The bottom callers are rampant. From the AFR:

“It does look a lot more like the Titanic settling on the bottom,” is the neat summation by Mark Wills, head of investment solutions at State Street Global Advisors.

…what we did learn last weekend is that the Chinese government is prepared to stand behind the economy and spend as needed to keep things from getting too bad. Whether that adds to longer-term risks around the sustainability of the country’s massive debt pile is tomorrow’s problem, and not one increasingly short-sighted markets are likely to dwell on.

In the absence of real fundamental change, what the past couple of weeks does show is how far commodities markets were stretched, to the degree where speculative positioning was dominant in an environment where the longer-term money had stopped buying long ago. So what we are seeing is the flip-side of the steep selling at the beginning of the year.

…But if Fed chair Janet Yellen signifies a slower path of monetary tightening, that will go a long way to taking the upward pressure off the greenback, which is also good for US dollar-denominated commodities.

Add that to the mix and we can get more confident the resources Titanic has, indeed, found the ocean floor. What will refloat it is another question altogether.

And more from that cheerful paper:

Ben Jarman, a senior economist at JPMorgan…says the negative story about the falling terms of trade and the associated collapse in mining investment is starting to look “quite long in the tooth”, Eventually, a bottom will be reached, he suggests. When a company stops spending money on new investment after a big increase, the fall-off or “subtraction” shows up as a negative in GDP. Eventually that effect wears off.

In the meantime, the rest of the country has made a good fist of getting on with life.

To support his case, Jarman points to signs that overall labour income declines have bottomed out. The logic behind this is that while individual households may be suffering from lower wages growth, the economy as a whole has produced more jobs than was expected. This has resulted in an aggregate increase in overall income. Some might be suffering, but more have jobs and a pay-check.

The consequences of this better-than-expected reality, if you believe it, can be seen in many places. Property construction is booming, particularly in NSW and Victoria, which have taken over from WA and Queensland as the nation’s economic powerhouses. Household spending has been the surprise factor in the recent fourth-quarter national accounts, which showed the overall economy grew by the most in almost two years.

Moody’s Investor Service, the ratings agency, this week said last year’s 2.5 per cent GDP growth was stronger than it had predicted, and demonstrated the nation’s resilience to external shocks. That’s all good news for the AAA rating – for now.

For the Reserve Bank of Australia none of this is news. It’s been trying to promote a more positive rendition of the economic story for some time. The evidence, perhaps, may finally be starting to swing behind it.

MB remains of the view that this is not the bottom. Here is why:

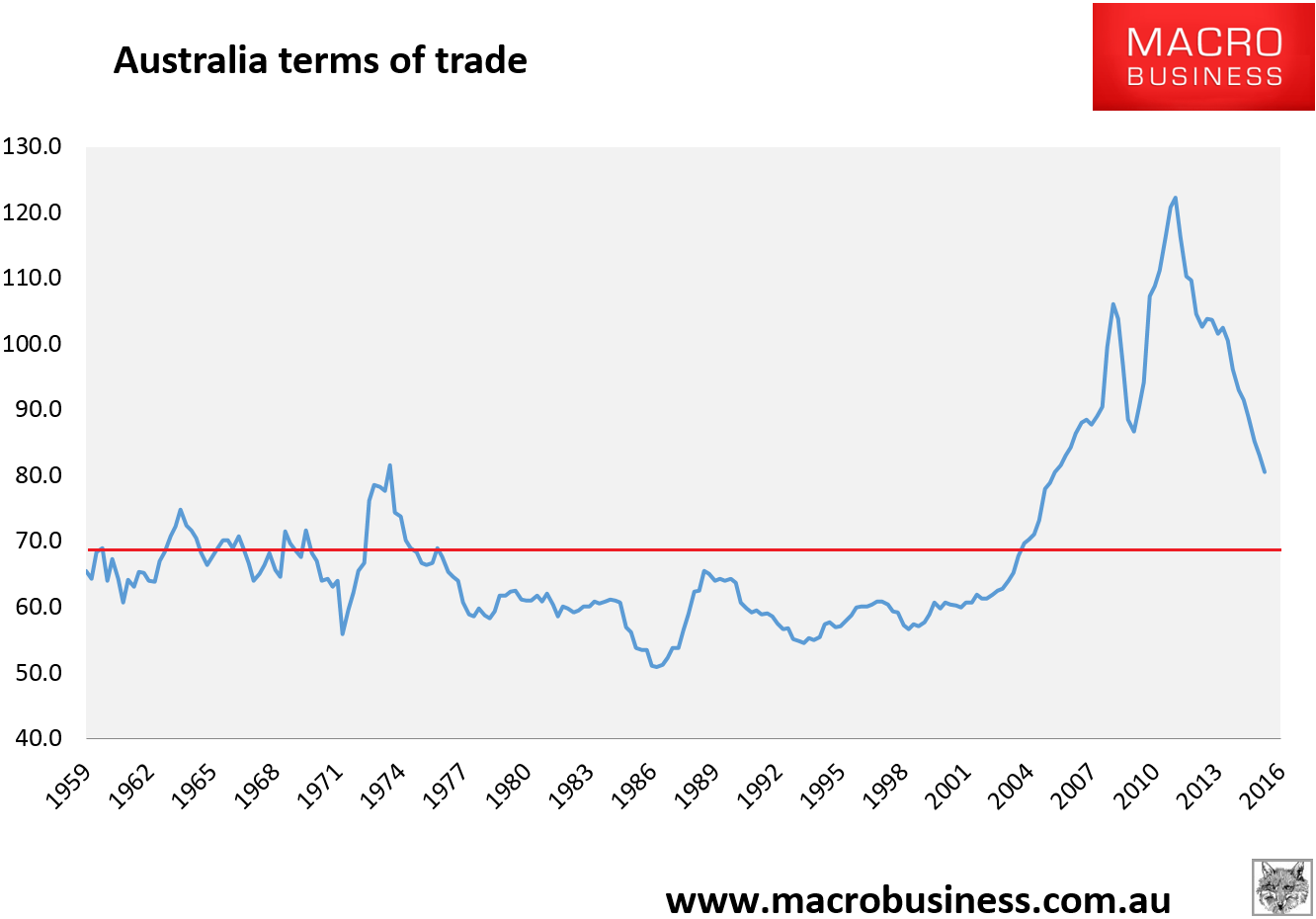

Australia’s terms of trade are currently equal with their highest pre-China boom level in history. Does it really make good sense to assume that they will settle here?

The average over 66 years is 69 points (marked in red) 14% below the current levels. But booms are always followed by downside overshoots to clear oversupply so we’re very likely to head right down into the 50-60 range. If the bottom is eventually 55 then that’s another 31% drop. The drop so far has been 34% so there’s plenty more pain ahead for income. If you doubt it then just consider:

- there are three more years of expanding iron ore supply as Chinese demand falls away and it will not bottom until $20 or so;

- coking coal falls with it and will not bottom until $60 or so;

- thermal coal is in structural decline and will not bottom until $30 or so;

- LNG faces the largest glut since iron ore for another 5-8 years and will not bottom until it’s $3 or so.

That’s over half of Australia’s terms of trade set to keep falling for years yet.

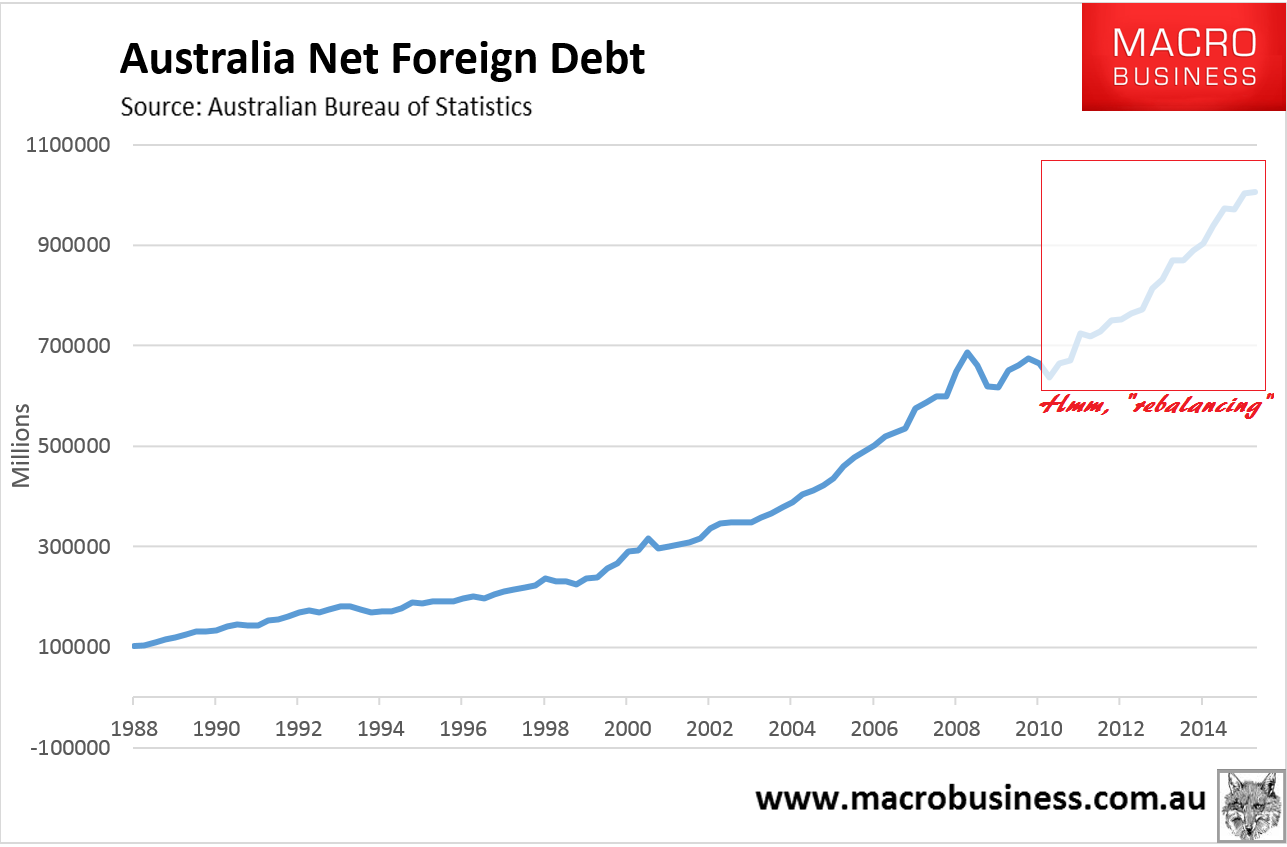

As for rebalancing, yes, there’s the eastern property bubble which has generated reasonable employment growth somewhere below the ABS numberwang figure. But it is entirely and massively offshore debt-funded for both private and public expansions:

Net external debt is rising at its fastest rate in history and looks rather more like it should be called the Australian “imbalancing”.

Authorities know this even though they lie constantly to cover it up. This, fundamentally, is why MB won the battle for macroprudential tools to be imposed. It’s why various governments keep committing suicide trying to find ways to balance the Federal Budget. The debt ramp up can’t go on for much longer for households lest ratings agencies downgrade the banks, nor for the government lest ratings agencies downgrade the sovereign and then the banks owing to the offshore funding guarantee.

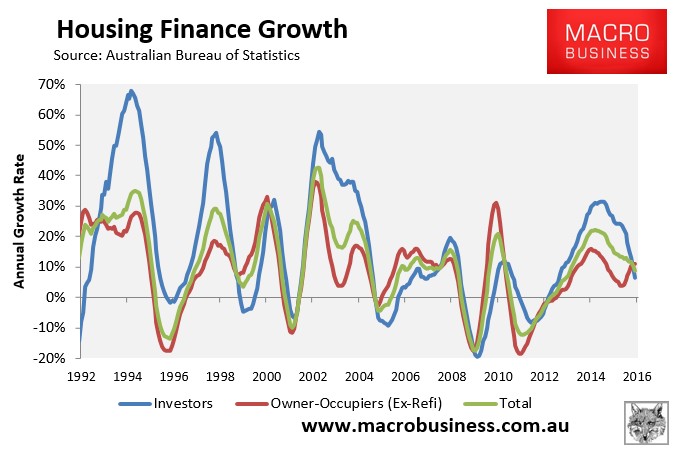

As a result, the great “imbalancing” is about to slow. The major driver of the offshore credit binge is mortgages and growth is coming off fast:

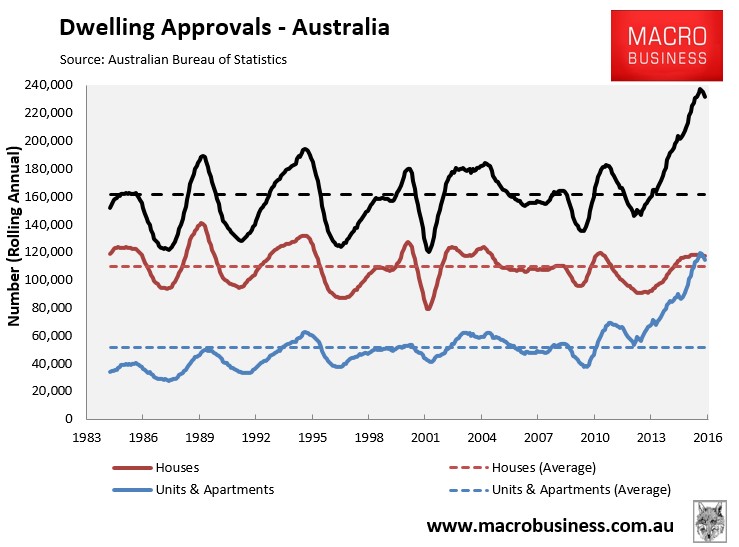

House prices are stalling and falling even if headline metrics disguise it to an extent. It is clearly set to get worse. Moreover, the construction booms that have directly offset job losses in mining by shifting labour from major engineering projects to residential building is also on the backside of the boom which is why we are seeing all sorts of warnings about “apartment busts”:

This slowing in credit is a good thing but it also means that growth will decelerate. Residential construction contributed 0.6% to GDP last year and that is not only going to fall to zero but subtract from GDP as the boom comes off, along with the ongoing mining and car industry capex busts. It is a pretty good bet that consumption is also going to taper as uncertainty rises with these forces and a toxic election upsets the apple cart. The labour market is going to slow along with all of it, as well as give back some ABS numberwang gains.

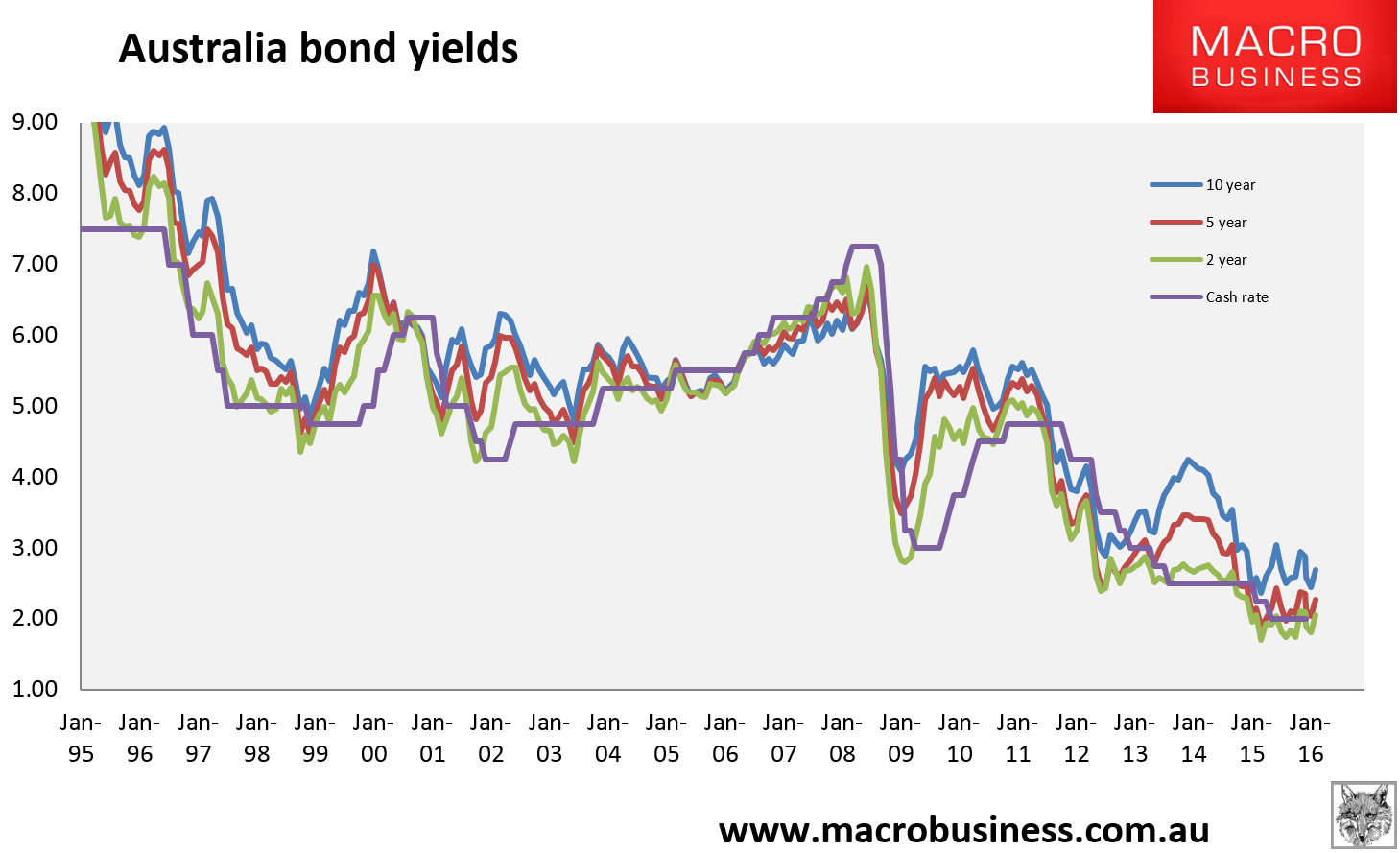

Yet, the Australian bond market is beginning to price rate hikes with the two year yield up to 2.06% Friday night:

There is not a lot of conviction in the rise in yields but it is still helping push the Aussie battler higher as it trades in the rear vision mirror view of the economy, towards 76 cents on Friday night:

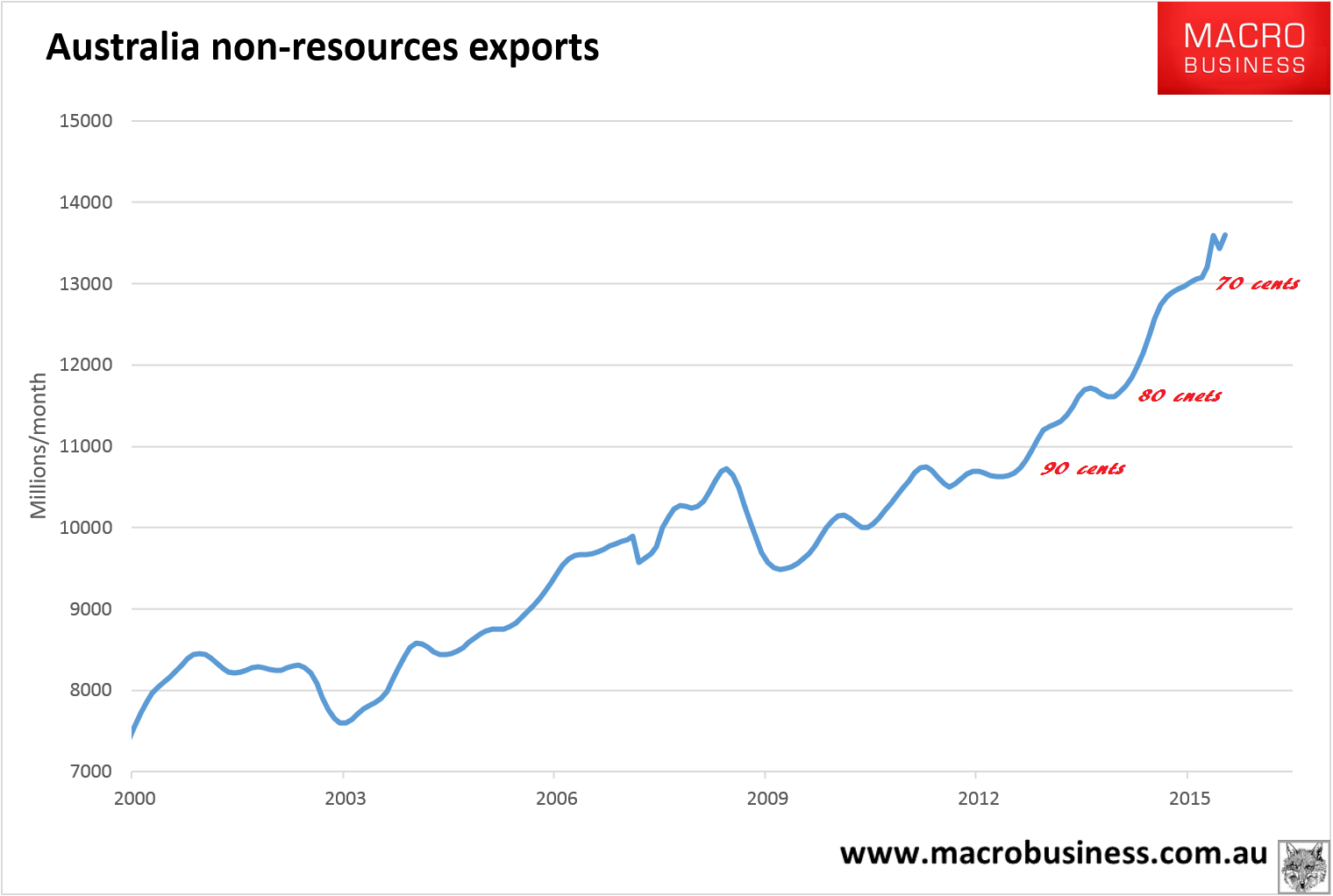

This could not come at a worse time for the economy given the prospective slowing in the eastern bubble. The one truly bright spot in the economic “rebalancing” is the lift in non-mining exports which have enjoyed two big jumps when the dollar fell to 90 cents then 80 cents and was in the midst of a third updraft triggered by the fall to 70 cents:

But that is now also in jeopardy.

It is still very difficult for Australia to register an actual official recession given high population growth and net exports growth but the income recession and very weak domestic demand are set to continue for another two to three years. That renders the overall economy chronically weak, leaving it vulnerable to external shocks, not least because we’ve spent so much of our ammunition on preventing the mining bust from crossing over the Great Dividing Range so far. It is still odds-on that as China slows and the US tightens that an external shock is coming in the next year or so.

Thus, the current Australian celebration is a false dawn, a commodity market led short squeeze that is temporarily boosting hopes of a bottom, but is paradoxically only snuffing out the faltering flame that is the Australian “rebalancing”. Both interest rates and the dollar will have to go lower.