Reserve Bank Governor of New Zealand Graeme Wheeler earns $600k per annum. But that’s only in kiwi dollars. If he replaced Glenn Stevens he’d virtually double his salary. That’s got to be tempting even for a Bledisloe Cup tragic.

And we need him really badly. The mooted successor to Glenn Stevens is Phil Lowe who, despite an excellent intellectual reputation and history of sticking it to ‘the man’, has given zero indication that he’ll break with RBA “lying our way to prosperity” bubble management.

If you want to know why we should pay Graeme Wheeler whatever he wants to take the RBA job then consider today’s cash rate release which is so refreshingly honest that it brings a tear to the eye:

The Reserve Bank today reduced the Official Cash Rate (OCR) by 25 basis points to 2.25 percent.

The outlook for global growth has deteriorated since the December Monetary Policy Statement, due to weaker growth in China and other emerging markets, and slower growth in Europe. This is despite extraordinary monetary accommodation, and further declines in interest rates in several countries. Financial market volatility has increased, reflected in higher credit spreads. Commodity prices remain low.

Domestically, the dairy sector faces difficult challenges, but domestic growth is expected to be supported by strong inward migration, tourism, a pipeline of construction activity and accommodative monetary policy.

The trade-weighted exchange rate is more than 4 percent higher than projected in December, and a decline would be appropriate given the weakness in export prices.

House price inflation in Auckland has moderated in recent months, but house prices remain at high levels and additional housing supply is needed. Housing market pressures have been building in some other regions.

There are many risks to the outlook. Internationally, these are to the downside and relate to the prospects for global growth, particularly around China, and the outlook for global financial markets. The main domestic risks relate to weakness in the dairy sector, the decline in inflation expectations, the possibility of continued high net immigration, and pressures in the housing market.

Headline inflation remains low, mostly due to continued falls in prices for fuel and other imports. Annual core inflation, which excludes the effects of transitory price movements, is higher, at 1.6 percent.

While long-run inflation expectations are well-anchored at 2 percent, there has been a material decline in a range of inflation expectations measures. This is a concern because it increases the risk that the decline in expectations becomes self-fulfilling and subdues future inflation outcomes. Headline inflation is expected to move higher over 2016, but take longer to reach the target range.

Monetary policy will continue to be accommodative. Further policy easing may be required to ensure that future average inflation settles near the middle of the target range. We will continue to watch closely the emerging flow of economic data.

Advertisement

Next, have a leaf through the accompanying document and you find all sort of stuff that in Australia is swept under bureaucratic carpets in the name of ‘kicking the can’. On China:

Economic growth in New Zealand’s trading partners slowed to an estimated annual rate of 3.5 percent over 2015. This rate was much weaker than expected a year earlier. Forecasts for 2016 growth have also deteriorated substantially over the past year (figure 3.6). The slowdown has been broad-based across New Zealand’s trading partners, despite more accommodative current and expected monetary policy setting

…Growth in the Chinese economy is projected to moderate gradually, with conditions in the industrial and real estate sectors unlikely to improve quickly. The risk of a sharp slowdown in Chinese growth remains elevated, and as noted above is a key focus for financial markets. Concerns are centred on a rapid build-up in corporate debt (which is likely to continue as credit growth outpaces nominal GDP growth), ongoing capital outflows and downward pressure on the renminbi, and the need for structural reform. Any sharp slowing in Chinese growth could have significant implications for global growth, and for the Asia-Pacific region especially. This is important for New Zealand, given that the Asia-Pacific region accounts for most of New Zealand’s exports. Weak external demand is already weighing on growth in New Zealand’s Asian trading partners. If China and Japan are excluded, growth in Asia has slowed substantially over 2015, from an annual rate of 3.9 percent in the December 2014 quarter to 3.3 percent in the December 2015 quarter.

Perfect and no bullish balderdash.

Advertisement

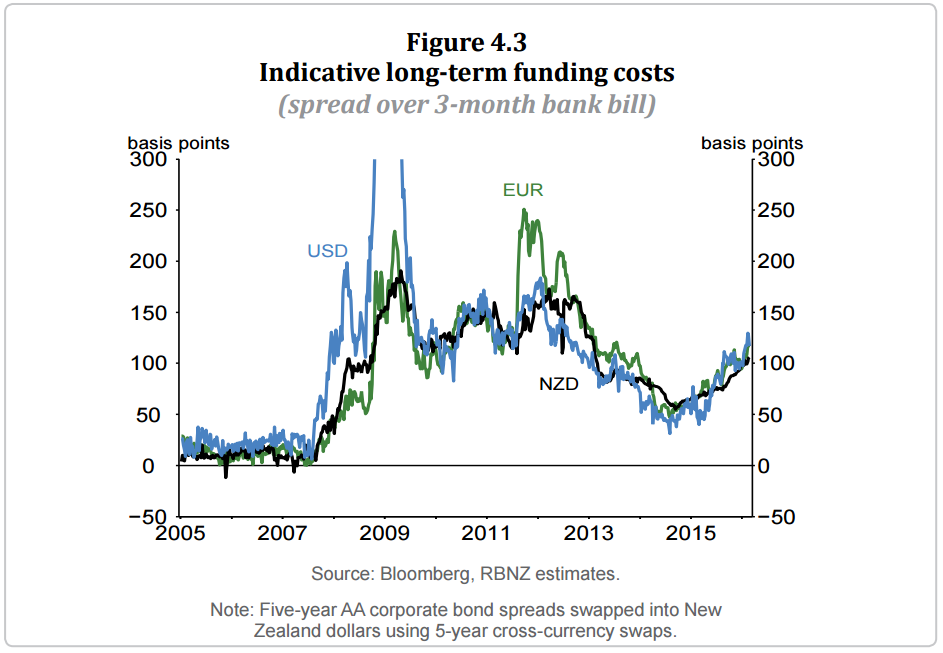

There’s realism about wholesale funding costs:

While indicators suggest short-term funding has become modestly cheaper for New Zealand banks in 2016, the cost of funding through longer-term wholesale borrowing has risen with the pick-up in financial market volatility (figure 4.3). The increase in longer-term wholesale costs this year adds to the increasing trend since mid-2014, which reflects a mix of global regulatory changes, concerns about commodity markets and emerging economies, and broader financial sector risks. To date, strong domestic deposit growth has limited the need for New Zealand banks to borrow at these higher rates. However, acceleration in credit growth over the past year might increase banks’ reliance on higher-cost long-term wholesale funding, leading to higher New Zealand mortgage rates. Moreover, continued financial market volatility may contribute to further increases in funding costs.

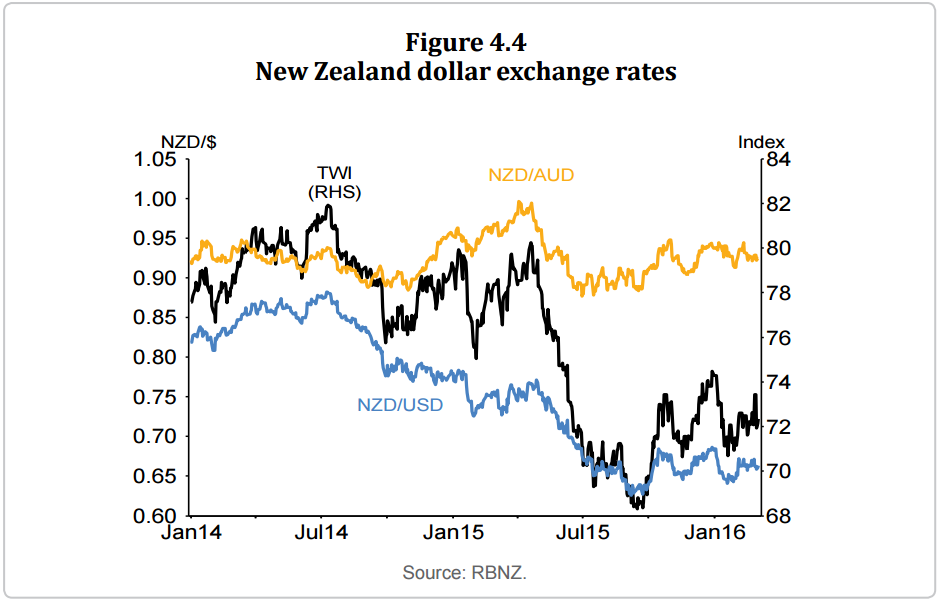

Realism about the NZ dollar:

The downward momentum in the New Zealand dollar exchange rate has faded in the past six months. The New Zealand dollar trade weighted index (TWI) fell from nearly 82 in mid-2014 to a low of 68 in September 2015, but has strengthened 6 percent to around 72 (figure 4.4). The TWI currently is around 4 percent higher than forecast at the December Statement. Despite increased global risk aversion and lower world dairy prices, there has been upward pressure on the New Zealand dollar exchange rate due to an expectation that international monetary policy will be more stimulatory than previously expected.

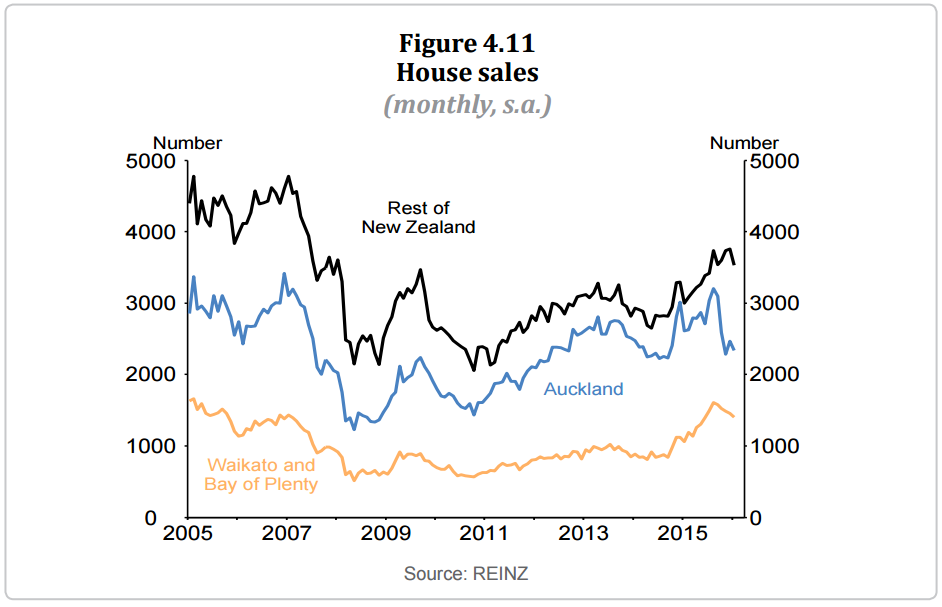

Realism in the use of macroprudential:

High net immigration, combined with limited housing supply in the Auckland region and low interest rates, has supported increases in house prices. House price inflation has slowed following the introduction of tax policy measures and macro-prudential policy measures applying to investor lending in the final quarter of 2015. The slowing in house price inflation has mainly been concentrated in Auckland, but has also occurred to some extent in the Waikato. House sales have fallen in Auckland and some surrounding regions, but have remained relatively stable across the rest of New Zealand (figure 4.11). It is too early to tell whether this moderation in house price inflation will be sustained.

And house price projections to make a specufestor quiver despite the boom:

Advertisement

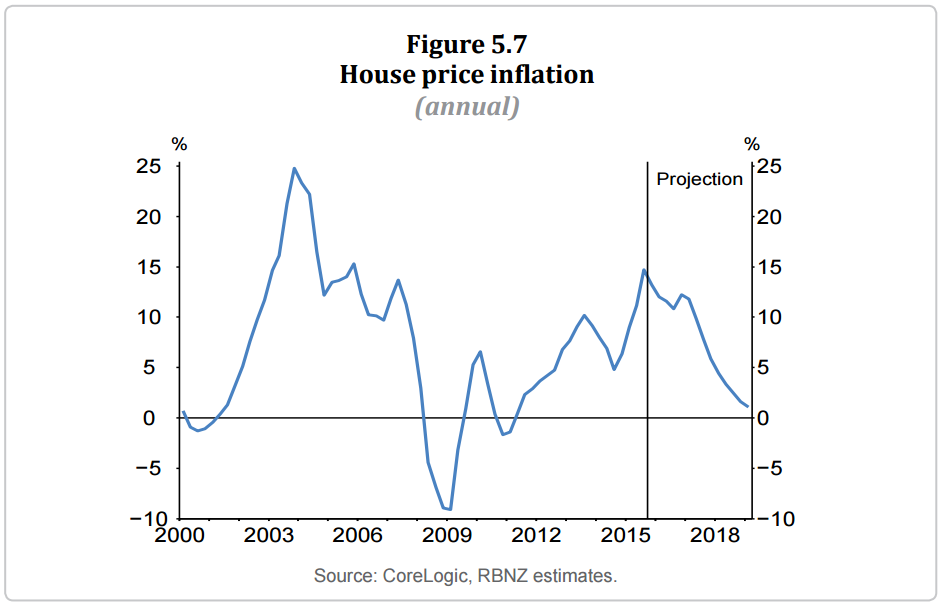

House price inflation is projected to remain elevated over the next 18 months, reflecting high net immigration, a shortage of supply in Auckland, and low mortgage interest rates (figure 5.7). Over the remainder of the projection, house price inflation slows as net immigration falls, affordability constraints bite, and increasing residential construction begins to address housing shortages.

And of course Wheeler has led the bank into a broader discussion about supply side reform to prevent house prices from hollowing out the economy on an ongoing basis putting a lot of pressure on fiscal authorities to respond.

Is the RBNZ operating in the same paradigm as the RBA? Yes. But it’s central banking without the rent-seeker bullshit. Alas, that probably means Mr Wheeler wouldn’t take the bribe.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.