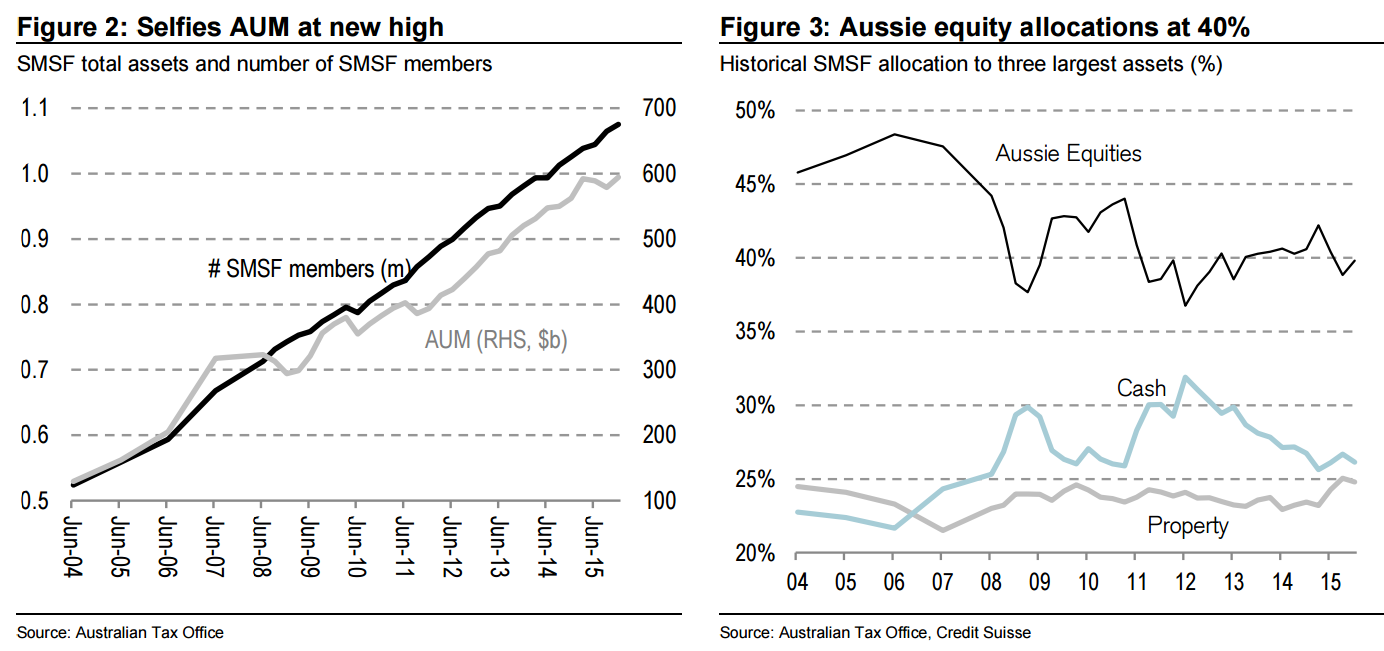

There are 1.08m SMSF members (Selfies) in Australia that manage 552k funds according to the Australian Tax office as of the end of December 2015. Selfies control AUM of $595bn which is a new high and is equivalent to 29% of Australian Superannuation assets. They held $562bn (29%) as of December 2014. Figure 2: Selfies AUM at new high Figure 3: Aussie equity allocations at 40% SMSF total assets and number of SMSF members Historical SMSF allocation to three largest assets (%) Source: Australian Tax Office Source: Australian Tax Office, Credit Suisse Selfies remain concentrated in three assets—Australian equities, Australian cash and Australian property. Aussie equities make up 39% (A$237bn) of Selfies current portfolio. We estimate Selfies own around 17% of the Aussie equity market. The equity allocation recently peaked, when the market peaked, in the March-15 quarter at more than 42%. The second biggest asset Selfies hold is Aussie cash, 26% of AUM (A$155bn). The cash allocation has been trending lower over the last few years but has not crossed below 25%. The last time Selfies held less than a quarter of their assets in cash was before the global financial crisis. It is clear that Selfies didn’t hold enough cash going into the financial crisis, but they could be holding too much after the brutal event. Finally, Selfies hold 25% of their AUM in Australian property (A$147bn). The property allocation has changed little for much of the last 10 years.

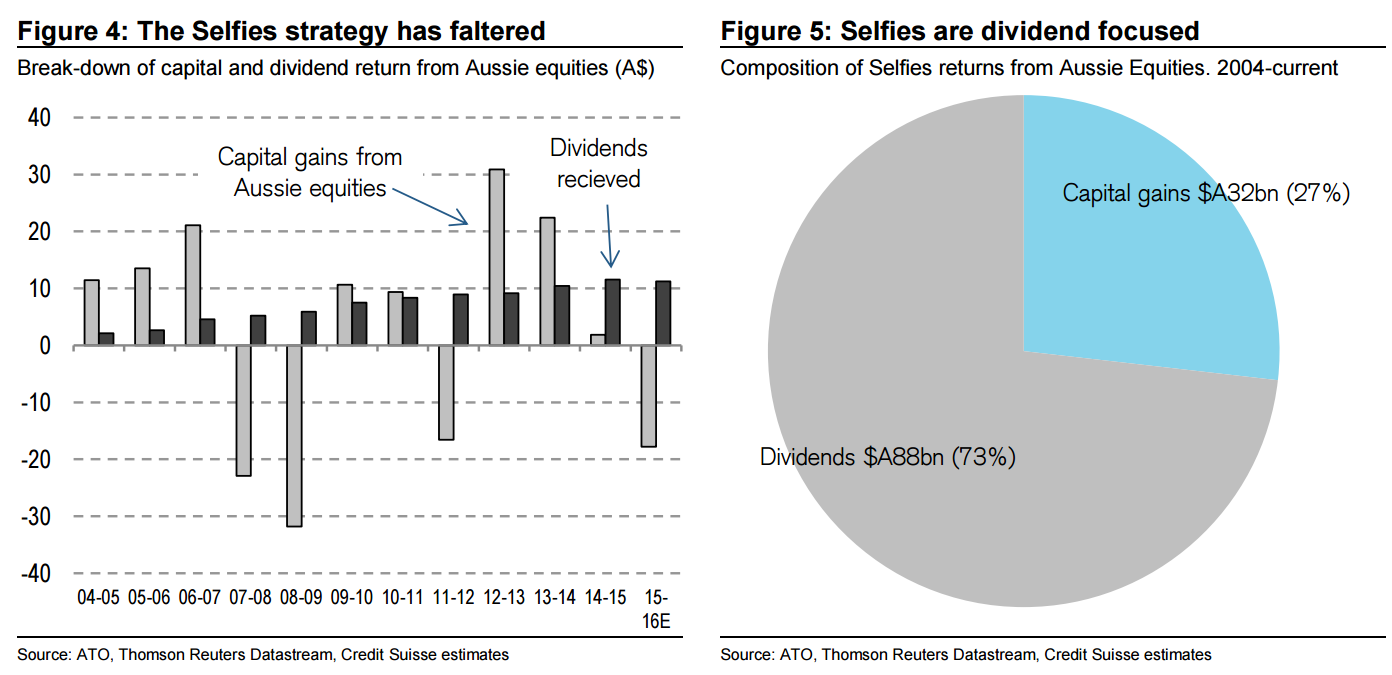

Selfies in the share market are after just one thing it seems and it ain’t capital growth:

CS notes that:

Advertisement

There have been two types of bear markets in Australia over the last 40 years. The less common has been the Grizzly Bear. After the initial 20% decline stock indices continue to fall another 20% over the next 12 months. The common bear market has been the Gummy Bear. After the initial 20% decline markets have risen over the next 12 months. The gain after these more benign bear markets—Gummy Rallies—has averaged 24%. We have noted that sector performance during previous Gummy Rallies has not been consistent. Leadership has often changed and it has not always been those sectors that underperformed the most during the bear phase. However, over the last three Gummy Rally’s we find buying high dividend yield stocks and selling low yielders, within each sector, delivered positive returns (Figure 4). Perhaps fueling the performance of this strategy is lower risk free rates. Government bond yields usually fall during bear markets and provide less competition for high yielding stocks.

My own view is that this is the Grizzly kind and if so the dividends and capital gains are going to take heat…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.