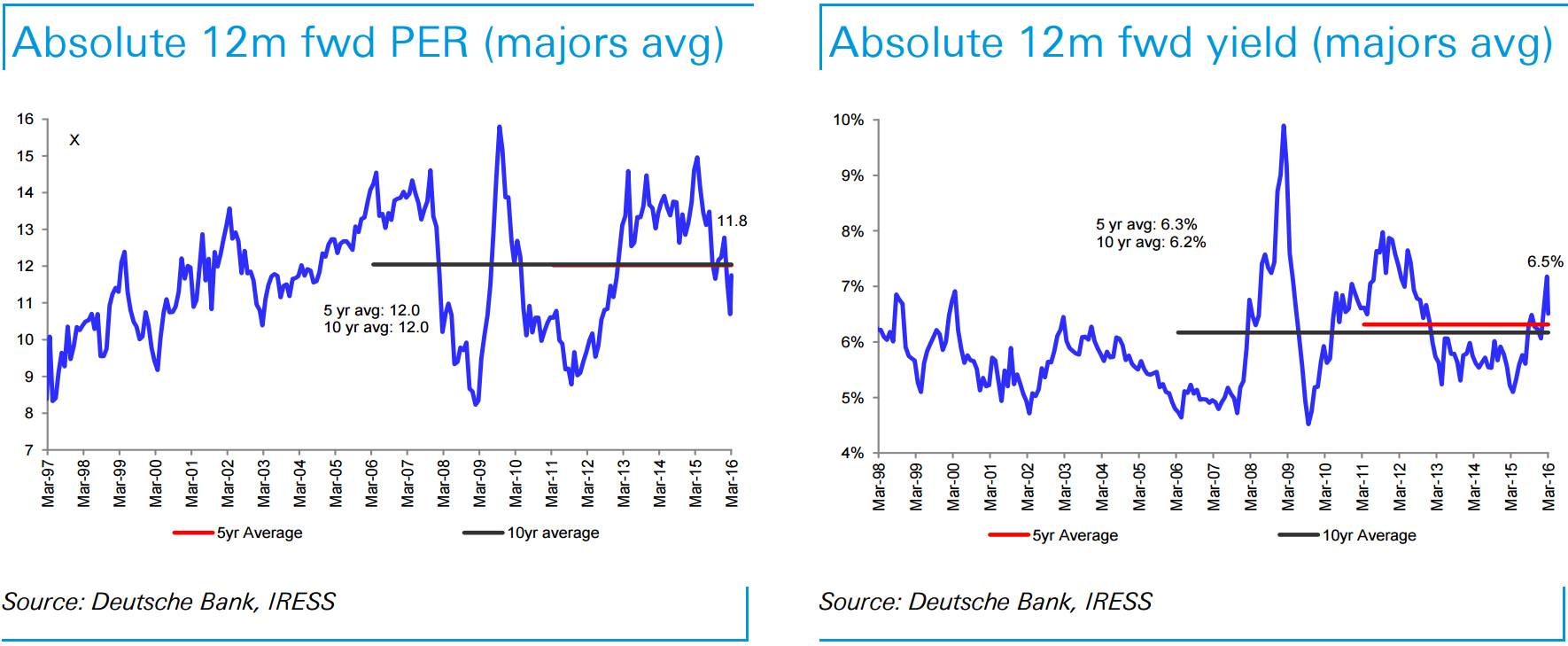

Inside the Bank Vault this week we highlight key valuation trends in the bank sector over the last month as well as take a look at the week’s global bank regulation news. The major banks on average are currently trading at a ~2% discount to their 5 year historical avg absolute PER (11.8x vs 5yr avg 12.0x), following a recovery in share prices over the past month. Looking at the majors’ 12m fwd dividend yields, they are currently trading at an average of 6.5%, slightly higher than the 5yr historical avg of 6.3%.

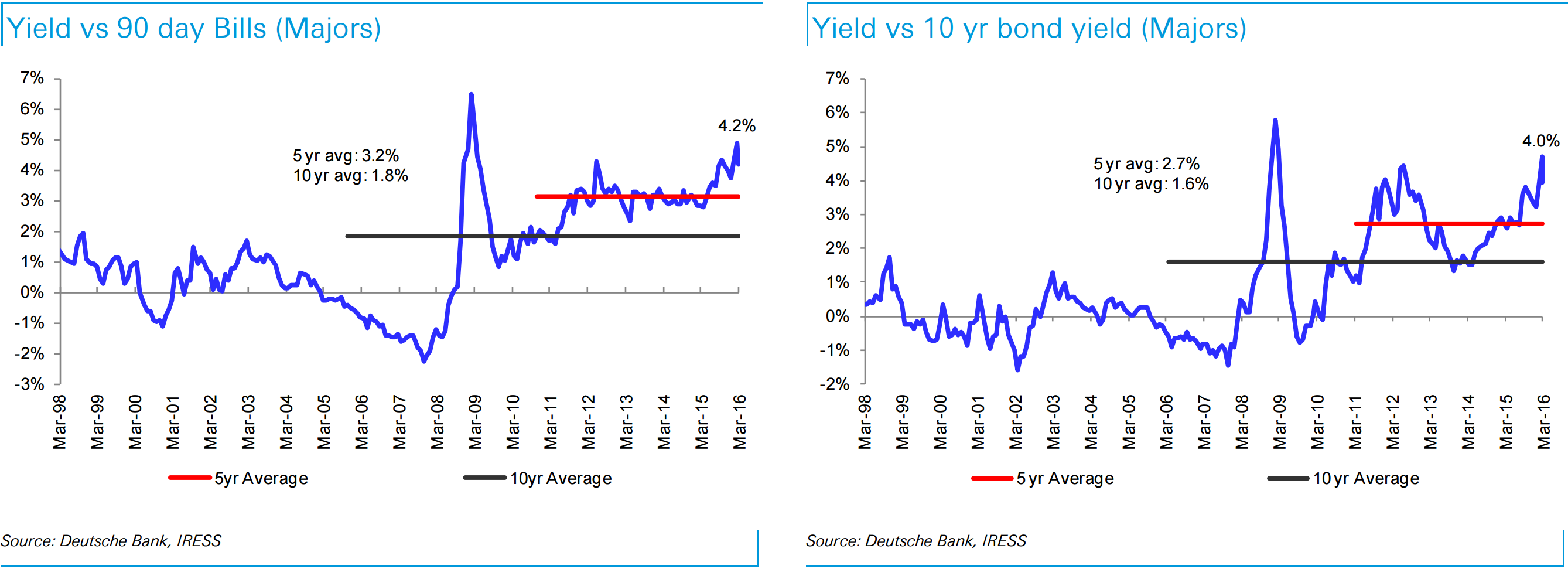

Looks to me like the recent big fall in bank valuations was really the popping of the “yield bubble”. Banks have never before traded on such high P/Es for such a long period and with rising global interest rates that trade ended.

Interestingly, that has actually coincided with falls in the local bond yields (but rises in the US as it tightens):

Advertisement

That might suggest that we’ll get another round of bank asset inflation if the Fed reverses but given it is nowhere near doing so, and that it will take a quite serious growth accident to trigger it, I think that unlikely. Rather, banks are now poised between the risks of that growth accident and firm valuations stemming from a still low yield environment.

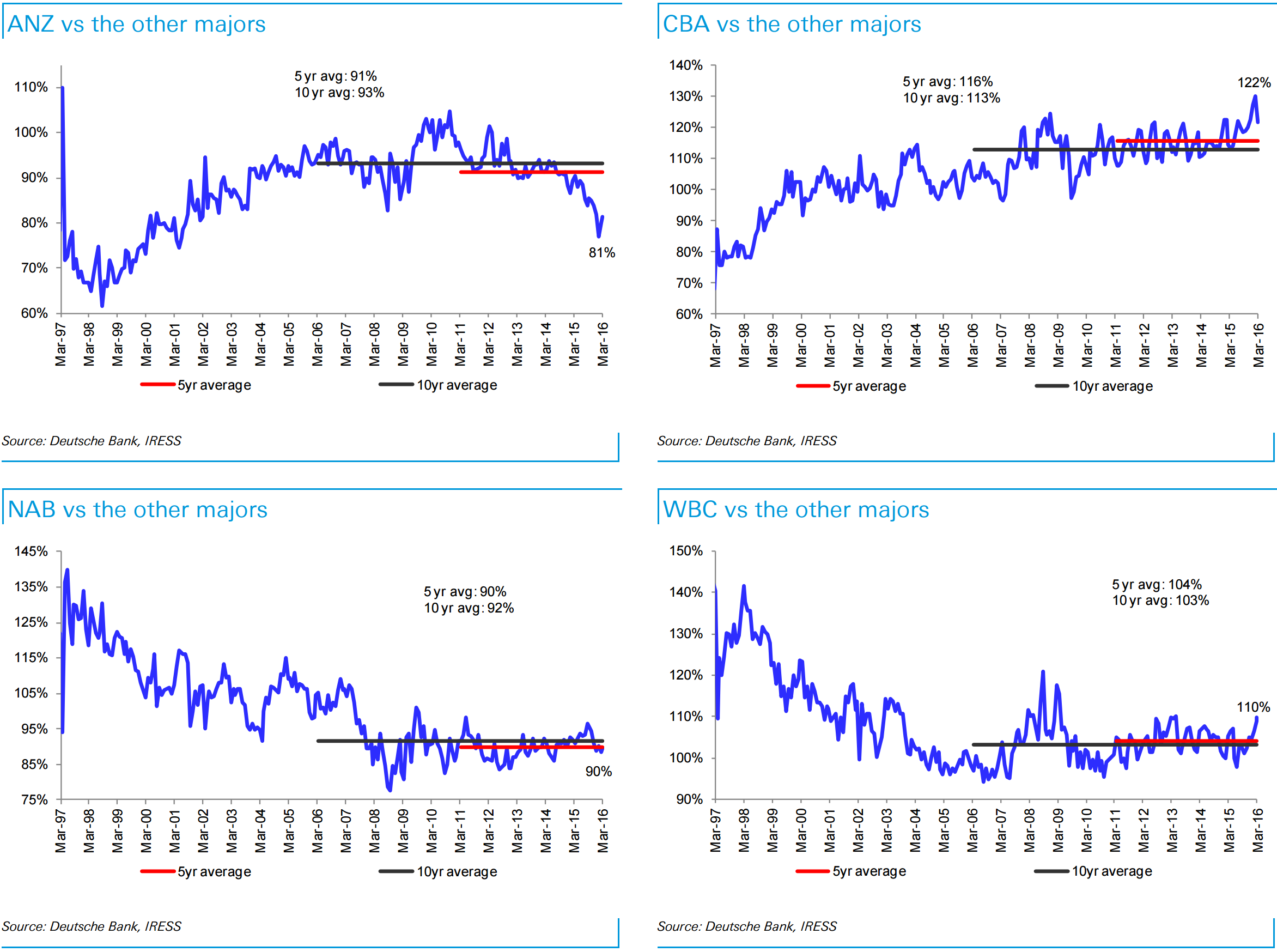

As for individual banks, the big mortgage monsters still look really overvalued to me:

Advertisement

If you believe the Australian rebalancing is on track then the banks look marginally cheap. If you don’t then they look seriously overvalued with both yield and P/E pressure ahead.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.