Macro newsflow in particular has been lifting hopes toward steel demand for this year. Last week we had the record new lending figures for January, registering RMB2.5tr. On Friday the PBoC raised the RRR for some larger banks to stem the surge in new lending, but it is still speculated in the market that new lending figures would continue to be elevated in February, and our economic team does not believe the monetary policy has turned tighter (see here).

In addition, further loosening measures toward the property market have raised hopes that housing construction will be better supported than previously feared. Over the last 12 months, down payment was halved to 30% for second-home purchases (cut from 30% to 20% for first home); deeds tax chopped off 2 percentage points to 1%, and business taxes went to zero. The latter two are the lowest ever. Our property team has raised their 2016 national floor space sales growth forecasts from single digit to 15%.

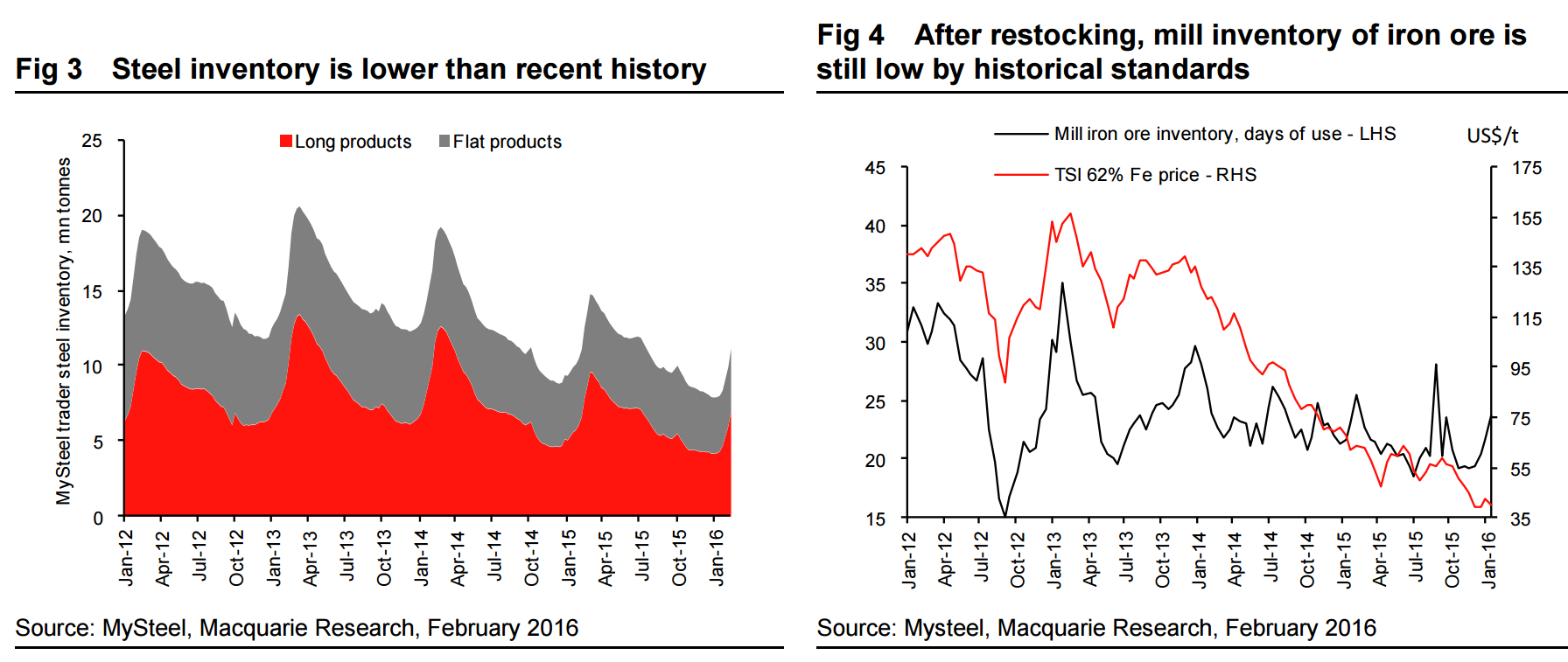

With demand expectations improving and steel inventory low, steel prices should continue to do well. While steel mill margins improved by about RMB50–150/t from November to January, capacity utilisation at steel mills had not responded before the Lunar New Year given tight financing conditions and seasonally weak demand. That said, mills were planning to resume production after the holiday – as we visited Tangshan in late-January, the local talk was that a few mills already shut down were looking to rely on private funding to turn on their blast furnaces after the CNY. Besides the better margins, a potential seasonal pick-up in orders seems to be another reason for their heightened interests in producing steel again.

If steel prices continue to run and mills look to lift steel production, this could lead to a scramble for iron ore restocking. There was minimal restocking of iron ore at steel mills prior to the New Year holiday, as in terms of days cover this was also flattered by the lower steel production rates in December and January. Port inventory of iron ore appears to have peaked around 90mt for the moment in December, and we would expect this volume to decline as iron ore imports slow seasonally due to weaker shipments out of Australia and Brazil from January.

Very much as MB has been describing. In my experience the Macquarie team are excellent on internal market dynamics and are usually too bullish on the Chinese economy. The fundamental problem is that floor space sales and floor space under construction have dislocated owing to the glut in lower tier cities so that is the fatal flaw in this argument. It really doesn’t matter if China sees strong growth in property sales if it does not trickle down to third and fourth tier cities which constitute 75% of construction and which are massively over-built. Present indications are that Chinese floor space started will fall 15% this year.

In short, I do not see iron ore going much higher than today and as the property and manufacturing recession bites into steel consumption all year it should roll over and hit deep new lows.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.