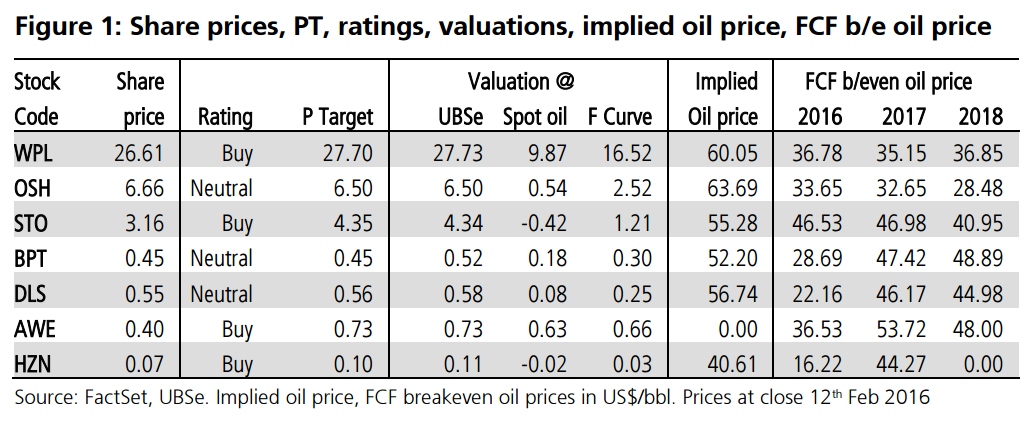

A review of E&P stock valuations, FCF break evens and implied oil prices

Oil prices remain extremely volatile, driven by both uncertainly surrounding the pace of the supply/demand gap closing and continuing macroeconomic uncertainties (China, global economic growth, USD strength). The bull case for oil price is based on: 1) 2016 will see another year of robust demand growth (1.1-1.3 mmbbl/d); 2) US shale prod’n decline should accelerate this year as drilling activity slows further, and; 3) sustained low oil prices may force some degree of cooperation amongst producers to take action on supply. The bears point to: 1) Global oversupply is currently 1.5-2 mmbbl/d; 2) supplies have been resilient in the face of lower oil prices, and this trend could continue; 3) there is downside risk to demand forecasts, given the risks surrounding the global economic outlook, and; 4) oversupply could cause key storage facilities to fill to capacity.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.