In 2005, former Treasurer Peter Costello implemented the mother of baby boomer bribes in the form of the “transition-to-retirement” (TTR) rules, which allowed those aged over 55 to legally minimise their tax by salary sacrificing up to $35,000 into a superannuation account (thus paying 15% contributions tax) and then simultaneously withdrawing the funds as income. In turn, TTR effectively allowed high income earners to reduce their marginal tax rate from 45% to 15% on the last $35,000 of their income.

I have often described transition-to-retirement pensions (TRIPs) as the super saver’s version of ‘having your cake and eating it’.

A transition-to-retirement pension enables Australians who have reached their preservation age (at least the age 55 and increasing to age 56 and older, depending on date of birth) to access their super in the form of a pension without retiring or satisfying an additional condition of release…

Although some individuals use TRIPs for a gradual transition into retirement, the majority of TRIPpers appear to have used the strategy for boosting super savings and tax minimisation…

One of the more popular TRIP strategies is to salary sacrifice into your super fund up to your concessional (before-tax) contributions cap, and replace that income with tax-free (if over 60) pension payments, or concessionally taxed pension payments (if under 60).

And ASIC provides a useful example of how Costello’s TTR rules can minimise one’s tax:

Andy is 55 and earns $100,000 a year. He intends to keep working full-time for another few years. Andy has $220,000 in super.

Andy’s financial adviser explored whether a transition to retirement (TTR) strategy could be useful…

How will the strategy work?

1.Andy transfers most of his super to an account-based pension. This saves money as he no longer pays tax on investment earnings.

2.He salary sacrifices a large amount into super. This saves income tax, but reduces his take-home pay.

3.Then, he withdraws up to 10% of his pension balance each year, which boosts his overall income back to his current level.Benefits

Andy’s take-home income stays the same. Overall he saves over $2,300 in tax in the first year. This means Andy will have more money in super when he finally stops work.

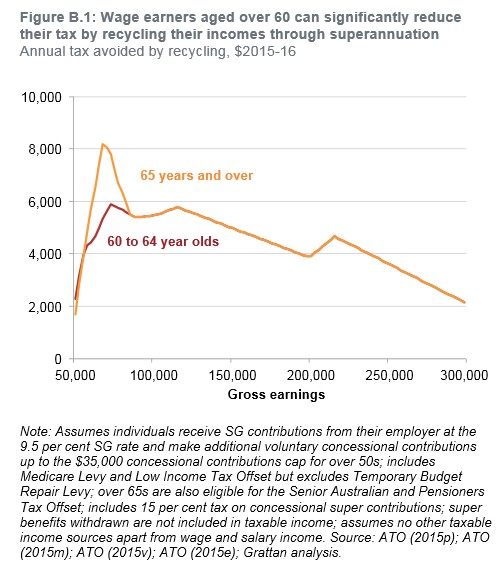

Likewise, the Grattan Institute report, entitled Super tax targeting (see here for summary), provided an excellent analysis of the TTR rules and their deleterious impact on equity and Budget sustainability:

Wage earners aged over 60 can withdraw money from superannuation tax-free. They can reduce how much tax they pay on wage income and immediate consumption by contributing up to the concessional cap out of their wage income, and then withdrawing the funds from superannuation the next day to consume immediately. Since workers only pay 15 per cent tax on the income contributed to super, rather than their marginal tax rate, the tax savings can be substantial. For workers aged between 60 and 64 years earning between $65,000 and $150,000, this strategy reduces the amount of tax paid by over $5,000 (Figure B.1). The tax benefits for workers aged 65 years and over are even larger.

Access to superannuation for older workers, such as via ‘transition to retirement’ rules for those aged below 65, was designed to allow individuals to move from full-time to part-time work without reducing their incomes, using superannuation withdrawals compensate for lower wages. However, recent evidence suggests that these rules are mainly used by high wealth individuals to reduce their tax bills while they continue to work full-time…

In essence. Costello’s TTR rules were a sop to the older generation, effectively enabling richer older people to avoid paying tax and shifting the tax burden to the younger generations.

Not surprisingly, then, the Productivity Commission urged reform to the TTR rules in its Superannuation Policy for Post-Retirement report, released last year:

…the tax concessions embodied in transition to retirement pensions — designed to ease workers to part-time work prior to retirement — appear to be used almost exclusively by people working full-time and as a means to reduce tax liabilities among wealthier Australians. A better understanding of how these incentives are being used and by whom could potentially improve the efficacy and sustainability of the retirement income system.

Today, The AFR has reported that pressure is being applied on the Coalition to wind-back Costello’s TTR lurk once and for all in the interests of equity and Budget sustainability:

The latest Australian Tax Office figures show the payment of transition-to-retirement benefits from self-managed super funds more than doubled from $1.7 billion in 2010 to $3.8 billion in 2014. There are no figures for drawdowns from regular super funds…

Financial planners and super funds encourage the take-up of the transition-to-retirement loophole as a tax planning strategy…

Treasurer Scott Morrison on Sunday pledged to ensure super could not be used to build “tax-free inheritance pools”.

Grattan Institute chief executive John Daley said there was “absolutely no public-policy justification” for maintaining transition to retirement arrangements.

He said people could pay their salary into the low-tax super environment and withdraw it the following day, without having to prove how many hours they are working.

“What’s it worth as pure tax avoidance device? The answer is, for a broad range of incomes above a certain level, it’s $5000”…

Chartered Accountants Australia and New Zealand said a work test should be applied to show that superannuants are reducing their hours of work.

SMSF Owners Alliance chairman Bruce Foy said if the system was being rorted, the behaviour should be stopped.

Hopefully, the Turnbull Government will unwind Costello’s superannuation blunders, starting with the “transition-to-retirement” rules, but also ending the tax-free status on superannuation earnings for over-60s, and making super concessions fairer.

If the Budget deficit has any hope of being eliminated, and the “age of entitlement” addressed, the Coalition must right Costello’s superannuation wrongs.