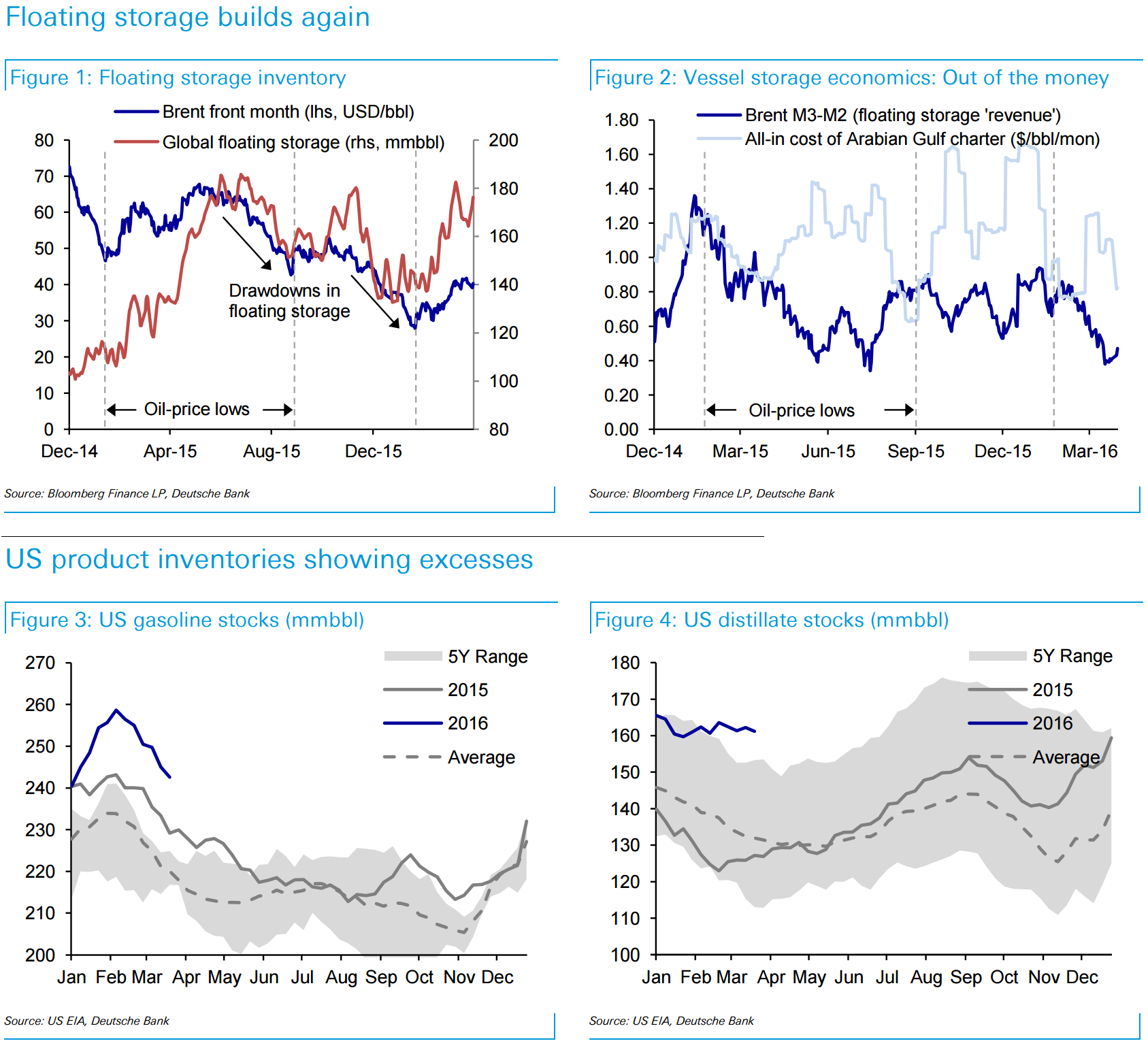

Since writing last week about an impending drawdown in floating storage which would pressure Brent prices lower, front month Brent has fallen by -6.3% (USD -2.6/bbl). However this has had nothing to do with floating storage as the Bloomberg estimate of floating storage inventory has actually grown by 10.5 mmbbl. This would have removed 1.5 mmb/d from the market for a one week period. So it appears that the build phase of floating storage triggered by the arbitrage in the first half of February is not quite over. However since the previous build phase lasted six weeks, the current phase is looking mature so we would hold to the expectation of a drawdown over the next three months, given that the arb economics remain unattractive. Note that Bloomberg floating storage estimates include both short-term floating storage as well as semi-permanent floating storage which the IEA estimates at 60 mmbbl. This less flexible volume located in Singapore, the Arabian Gulf, Caspian Sea and Arctic is used for the building and breaking of bulk for combining or splitting of shipments for resale. This still leaves a potential 116 mmbl which may be short-term in nature, Figure 1.

In the US, commercial crude inventories are trending slightly below our expectations, and we still see little likelihood of reaching a capacity crunch this year as utilization running at 73% currently should only rise to 79% at most by the May peak in inventory. For product inventories, the emerging trend of the year is for gasoline and distillate stocks to begin showing significant excesses above their historical ranges whereas last year, this was only evident for crude oil stocks. For us this suggests that we are still some way from what might be regarded as normal fundamental parameters. These excess inventories may be sustained for some time as the global market remains in surplus, but are likely to fall gradually as global market surpluses turn into deficits either by the latter half of 2017 or into 2018. More positively for the market, US product supplied figures remained relatively strong in the past two weeks. Growth in product supplied this year has now gone from consistently negative year-on-year comparisons in January and February to strong growth in March. This means that taking the first quarter as a whole, product demand is simply flat year on year. Given that we regard product supplied as a better predictor of final oil demand than refinery net inputs, this gives a bit more confidence around our 2016 assumption that US oil demand will be flat year on year (rather than down).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.