Tom Garcia, chief executive of the Australian Institute of Superannuation Trustees (AIST), has written a tirade in Fairfax lobbying against “ad hoc” superannuation reform and calling for the compulsory superannuation guarantee rate to be increased:

Last year’s 11th hour Budget change to the age pension means test is just one example of the perils of ad hoc policy, though the impact won’t be felt until next year. Left unchanged, the new asset test will significantly widen the equity gap in Australia’s retirement income system – one of the very issues this current tax inquiry was set up to rectify.

The introduction of a more aggressive age pension taper rate undermines the incentive for middle Australia to save once their super balances reach around $400,000, after which increased savings are largely clawed back through lower pensions. In the first year alone, hundreds of thousands of part-pensioners will be affected, many of them losing their pension altogether.

Yet it is this very group of Australians – those in the 30th to 70th income percentile who typically rely on some pension support in their retirement – who currently receive the least Government support to save for their retirement…

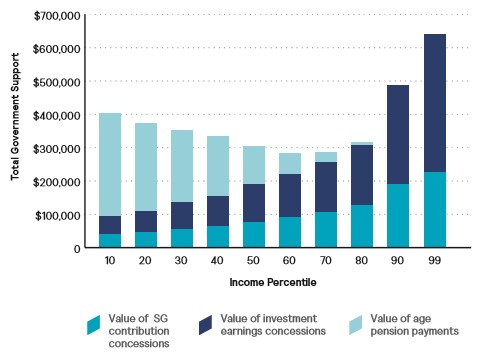

AIST’s research shows those at the top end of the income percentile receive as much as $660,000 of total government support to their retirement income over a working lifetime (mostly through super tax concessions). This compares to around $300,000 in government support to someone on the median wage of about $50,000 a year.

AIST’s complaints about last year’s changes to the Aged Pension makes little sense, given they merely unwound some of the largesse provided by former Treasurer, Peter Costello, who greatly relaxed the assets test to qualify for the Aged Pension.

Prior to this decision in 2006, the Age Pension was reduced by $3 a fornight ($78 a year) for every $1,000 of assets above a certain threshold.

In May 2006, in the twilight years of Government, Peter Costello announced that the taper rate applying to assets (excluding the family home) would be halved to $1.50 for every $1,000 of assets above the threshold, effectively doubling the value of assets allowed for eligible part-Age Pensioners.

This relaxation in the Pension assets test meant that a swathe of wealthy retirees qualified for taxpayer support, as stated by former Treasurer, Joe Hockey, on Budget night in 2013:

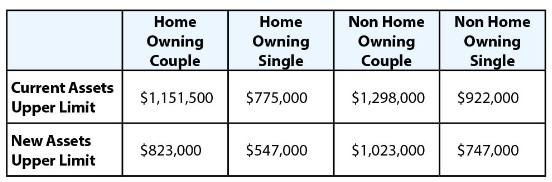

“…currently, an individual with a home and almost $800,000 in assets still qualifies for the age pension; a couple with a home and almost $1.1 million in assets also qualify for the age pension”.

Following the reforms by the Coalition, announced in last year’s Budget, thresholds will be adjusted for the Aged Pension so that those with financial assets (in addition to the family home) of $547,000 for singles ($823,000 for couples) will no longer qualify for the part-pension (see below table).

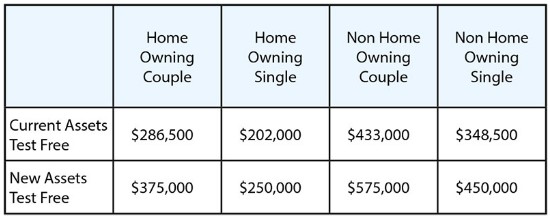

However, there will also be additional funding for those with few financial assets – by increasing the “assets test free area” (the amount of assets you can have before your pension will be affected – see below table) – as well as retaining access to pensioner concession cards.

Based on the above, it is a bit rich for AIST to complain that the new pension rules will harm “middle Australia”, given they provide greater benefits to those at the lower end, whilst restricting access to wealthier retirees – as they should.

AIST does have a point when it argues that the wealthy are receiving the lion’s share of taxpayer assistance in retirement. Indeed, Mercer and AIST’s own research showed that the top 10% and top 1% of income earners receive more government retirement support than the other 90%:

But this does not mean that the superannuation guarantee should automatically be raised to 12%, given such a move would merely heighten inequities already present in the superannuation system, would rob lower income workers of much lower disposable income via less take-home pay, and increase superannuation concessions’ drain on the Budget.

Rather, what is does argue for is:

- Making superannuation concessions more progressive, by replacing the flat 15% tax on contributions with a 15% discount from one’s marginal tax rate;

- Re-instating the 15% earnings tax for those aged over 60;

- Implementing a life-time limit on concessional superannuation contributions; and

- Winding back the overly-generous ‘transition-to-retirement’ superannuation rules.

While AIST is correct to lambast the inaction and ad hoc discussion over super concessions, it should not wage a faux war on the pension reforms – which have improved the equity and sustainability of the system – or advocate a rise in the superannuation guarantee before the existing inequities have been addressed.