From Macquarie comes the news that there is life in the old dog yet:

The world’s mines, utilities and factories increased their production by more in January 2016 than over the whole of 2015. This is good news for metals demand, though other data suggests one should remain cautious on the outlook.

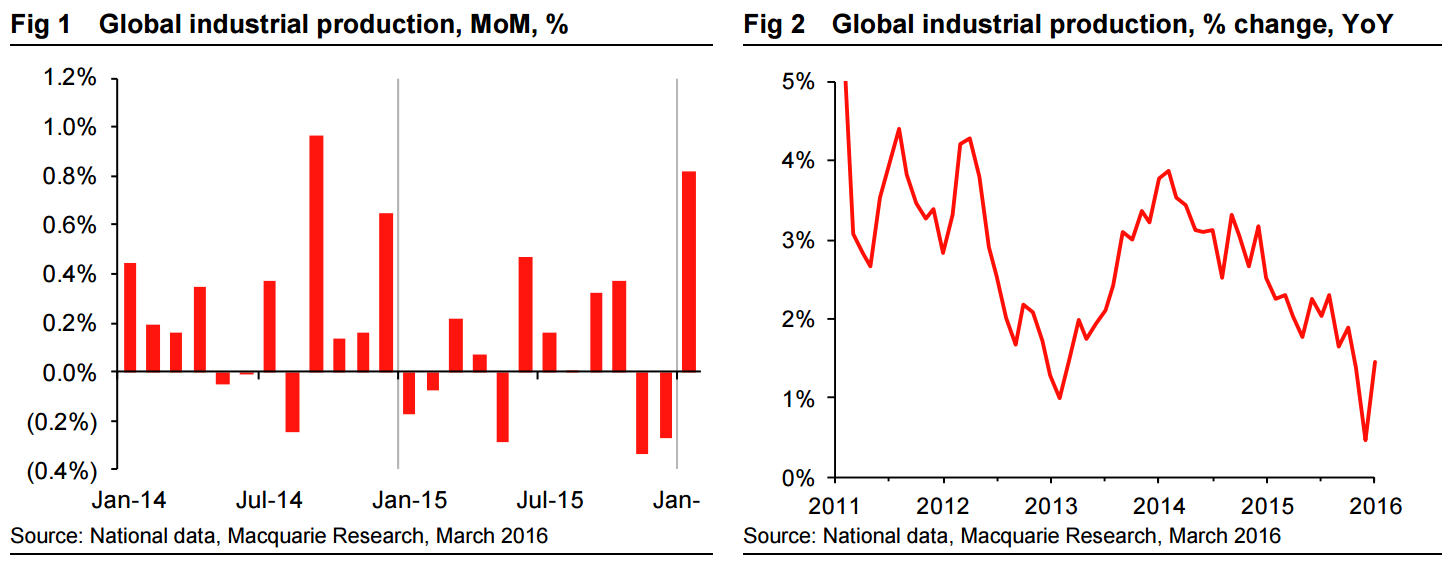

Industrial production (IP) – the output of mining, utilities and manufacturing – consumes a lot of metals and hence is crucial to the health of most markets. Output growth was very weak in 2015 – indeed after December’s dismal data we were bracing ourselves for a global industrial recession. That has all changed with January’s releases. Our database of 69 leading industrial countries, which account for about 93% of global IP, shows output surged by 0.82% MoM, more than it grew over the entirety of 2015 (fig 1).

Furthermore output actually fell MoM in January 2015, so January 2016’s surge was sufficient to push the YoY change up from December’s distinctly recessionary 0.4% YoY, to a much more respectable 1.5% (fig 2).

It is possible technical explanations account for at least part of the strong recovery. One is imperfect seasonal adjustment, which could have depressed December’s data and has made January’s recovery seem more impressive. This seems an issue in Japan in particular, which even using its seasonally adjusted data always has a big bounce in January. In the Eurozone such an effect is not so apparent, though fig 5 shows how much adjustment is done to the raw1 data, using Germany as an example. A weak January absolute number was made higher by calendar adjustment (how many working days there were) and then seasonal adjustment. All of these adjustments are legitimate, but an extra working day is not what most people think when one says industrial production rose strongly MoM. There are also short-term issues, such as that the weather was somewhat colder in January than December in many countries. In the US this meant depressed utility output in December and higher in January (fig 6), something which contributed about half of the MoM increase in total industrial output.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.