Home prices have fueled up fast in Tier-1 cities but remained quite stable in lower tier cities. In February, prices of new homes in Shenzhen surged 72% yoy or 3.4% mom to RMB48,095/sqm, and the yoy home price inflation was also quite staggering at 45% in Beijing and 28% in Shanghai. Meanwhile, it was on average 1.5% yoy in Tier-2 cities and -0.1% in Tier-3/4 cities.

The housing market performance has further diverged between the Tier-1/2 cities, with continued improvement in sales, and Tier-3/4 cities. Moreover, there has been extensive media coverage recently on rapid home price increases and booming peer-to-peer (P2P) lending business to fuel speculation through amplified leverage ratio. Some investors are increasingly concerned about a potential reversal in property market sentiment as the one in 2008.

In our view, there are rising warning signs of property overheating in Tier-1 cities, especially in Shenzhen, with too-fast price inflation and rising usage of informal leverage for mortgage down-payment. The size of such informal leverage should still be very small and Tier-1 cities are only 5-9% of China’s overall property market by various measures, while the overall housing mortgage size is still quite modest. This implies systemic risks to the financial system remain manageable, in our view.

To facilitate housing destocking in lower-tier cities, we expect the government to roll out more supportive measures: (1) Cash payment as the major form for shanty town redevelopment (with the target of 6mn units in 2016); (2) to encourage local governments to acquire existing projects as social housing; (3) to provide tax incentives for individuals and institutions (such as SOEs) housing purchase; and (4) to speed up Hukou reforms with better social welfare access and fiscal subsidies in small cities to attract migrant workers. Moreover, continued monetary easing is likely, with two 25bp policy rate cuts in 2016, in our view.

The State Council encourages local governments to carry out their specific housing destocking initiatives. However, significant loosening, such as zero down-payment or lending to college student without stable sources of income in the first draft of policy changes in a certain province, will likely be prohibited.

Regarding Tier-1 cities, we expect policies to better balance supply-demand and rein in price speculations. The Minister of Housing suggests several measures are being discussed, including: (1) Stricter enforcement of housing purchase limits and differentiated tax and loan policies; and (2) increase in supply of land, ordinary homes and social housing. Moreover, financial regulators will likely tighten scrutiny of mortgage applications and cases with down-payment loans involved will be rejected. Housing purchase-related P2P lending will be prohibited.

If authorities sit on first tier city prices then lower tiers are not going to rally.

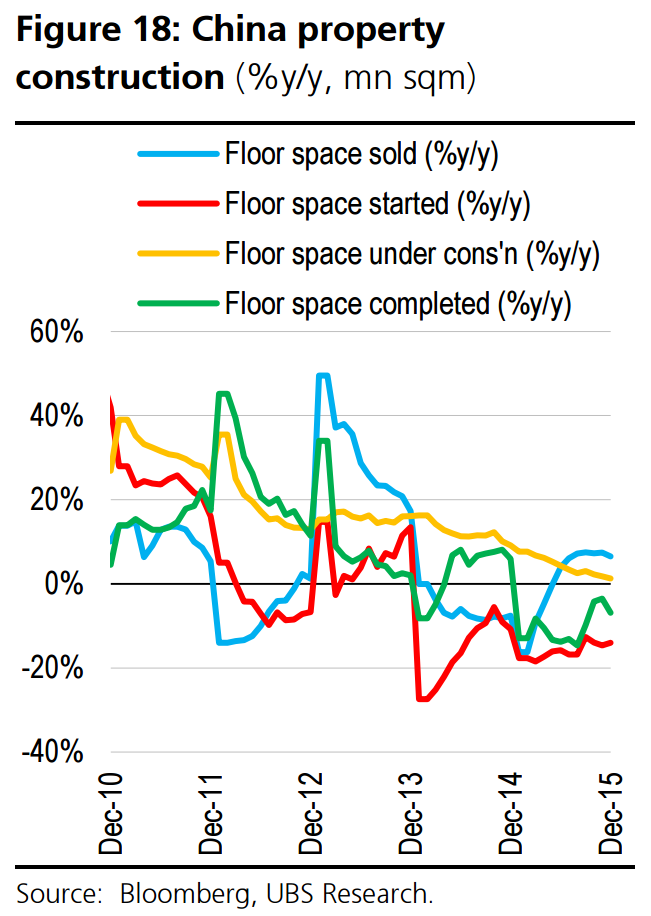

This is my number one reason for remaining bearish about iron ore and global commodities. Depending upon who you ask, tier 3-4 city housing constitutes 70-90% of Chinese construction volumes. Until that overhang is cleared then this will continue:

Advertisement

China consumes roughly half of the world’s hard commodities. Residential construction consumes roughly half of that consumption. Until it turns there is no demand growth coming and probably shrinkage.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.