There’s plenty to choose from but this one is convenient, from the inappropriately titled The Evolving Risk Environment speech yesterday:

…the hypothesis that falling equity and falling oil prices are inter-related responses to a weakening in global demand is hard to sustain. The falls in oil prices seem to be mainly driven by strong supply, not weak demand, as indeed has been the case for a number of other commodities such as iron ore. Consistent with that, other non-energy commodity prices have been relatively stable during this recent period when oil prices have continued to fall. This has important implications for the general outlook. While an oil supply expansion could be expected to have a range of complicated effects on producers, consumers and holders of energy assets, it would normally be considered a net positive for the world as a whole.

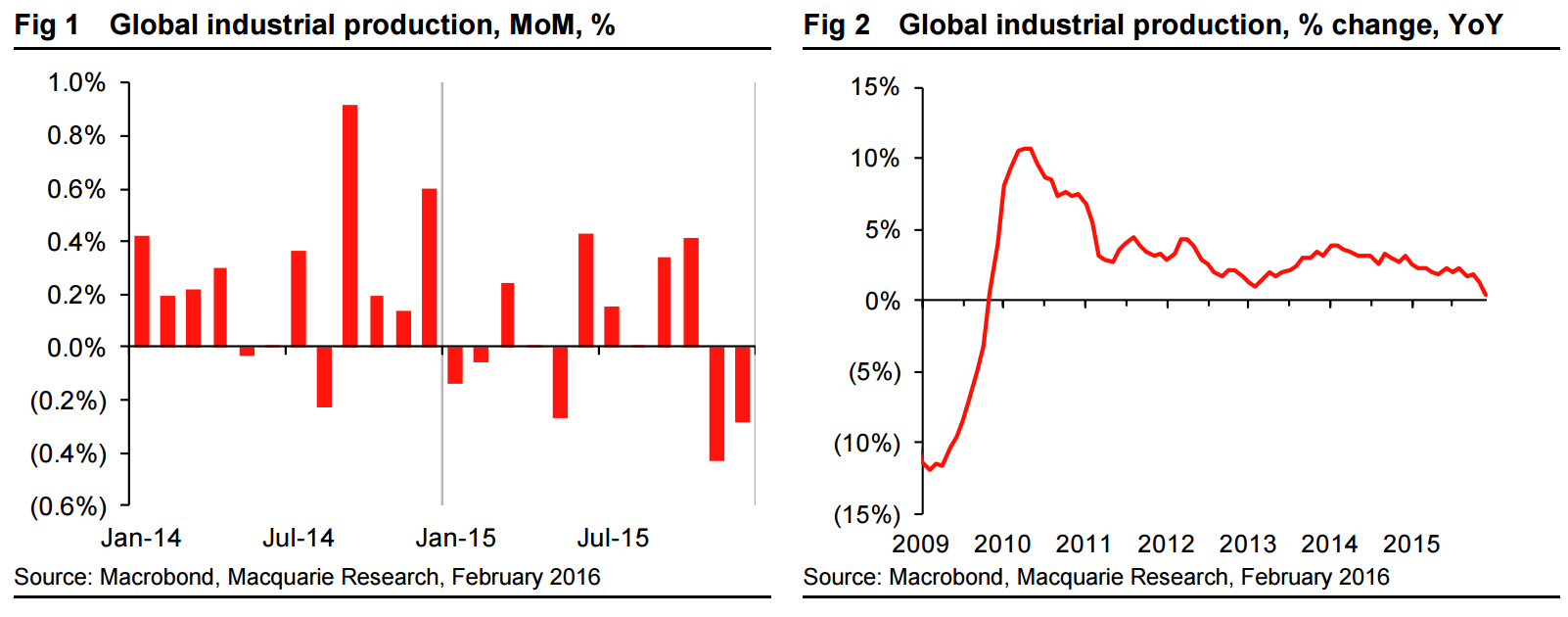

Aaaand the truth via a Macquarie chart:

Global industrial production, a key driver of commodity demand, fell MoM in December for the second consecutive month, leaving it barely higher than a year earlier. This takes Chinese data at face value – if you believe they even moderately overstate growth then we are facing a global industrial recession. Cyclically things should get better; the concern is a structural slowdown.

Never let the truth get in the way of good confidence fairy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.