While the balance sheets of Australian energy stocks have attracted significant scrutiny over recent months (particularly following credit rating reviews by both Moody’s and S&P after a change in oil price assumptions and during reporting season), emerging concerns surrounding access to liquidity appear to have little consequence for the Australian large-cap E&P sector, in our view. Furthermore, all large-cap energy companies are now break-even under the forward curve in 2016. Consequently we believe that the Australian Energy Sector remains well placed to navigate a weaker oil price outlook.

Liquidity is king: Companies have built substantial liquidity positions (we estimate U$12.6bn in available liquidity), successfully deferred major debt maturities until post 2018 (with only U$3.3bn maturing over the next 3 years) and therefore have little reliance on external capital markets for the foreseeable future (albeit with deteriorating credit metrics if further committed debt facilities are drawn which could have implications for credit ratings).

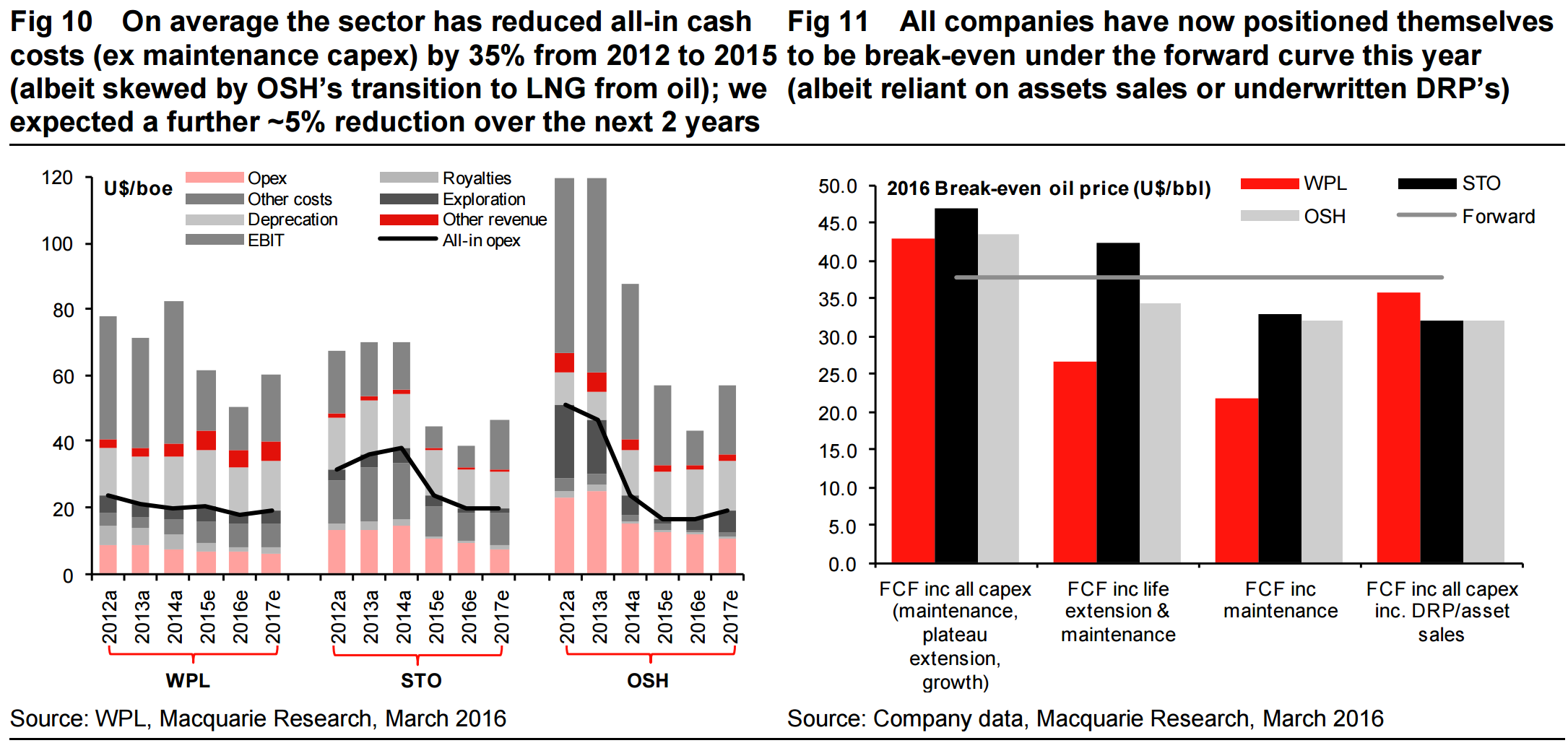

Striving to break-even at all cost: While access to liquidity is paramount, management teams are also targeting break-evens as close as possible to the forward curve to prevent excessive draw-down of respective liquidity positions in the near-term. Through a combination of cost reductions, asset sales, underwritten DRPs, capex deferrals and hedging, all large-cap energy companies are now break-even under the forward curve in 2016. However WPL’s underwritten DRP, STO’s reliance on asset sales and ORG’s hedging program are not recurring, suggesting that further work will be required to lower sustainable break-evens.

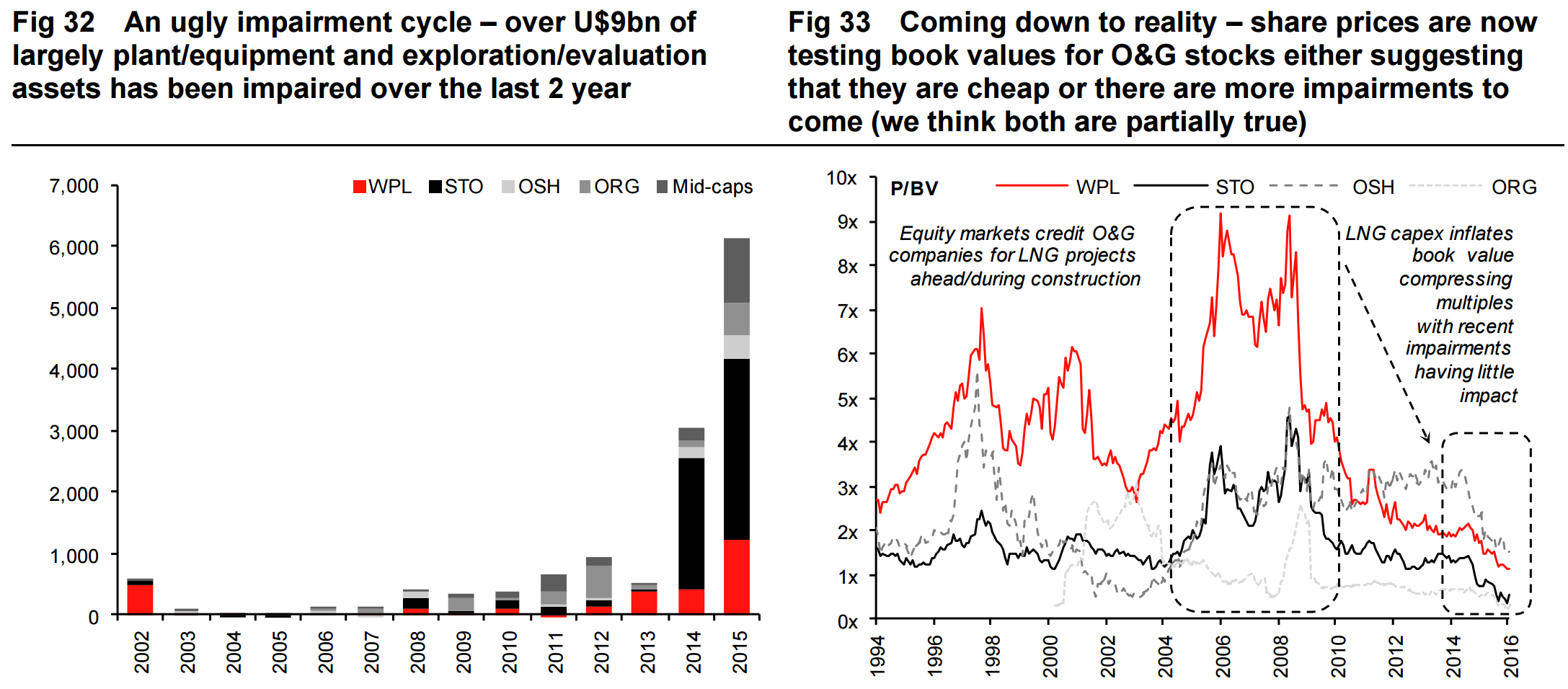

Ugly impairment cycle: The largest impairment cycle seen in over two decades (we estimate U$9bn over the last 2 years) has raised questions surrounding companies’ current long-term planning assumptions and prior investment decisions. Many companies have now adopted the depressed forward curve in the short term and a long-term assumption averaging ~U$77/bbl from 2020. This appears conservative vs. Macquarie’s oil price deck but 35% higher than the longer end of the forward curve (which could see further impairments if further revisions are made).

Quite right and all points I’ve made myself many times. The recent crash may be somewhere near the bottom for share prices but there are still good reasons to think that there is no hurry to buy and as cheap if not cheaper opportunities lie ahead. The first is made by Macquarie itself in another note:

We remain short-term bearish on crude oil despite the recent rally. Crude seems to be increasingly discounting bearish news and data including rapidly rising inventory levels. Market fundamentals, in our view, suggest the rally is too early, and we expect crude to retrace to the $30 per barrel range. Event WTI crude is up $8.50 per barrel or 32% since February 11, 2016. Over that same period, Middle East loadings have remained robust and global storage levels have continued to rise.

The key factors we are concerned about include:

Cushing as of today is likely at its maximum capacity of 66 million barrels. Cushing has approximately 80 million of shell capacity so there may be ways to get more crude into the tank farms there, but at lower prices.

KSA loadings are up approximately 200 K BPD over the last three months. Iranian loadings have jumped 300 K BPD from the last quarter and look to be rising over the next few weeks. This ST bearish trend is largely being ignored in our view.

The second half of the US TA season is underway and roughly 1 million BPD of CDU capacity will be out until mid-April before falling to 400 a day by early May.

Crude import volumes are likely to stay high for at least the next few weeks. The question is will these physical realities dominate or will this substantial growth in net length drive prices higher regardless of the physical market weakness. These fundamentals make it hard for us to get comfortable with the current rally though we believe long-term value is substantial.

That is also my view, not least because we are already seeing US capital markets beginning to open up for shale again.

Advertisement

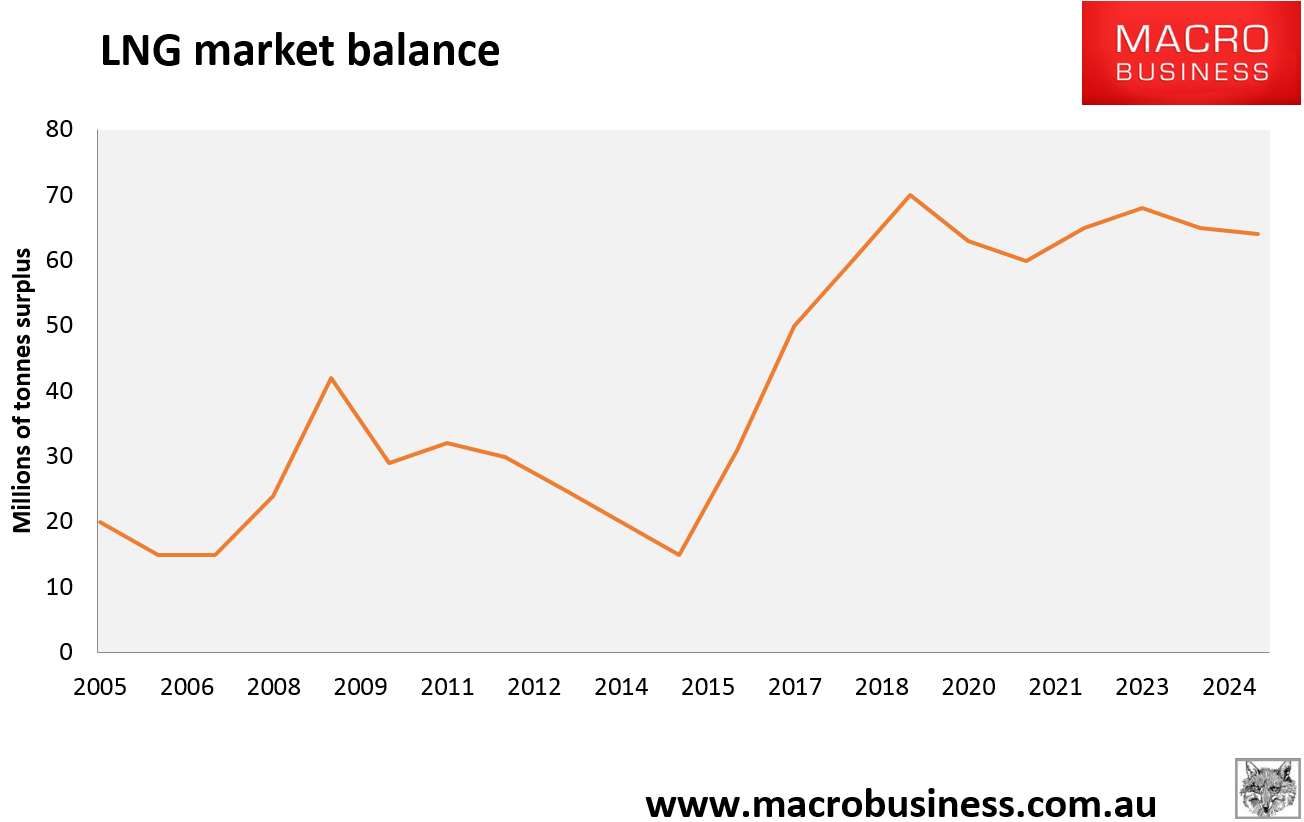

Second, the other big risk is the building spot market glut in LNG. It is enormous at perhaps 50mtpa and is already putting a lot of pressure on existing contracts:

We appear to be at the threshold of some kind of mass default on existing contracts. It has already begun with Qatar renegotiating existing agreements with India and Pakistan. How is ORG going to maintain an oil-linked pricing slope above 15% when new deals are being done at 13% or you can buy spot for half of contract at $3mmBtu and simply default and refuse to pay any fine, as India did. As LNG break evens fall so will prices via contract…ahem…adjustments. It’s Australia’s 2009 iron ore success in reverse for LNG.

Advertisement

So, more oil pain, massive impairments and structural change to LNG pricing make it too early to allocate to the white elephants.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.