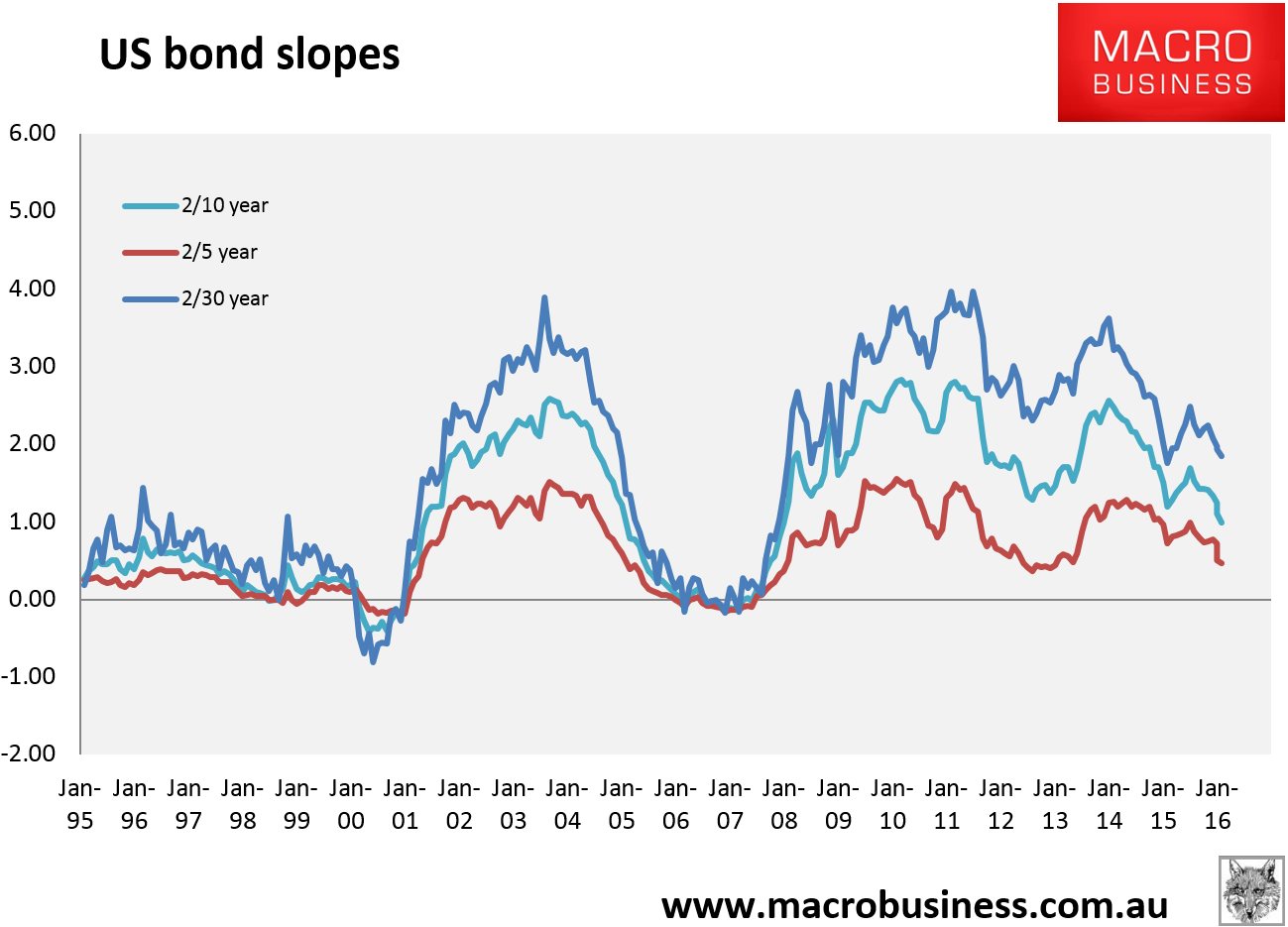

We all know that the Fed has made a policy error in hiking rates in December as its bond market curve continues to collapse presaging a growth accident:

But if you’re looking for a quick u-turn then history is not on your side according to Goldman:

There is nothing inherently wrong with policy reversals. If the growth or inflation outlook were to deteriorate meaningfully, optimal policy might call for a lower funds rate, even shortly after an increase. In Exhibit 2, for example, we show the implied cumulative probability of a cut using the Fed’s large-scale macroeconomic model, FRB/US. In this exercise, we use the median forecast from the FOMC’s Summary of Economic Projections (SEP) as the baseline for the simulations, and then allow FRB/US to draw shocks that are calibrated to the economy’s realized uncertainty over the last twenty years. We then calculate the path of the funds rate in each simulation using Chair Yellen’s preferred version of the Taylor rule, the economic outcomes from the simulations, and an assumption that the neutral rate either remains flat at zero or normalizes gradually at the rate implied by the FOMC’s “dot plot”.