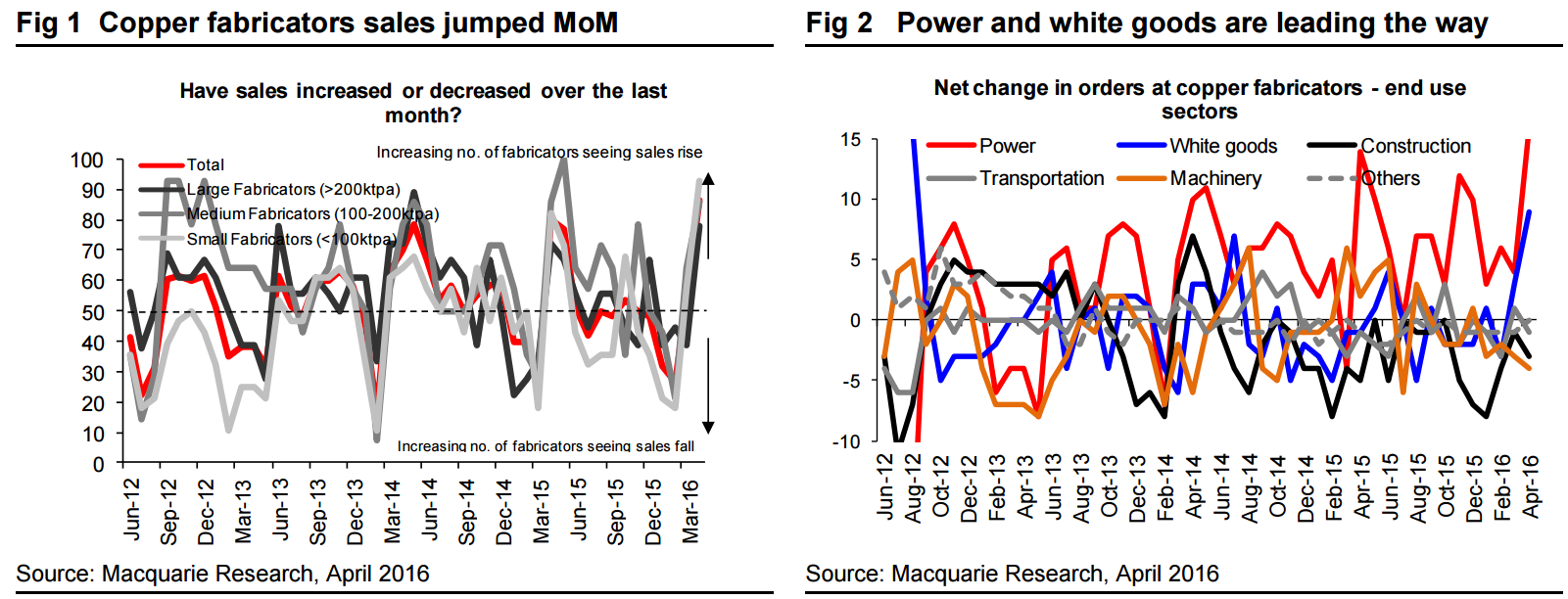

Our latest China copper survey pointed to a better demand picture: Orders from downstream industries increased clearly for both copper fabricators and traders, led by the power and white goods sector, fabricators lifted their capacity utilisation rate and sentiment over the industry chain remains positive. However end-user demand improvement has not yet fully fed into smelter orders, which were mixed and fabricator operating rates are still lower than same period last year. We also noticed traders reported sustained copper financing activity and export orders for certain larger smelters gained.

End-user orders picked up strongly MoM for the second month: Copper fabricators in our survey reported clear growth in their sales over the last month, including both wire/cable producers and plate/pipe producers, and the MoM expansion was even stronger than last April. By sector we saw continued positive growth from the power and white goods sectors, while machinery and construction continued to lag. Unlike steel where demand from the construction sector outperformed others, for copper the lack of demand driver from this sector could be due to a soft floor space completion in the property sector, given copper is mainly used in the mid and late periods of construction. According to the latest NBS data, 1Q China completed floor area (real estate) increased by 17.7% YoY, but all the growth happened in the first two months and March completed floor space declined by 1.9% YoY with a volume even lower than the Jan-Feb average.

Sentiment over copper market remains positive across the industry chain: Short term sentiment over the copper market has stayed positive in our survey, though there was a dip in the fabricators’ sentiment index. Copper prices climbed over early March, the domestic premium has improved since late March and became positive last week, and SHFE copper inventory has been falling for four weeks, plus an outlook for a firmer oil price and a softer USD index, all these contributed to the positive views over three months copper market (a similar trend can be seen on the average sentiment in China on commodities (Fig.20)). However, we should note that there remain some near-term risks for copper, i.e. China inventory remains high, supply increase is still a concern and there is an uncertainty on the sustainability of strong China macro data, as suggested by the pullback in metals prices after the release of 1Q data.

Copper is only up 8% from its lows versus 58% for steel and 68% for iron ore. The reason is twofold:

copper is less though still significantly exposed to building stimulus, and

most importantly, it has high inventories.

Copper’s small rise is a warning of the big pull back to come in iron ore and steel.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.