Advertisement

From Citi:

- ENN buys into Santos — ENN Ecological Holdings (a subsidiary of ENN) has announced that it is acquiring Hony Capital’s 11.7% interest in Santos for US$750m, with Hony Capital then agreeing to become a strategic investor in ENN via a US$380m private placement. ENN is paying $750m for Hony’s interest in STO (205.2m shares) which implies ~A$4.85/shr for STO at spot FX, a 24% premium to yesterday’s close. The placement by Hony into ENN at an undisclosed price may bring into question if this see-through valuation for STO is in fact clean.

- ENN stake is still subject to same escrow conditions — Hony’s shares which were acquired through private placement with STO in late 2015 are restricted until 9th November 2016, meaning they may not be sold unless specific conditions are breached, although may be sold to a strategic third party with STO’s approval. STO stated in its release that it had granted permission to Hony to sell its shares to ENN, and the restricted shares are subject to the same conditions, unless 1) STO sell an interest in PNG LNG that reduces its interest below 10% (from current 13.5%); 2) A third party takes a 20% controlling interest in STO; 3) Santos approves the sale to a “strategic third party”. We estimate that ~159m of the 205.2m shares are restricted based on Hony’s disclosed ownership prior to private placement with STO, and shares acquired on market since standstill ended in February.

- Hard to see synergies, confirms our view on value — ENN is looking to grow an integrated gas business in China, with a particular focus on LNG. ENN is currently building a 3mtpa re-gas facility in Zhejiang Province where it is looking to grow demand through residential, transport (LNG bunkering in marine and trucks, CNG in cars), and power generation. It is hard for us to see synergies for ENN’s stake in STO however, given LNG offtake from STO’s projects are largely contracted. Therefore, we see this investment as based on value, with expectations of growing gas demand in China longer term, LNG markets moving back to balance after 2020, and a view of recovery in oil prices in the medium term. Our valuation of STO is A$6.75/shr based on a US$70/bbl (real) long term oil price, which is underpinned by a producing asset valuation of A$6.62/shr. STO is our preferred pick in the space.

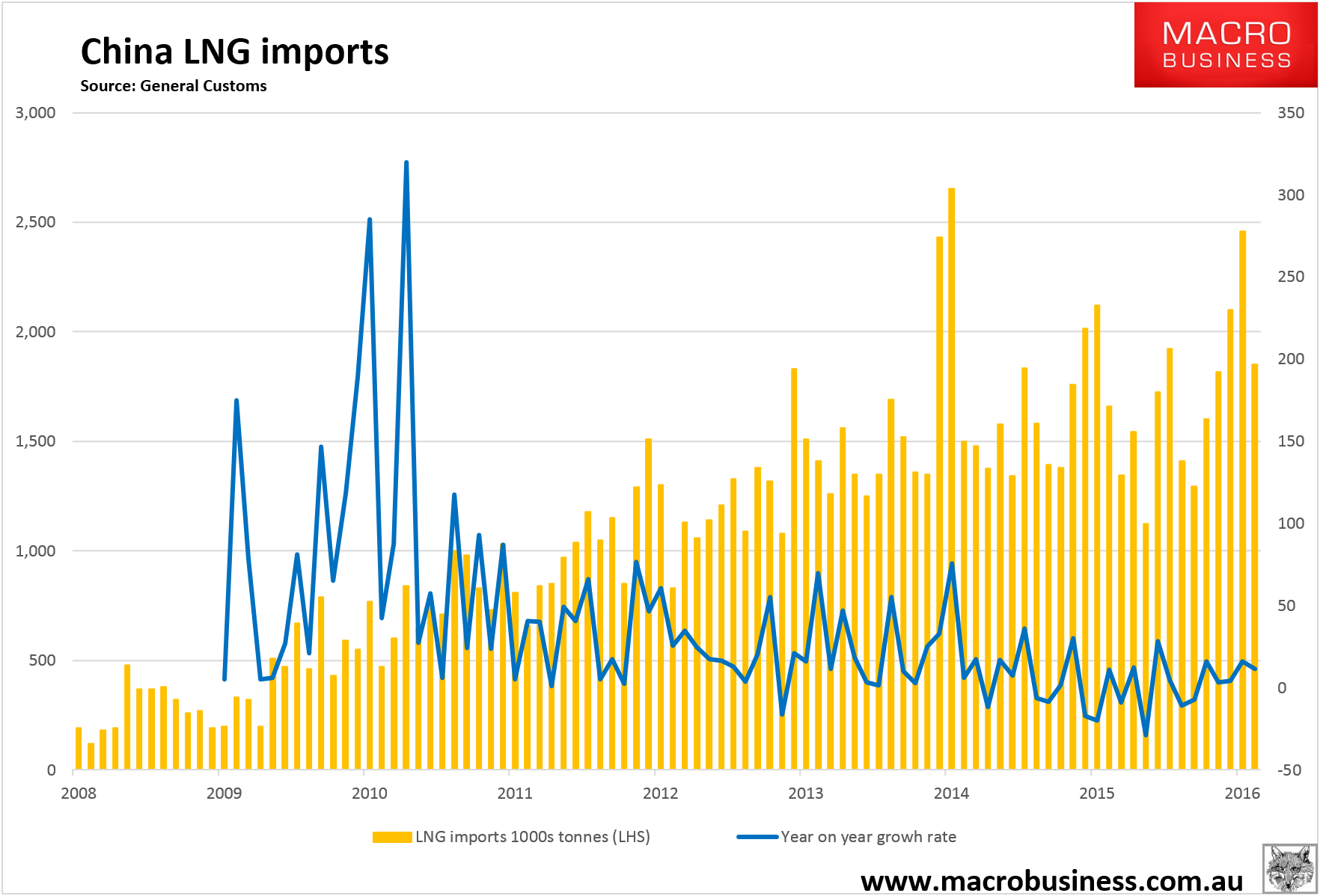

True enough, so long as you’re prepared to look across the valley or grand canyon more like. China’s LNG imports will rise (indeed contracted volumes means they have no choice):

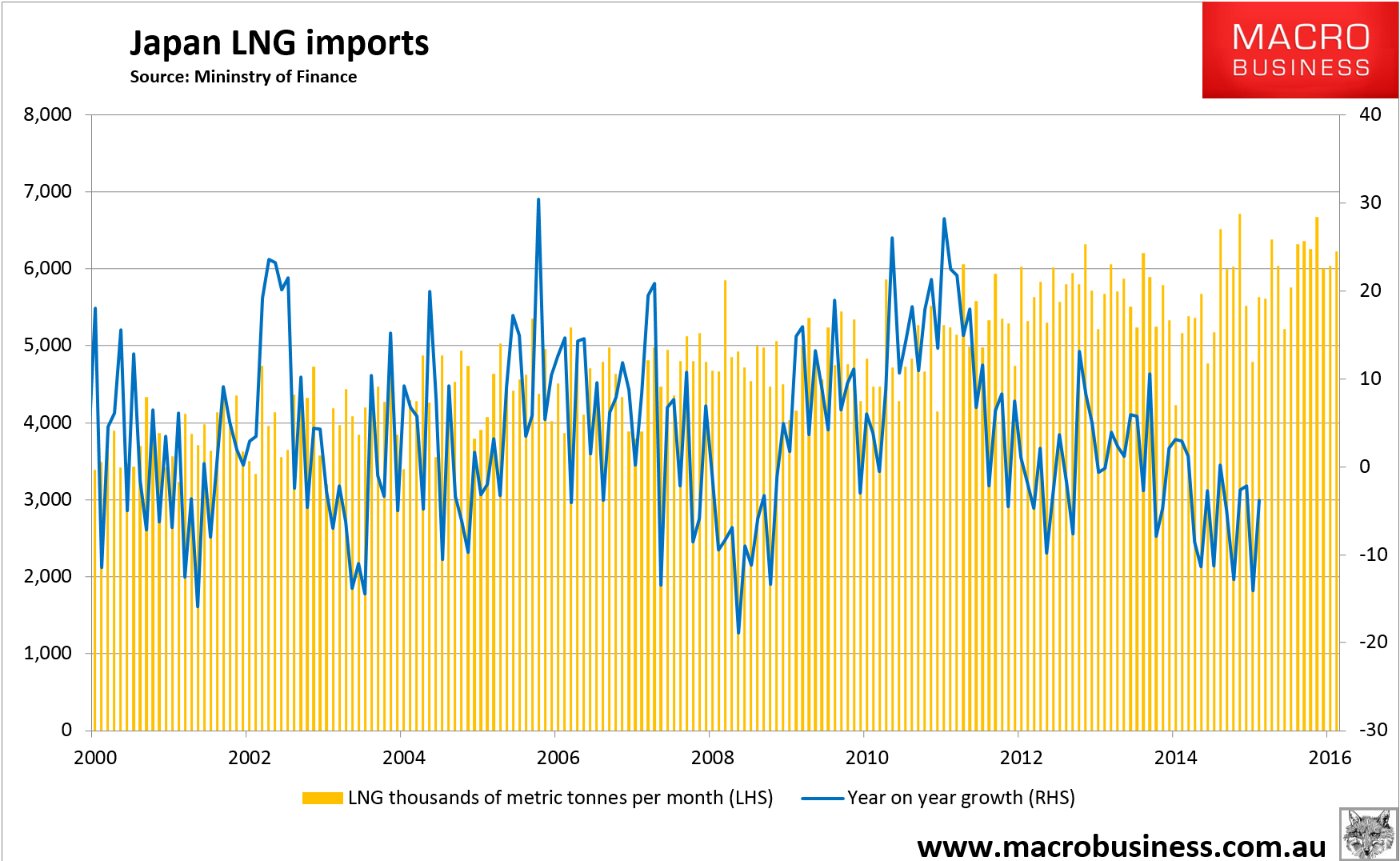

But they won’t rise enough for a very long time to offset glut as Korean and Japanese volumes fall just as fast on the resumption of nuclear power:

Advertisement

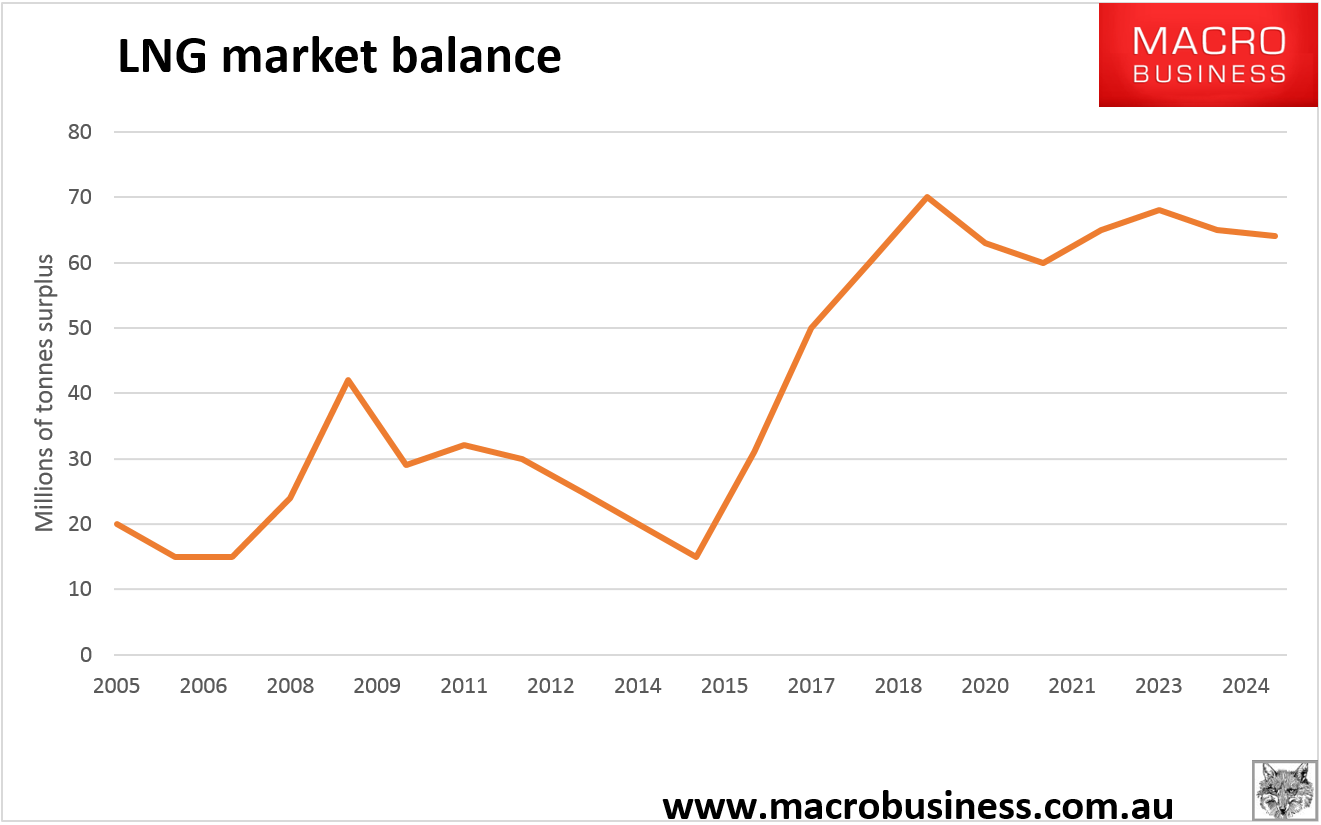

Keeping the market balance in severe oversupply well into the 2020s:

Advertisement

If it’s your fancy, there is plenty of time to wait for ludicrously cheap entry points into Aussie LNG plays.

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.