Deloitte financial services has offered a so-called “circuit breaker” on superannuation reform, estimating that the Budget could save $6 billion per year if super concessions were taxed at a worker’s marginal tax rate with each worker then receiving a flat rebate of 15%. From The Canberra Times:

For high earners on the 45¢ marginal tax rate, the rebate would leave them paying 30¢ in the dollar. For low earners on the 19¢ cent rate, the rebate would pay just 4 per cent. Earners below the tax-free threshold would receive a payment from the government of 15¢ in the dollar…

“We’re suggesting a truly level playing field,” Deloitte partner Chris Richardson said…

Mr Richardson said while stability was important to the super system, the system would be unstable until it was affordable and seen to be fair.

Deloitte’s proposal makes a lot of sense. It is also identical to the approach advocated for years by me, which has called for the 15% flat tax to be replaced by a 15% flat deduction, whereby every income earner would receive the same concession, thus maintaining the progressiveness of the system.

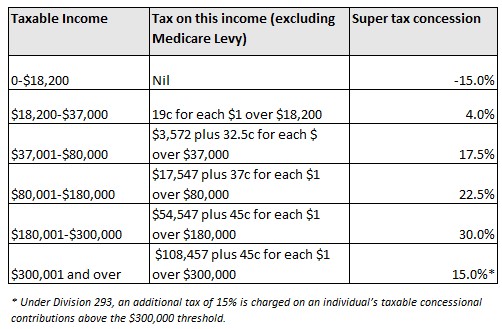

The key problem with the current superannuation concession system is that the amount of tax concession received grows as one moves up the income tax scale. For example, a very low income earner earning up to $18,200 effectively pays 15% for their superannuation concession, whereas a high income earner earning $300,000 enjoys a 30% tax benefit (see below table).

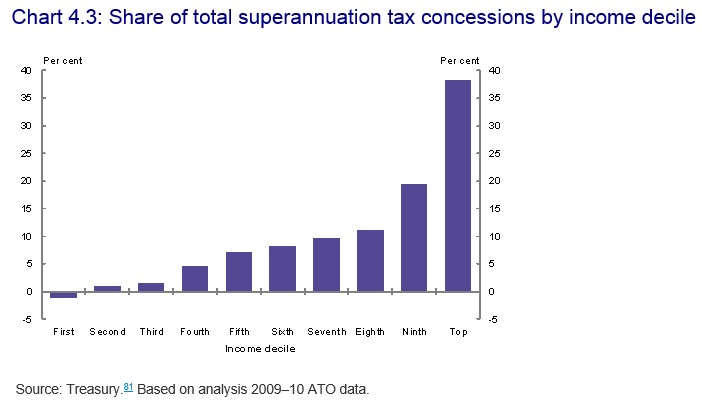

This system has led to a situation whereby the lion’s share of concessions flow to high income earners, while the poorest workers are penalised, thereby reducing the progressiveness of the tax system and blowing a big hole in the Budget (see next chart).

We already know that Deloitte’s proposal has the support of the Greens, which earlier in the year also advocated replacing the current 15% flat tax rate with a progressive system that is closely based on a person’s marginal income tax rate.

This makes super concession reform a fairly easy prospect for either of the two major parties given it would be passed in the Senate.

Put simply, it’s a policy no-brainer on political, equity and Budget sustainability grounds.