The Mining GFC has been postponed by a perfect US jobs report that was perfect for growth and equally perfect for inflation as wage growth fell away. The result was both firming commodity consumption hopes and a weaker US dollar as US Fed tightening expectations eased. The US dollar fell:

That chart is a neutral symmetrical triangle suggesting that the jury is out on where it goes next. Commodity currencies had no doubts as they flew, with Aussie the strongest of all:

Advertisement

Brent broke out massively and appears to have big upside:

Base metals also busted out and likewise have room to fly:

Advertisement

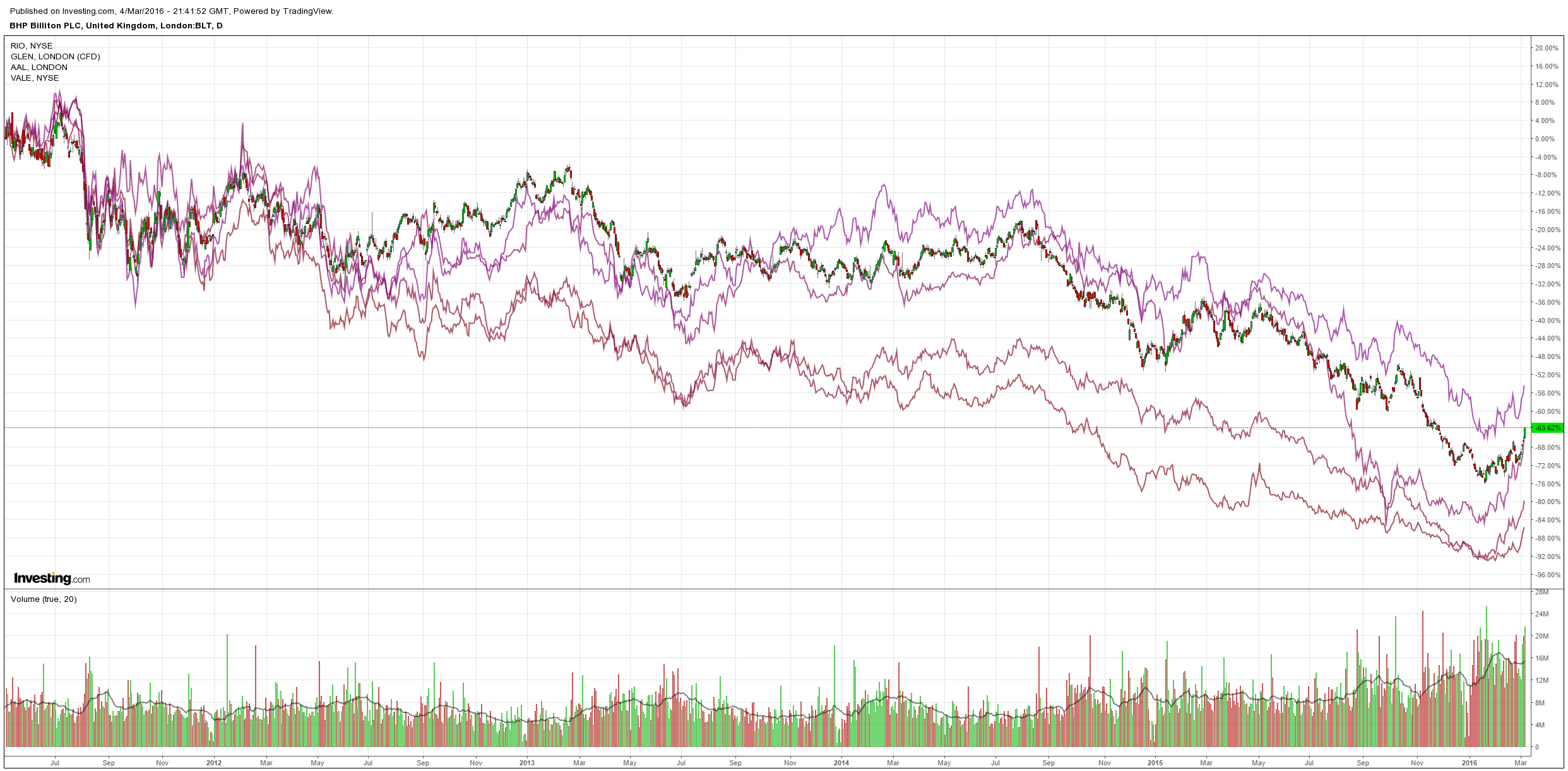

Big miners entered ecstasy with Glencore now double its August 2015 low, BHP roared 9% and RIO 6%:

Advertisement

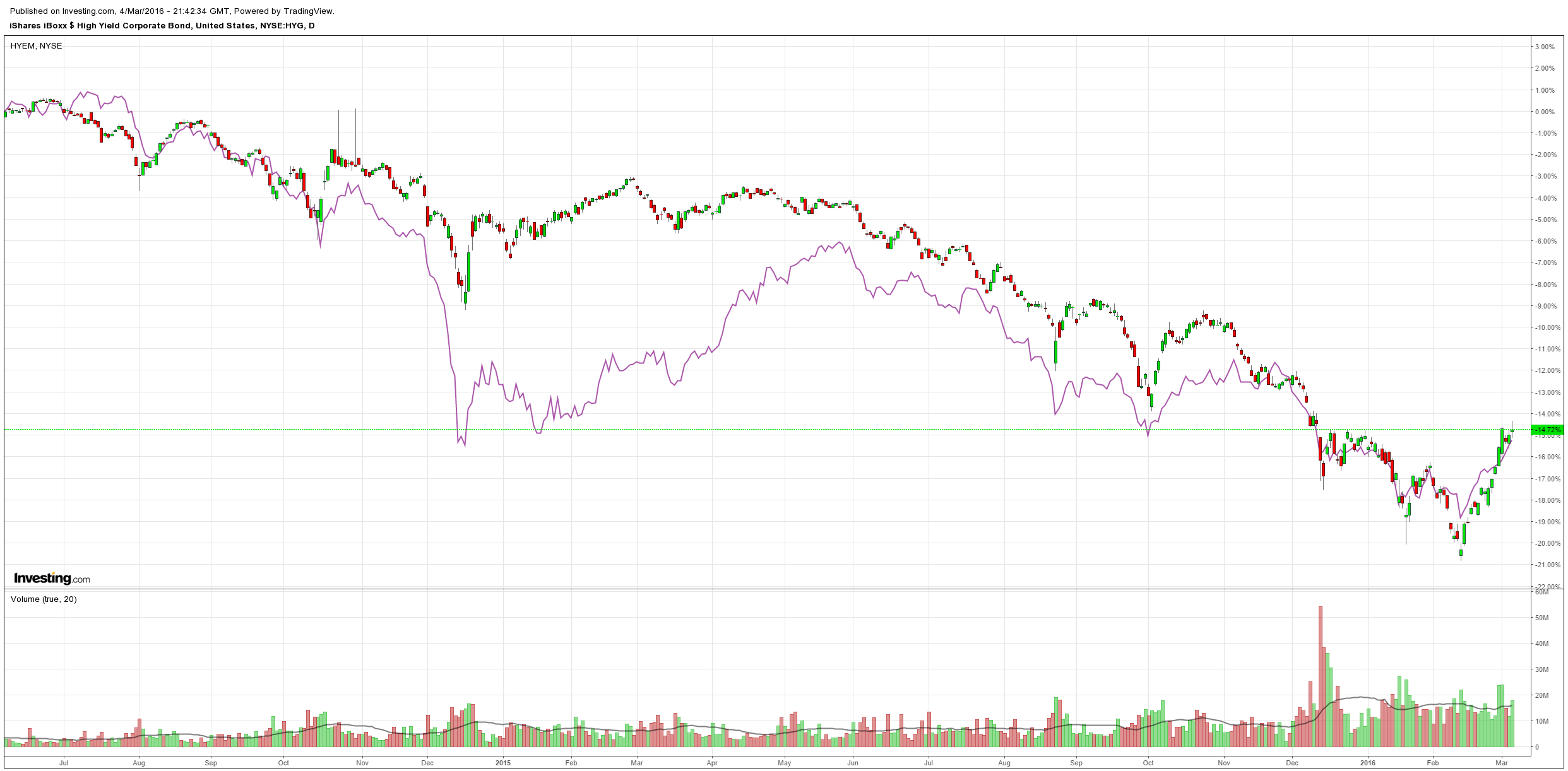

Oddly, credit was a big under-performer, which kind of suggests we’ve entered a rather frothy stage in the bear market rally:

Credit will have to keep recovering too or the rally will stall. The odds favour it doing so for a while yet so long as oil keeps recovering. BofAML agrees:

Advertisement

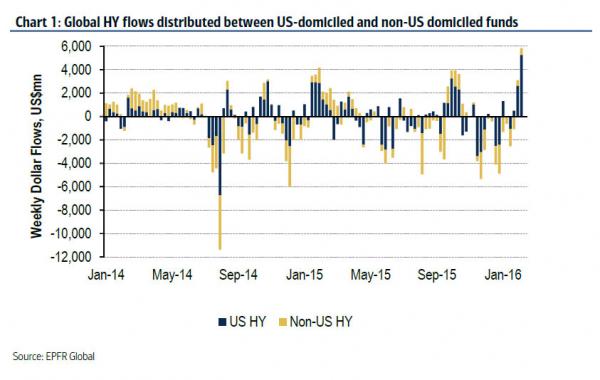

US HY has been starved of inflows since July of last year as investors waited for better entry points into the asset class. And as we have seen volatility subside, economic indicators turn more positive, spreads tighten 156bps, and oil rally nearly 20% in the past 3 weeks, retail has piled into high yield in what amounts to be the 2nd consecutive $2bn+ weekly inflow. However, we would fade the rally we have seen of-late as the fundamental backdrop has not changed meaningfully. In fact, we continue to see signs that we are nearing the end of the credit cycle with the default rate now at 4.2%, 2 consecutive periods of banks tightening lending standards, downgrades outpacing upgrades by a ratio of 6:1, and a general unwillingness to fund CCC borrowers. Regardless, this week’s inflow is undoubtedly a strong technical for the market and we would not be surprised to see the near-term rally continue for several more weeks.

So, what’s going on? Ivan Glasenberg has called a commodity bust bottom, from the FT:

Ivan Glasenberg, the chief executive of Glencore, argues that fears about a slowdown in China, which consumes about 40 per cent of the world’s copper, are overdone. “Our order book and our sales into China and around the world at the moment is pretty good. We had very good orders in the last quarter of 2015 and we continue to see good orders into China whether you are talking zinc, copper, nickel or coal,” he adds.

…A sustained recovery in commodity prices, say analysts, would need a pick-up in global economic growth and demand, particularly in China.

“Have we bottomed? I think so but I don’t want to sit here and predict commodity prices over the next few months,” says Mr Glasenberg. “A lot depends on China. We all have to wait and see.

Advertisement

It remains the MB view that this is a tradable rally not a bottom. This cycle is another in the long series of commodity price convulsions that has shaken Australia (and increasingly the world) since 2011.

First, the US economy is plodding along OK so its dollar will remain bid as other major economies do less well and ease policy by more, keeping the monetary headwind for commodities intact.

Second, new Chinese stimulus will not re-ignite its building boom. The surplus of commercial and residential buildings in three-quarters of Chinese cities remains vast. Instead, new stimulus is flowing into top tier city house prices prices and some infrastructure which will support consumption and a glide slope to lower commodity-intensity, but is not be enough to renew commodity demand. As we saw last week, this will require more stimulus and continue to pressure the yuan.

Advertisement

Third, as commodity demand plateaus (and falls for some like steel inputs), production surpluses will remain despite the capacity cuts to date. That means more cycling through price slumps below marginal cost followed by capacity cuts, then rebounds on the hope that it’s over only to see over-production sustained and further price slumps.

This remains the case in coal, iron ore and base metals. Oil is different because it generates higher demand as its price falls, such as in the US right now, and it is perhaps the closest to the bottom of the major commodities. Even so, it is also going through this shakeout process as it tests and retests marginal cost producers deeper and deeper into the cost curve, with US shale being stress-tested again now to see if it will spring back as prices rise.

Following the commodities boom of the 1970-80s built on the Japanese development blowoff, the commodity price crash did not end in a spectacular rebound in prices after sinking to overshot lows. Rather, it kept cycling through the above price discovery grinder and prices sank chronically for fifteen years.

Advertisement

That’s the kind of end you can expect to repeat itself overlaid with the following from macro economic legend Richard Koo:

For more than half a century after macroeconomics began to develop as an independent academic discipline in the 1940s, the emergence of breakthrough products such as aircraft, automobiles, home appliances, and computers provided companies in the developed world with a host of investment opportunities. Perhaps it should not be surprising that economic theorists at that time were unable to envision a world of no borrowers.

Economists were focused instead on the problem of how to effectively allocate a limited pool of private-sector savings. Government borrowing and spending was seen as something to be avoided since it was a symbol of inefficient resource allocation.

And until Japan caught up with the west in the 1970s, economists’ attention was focused on monetary policy since there was a surplus of domestic private-sector borrowers and no one envisioned capital fleeing the developed world for the EMs. This was the world of Phases 1 and 3, in which there were enough borrowers. Given the historical backdrop, it is perhaps only natural that economists at that time moved in the direction they did.

Macroeconomics did not keep up with changes in global economy

Subsequently, the global economy underwent major changes, with manufacturing shifting to Asia and the developed economies—almost without exception—experiencing asset bubbles that eventually burst, triggering balance sheet recessions. These economies entered Phases 2 or 4 as a result.

The discipline of economics, however, did not keep pace with these changes. Economists continued to build their theories and models based on assumptions that had only been valid in the developed economies of the 1950s and 1960s.

That is the main reason why most economists, whether in academia or the private sector, were completely unable to predict what has happened since 2008. They could not imagine a world where the private sector is actually minimizing debt instead of maximizing profits. Even now, the discipline tends to suffer from the bias that monetary policy is inherently good and fiscal policy inherently bad.

Unconventional monetary policy creates problems when it is wound down

These preconceptions underlie the current policies of inflation targeting, quantitative easing, and negative interest rates. Because central banks have pushed ahead with these policies even though there is no reason why they should work at a time of no borrowers, excess reserves created by the central bank now amount to $2.3trn in the US, or 15 times the level of statutory reserves, and to ¥222trn in Japan, or fully 26 times statutory reserves.

I have used the term “QE trap” to describe the problems that must be confronted when such policies are unwound. They can trigger severe market turmoil that cannot be avoided no matter how extensive the authorities’ dialogue with market participants.

Recently, for example, the markets took a tumble when the Fed moved to normalize monetary policy. The US central bank responded by delaying the normalization process, which stabilized the markets, but eventually fears of falling behind the curve on inflation will force it to resume the process. That will lead to renewed market turmoil in a cycle that has the potential to repeat itself endlessly.

QE was no game changer, and price has yet to be paid

Professor Krugman, who came up with the idea of lowering real interest rates by combining an inflation target with quantitative easing, has finally acknowledged that these measures were no “game changer” capable of sparking an economic recovery. But he still insists they did no real harm.

While that may be the case during a balance sheet recession, when there is no private loan demand, these policies can cause huge problems when they are wound down (witness the market’s recent gyrations). The global economy has now entered a phase characterized by this kind of instability.

Inasmuch as there is no clear way out, I expect this balancing act between the monetary authorities, who want to push ahead with policy normalization, and the markets, which violently reject each such attempt, will persist for an extended period of time, interspersed with periodic lulls like the current one.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.