A business cycle long in the tooth

Regular readers will know that MB’s current implied asset allocations matrix is very conservative. For the past year or more we discussed selling into rallies for stocks, selling excess property exposures, and championed bonds and cash. Obviously we also see interest rates and the Australian dollar falling further as well.

In part this outlook is the result of what we see as the mismanagement of Australia’s post-mining boom adjustment, management that has a lot more to do with the RBA and Treasury covering its butt following a grotesque over-estimation of the durability of the boom, than it does sensible and sustainable economics.

Related and just as important is that we also see the major drivers of the commodities bust – a weakening China and yuan plus a strengthening US and dollar – being sufficient to end the global business cycle. It is due, after all, with most cycles averaging around eight years.

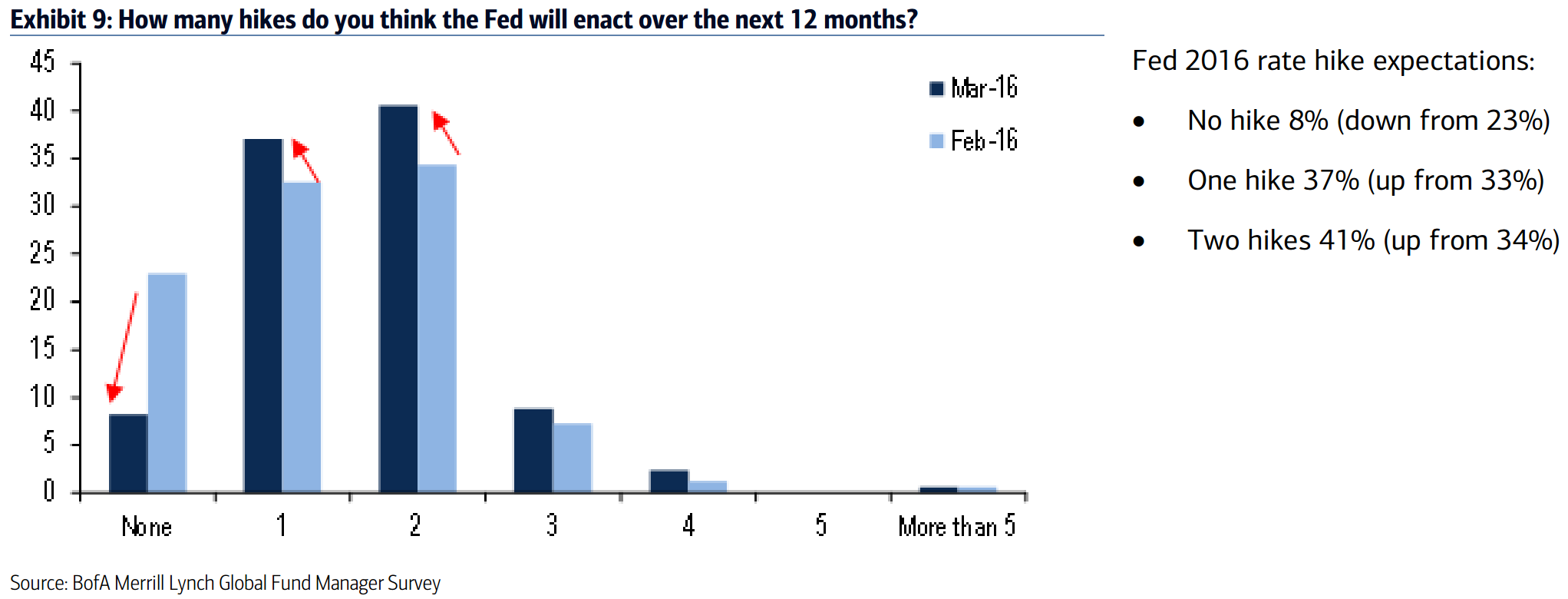

Today we have confirmation that we are very far from alone in these thoughts. From the March BofAML global fund manager survey, the Fed is tightening:

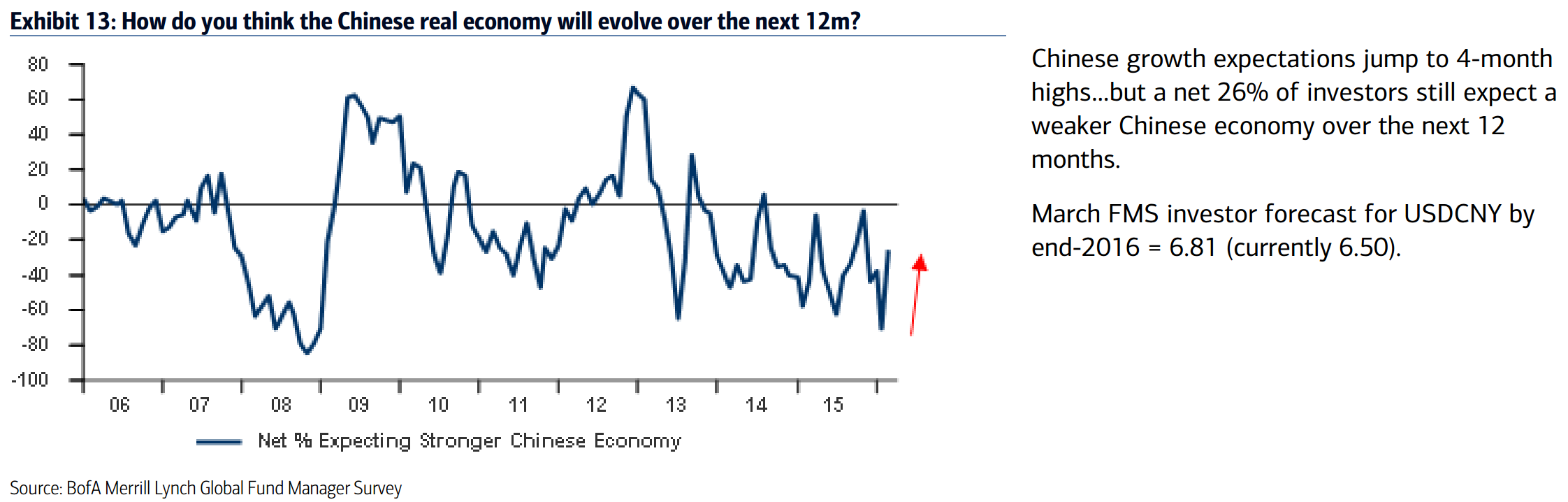

Chinese hopes are fading (in trend terms):

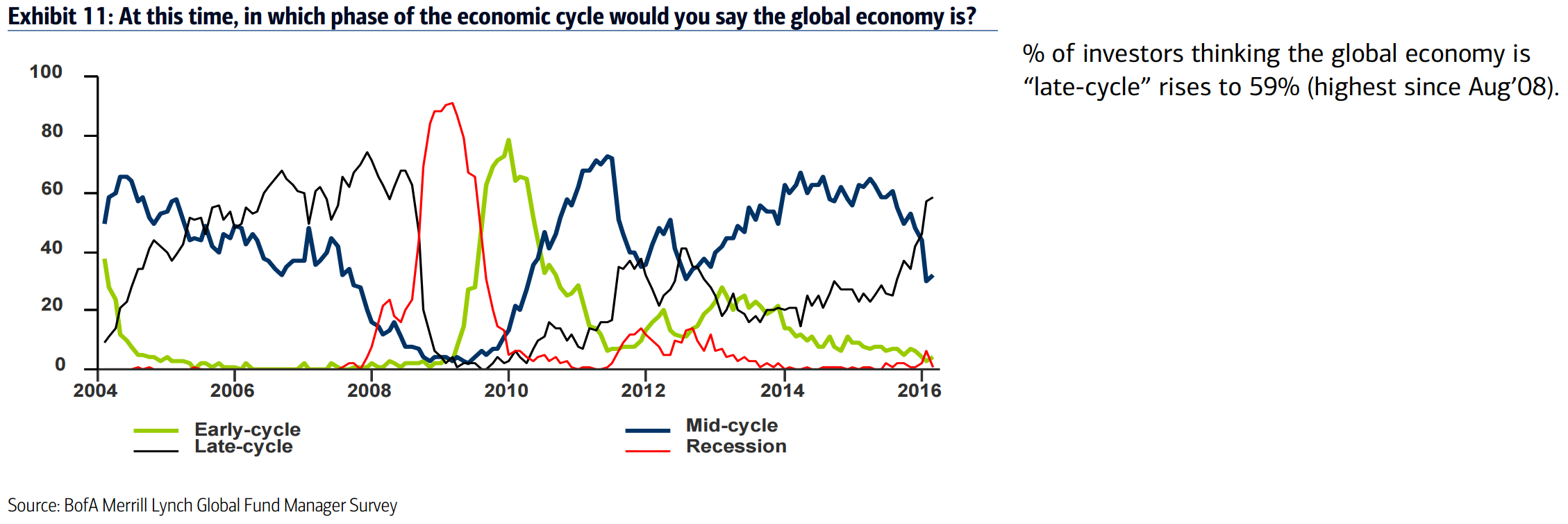

Business cycle is as “late”:

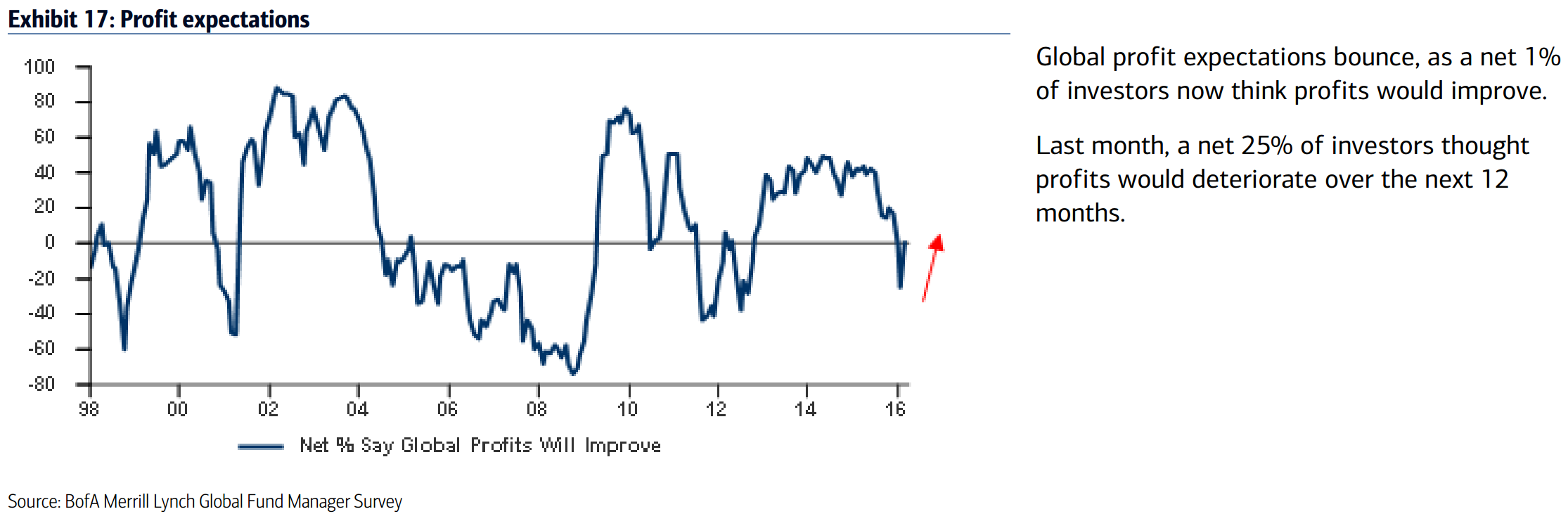

Profit expectations have cratered:

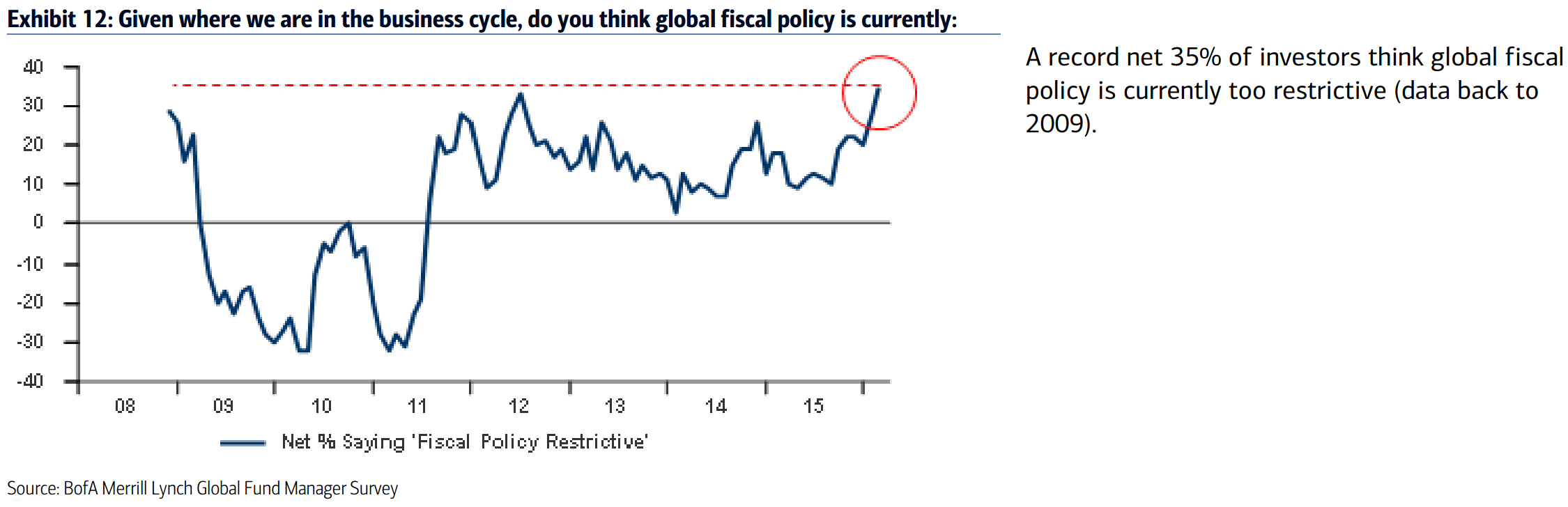

Yearning for stimulus is surging:

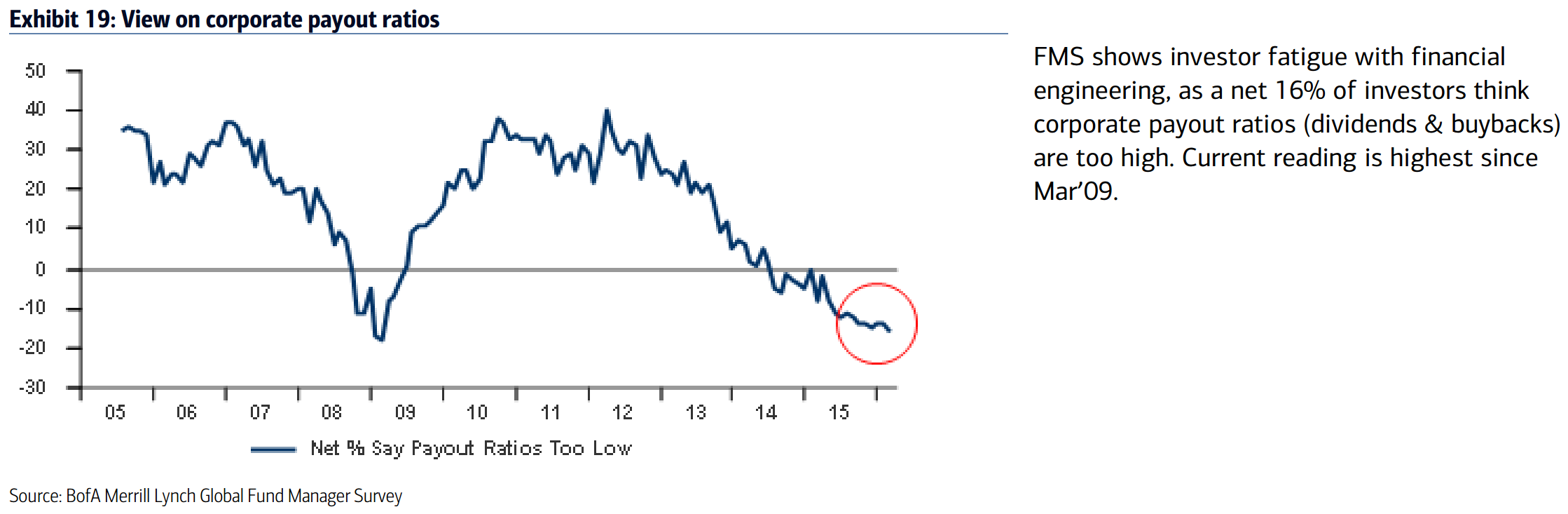

Fatigue with capital management is extreme:

It’s a business cycle very long in the tooth alright.