The Australian Treasury has changed the methodology that it uses to calculate the cost of superannuation concessions, which has downgraded its cost to the Budget by 30%. From The AFR:

In its annual tally of the so-called cost of tax expenditures, Treasury said the loss in 2015-16 from super tax breaks would be $29.8 billion compared to last year’s $33.5 billion, a reduction of $3.7 billion or 11 per cent.

The downgrade in latter years is even more substantial, dropping by almost 30 per cent to $32.2 billion for 2017-18, a change of $13 billion…

The superannuation industry has seized on the figures, saying they debunk claims that super tax concessions need to be pared back because they represent a growing cost to the budget.

“Contrary to what some commentators have claimed, the cost of tax concessions for super is not overtaking the cost of the age pension,” Association of Superannuation Funds of Australia chief executive Pauline Vamos said.

Okay, so the cost of superannuation concessions will only grow by 8% to only $32.2 billion by 2017-18. And this is somehow supposed to alleviate the need to take action to wind-back concessions? The Association of Superannuation Funds of Australia (ASFA) is really taking the piss now.

The fact is, superannuation concessions are costing the Budget many billions of dollars in revenue foregone. They are also growing at a solid pace.

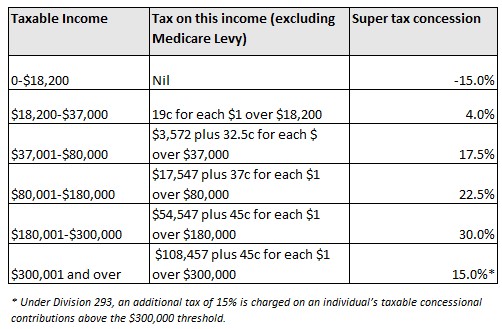

ASFA needs to explain to Australians why it is efficient and fair that the amount of superannuation tax concession received grows as one moves up the income tax scale. For example, a very low income earner earning up to $18,200 effectively pays 15% for their superannuation concession, whereas a high income earner earning up to $300,000 enjoys a 30% tax benefit (see below table).

Indeed, the Parliamentary Budget Office last year estimated that replacing the current flat superannuation tax rate of 15% with a progressive system that is closely based on a person’s marginal income tax rate would generate $10.3 billion in budget savings over the first three years, whilst still ensuring that superannuation remains a tax-effective investment for everyone. Deloitte offered a similar plan, arguing that it could save the Budget some $6 billion. How is such reform not worthwhile, even if it raises a bit less revenue than first thought?

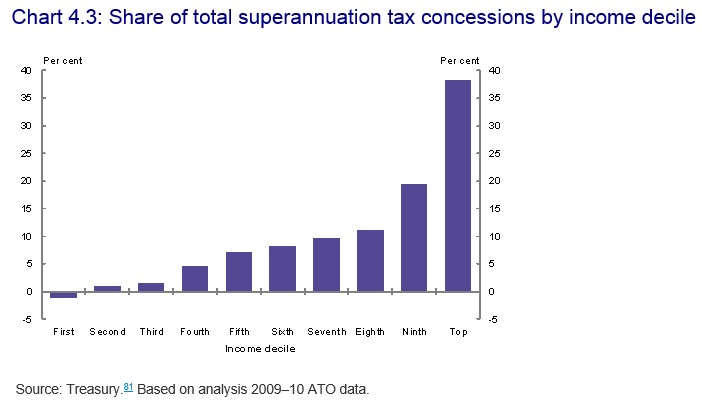

The Murray Inquiry into Australia’s financial system agreed that the system makes little sense, noting that “the majority of superannuation tax concessions accrue to the top 20 per cent of income earners (Chart 4.3). These individuals are likely to have saved sufficiently for their retirement, even in the absence of compulsory superannuation or tax concessions”.

On a related matter, ASFA should also explain why it is appropriate for those aged over 60 to pay zero tax on superannuation earnings, while workers aged under 60 must pay full tax? Take, for example, a retiree aged 61 that earns $100,000 through superannuation earnings. They currently pay zero tax. Compare this against someone of working age that earns $100,000 in labour income, who must pay around $25,000 in income taxes. How is this fair? And how does applying zero taxes on one group (over 60s) not automatically raise the tax burden on the other (workers)?

The bottom line is that superannuation concessions in their current form are both highly inequitable and inefficient, costing the Federal Budget many billions in foregone revenue whilst reducing the progressiveness of the tax system. They have increasingly become a mechanism for richer older people to avoid paying tax, rather than a genuine means for Australians to pay for their own retirement and avoid drawing on the Aged Pension.

If ASFA had any morals, it would be pushing for superannuation reform, in the interests of inter-generational equity and Budget sustainability, rather than muddying the waters.

unconventionaleconomist@hotmail.com