Did CBA just form the mother of all chart tops?

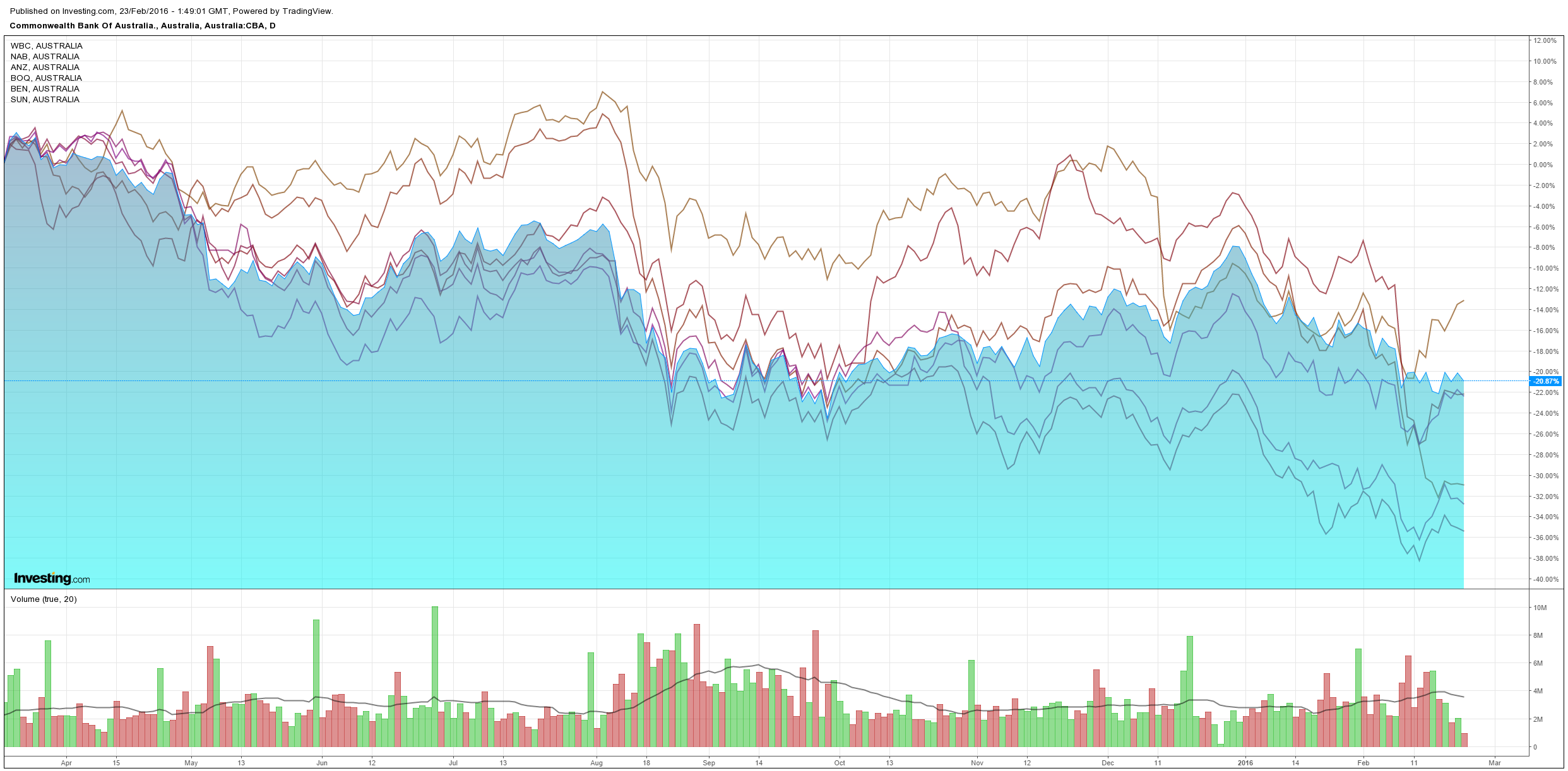

The screaming dead cat bounce of the last few days is finding resistance today as key prices weaken. Banks are down with CBA -1.2%, WBC -0.9%, NAB -0.7%, ANZ -0.5%, BOQ 0.45%, SUN flat, BEN -0.3%:

Homing in on CBA we see an unsettling picture emerging. Here’s the monthly chart:

I’m not going to hurl myself off a cliff or anything but that looks awfully like the mother of all “head and shoulders” tops forming. Technicals are useful for entry and exit signals mostly so I wouldn’t take this to the bank (at it were) but when you combine a strong pattern with a matching fundamental picture (bearish or bullish, in this case Australia’s deteriorating outlook) then it’s pretty powerful stuff. Any break below the neckline zone around $72 on that CBA chart will be a very bearish signal. As texture for this, the age old bank defenses are going up at the AFR:

Foreign hedge funds are talking up a collapse in the local housing market and taking short positions in the big four banks, but their enthusiasm is misplaced, Aurora Funds Management says.

Hedge funds have stepped up their positions in the “widow-maker” trade of short-selling Australia’s banks, anticipating falls on the back of what they see is a housing bubble due to burst.

Short-sellers have enjoyed some success, with the share prices in the big four falling between 20 and 30 per cent since capital requirements sent them tumbling from at or near record highs last April.

Yet the housing market isn’t in crisis, despite the hedge fund doomsaying, Aurora senior portfolio manager Hugh Dive said.

“Whilst Australian housing can be viewed as expensive globally, we see a range of factors that strongly encourage Australian households to maintain mortgage payments,” he said.

“These include recourse lending, homes are exempt from capital gains tax and strong cultural desire to own one’s own home.”

All very tired. We all know that the Australian housing market is a gigantic imbalance. The only question is what would force it to adjust? For my money that is authorities running out of ammunition to prevent it, and yes, I believe we are entering such a period.

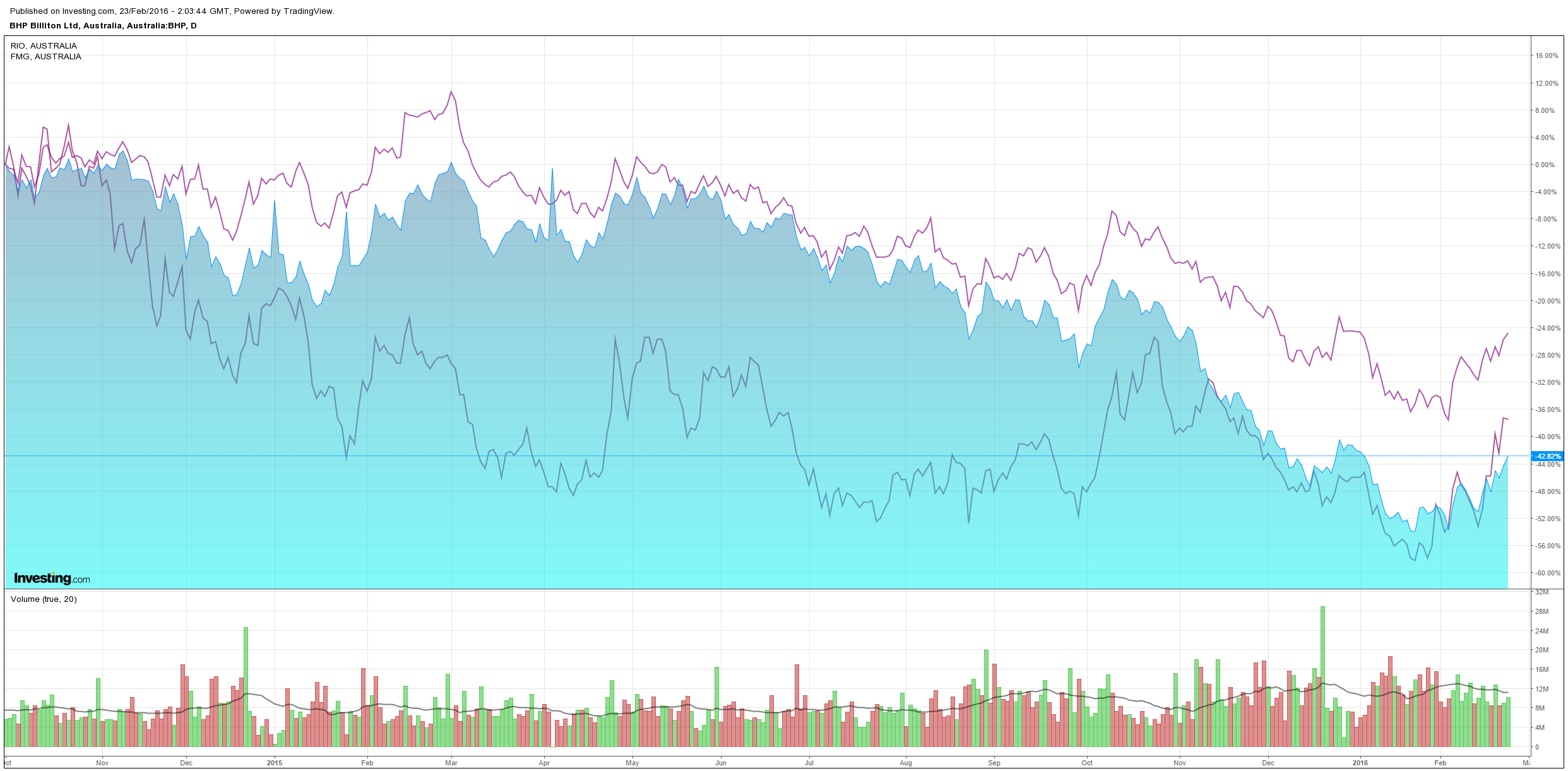

Turning to iron ore, Dalian has flamed out at the open shedding last night’s big gain. Even so, BHP is 2.5% up despite puking on investors, RIO 1.2% and FMG -0.7%:

Is this a buy signal? From Trevor Sykes:

BHP changed its dividend policy and slashed the interim payout by 75 percent – from US62¢ to US16¢.

There could be even worse to come, because board policy is for future dividends to be a minimum of 50 percent of underlying attributable profit.

If the board had adhered to that policy on Tuesday the interim dividend would have been only US4¢.

BHP’s December half figures were an even worse shocker than the market had been expecting.

The good news is that this is probably as bad as it gets.

…Overall, BHP will survive and everything it produces will probably start rising again in the long term.

Not entirely encouraging because, as Lord Keynes famously observed: “In the long term, we are all dead.”

It’s tempting to see Sykesnado capitulation as a buy signal but I don’t think so. Nothing in the global economy is fixed yet and thus commodity prices will turn lower soon enough. The BHP chart is far from out of the woods.

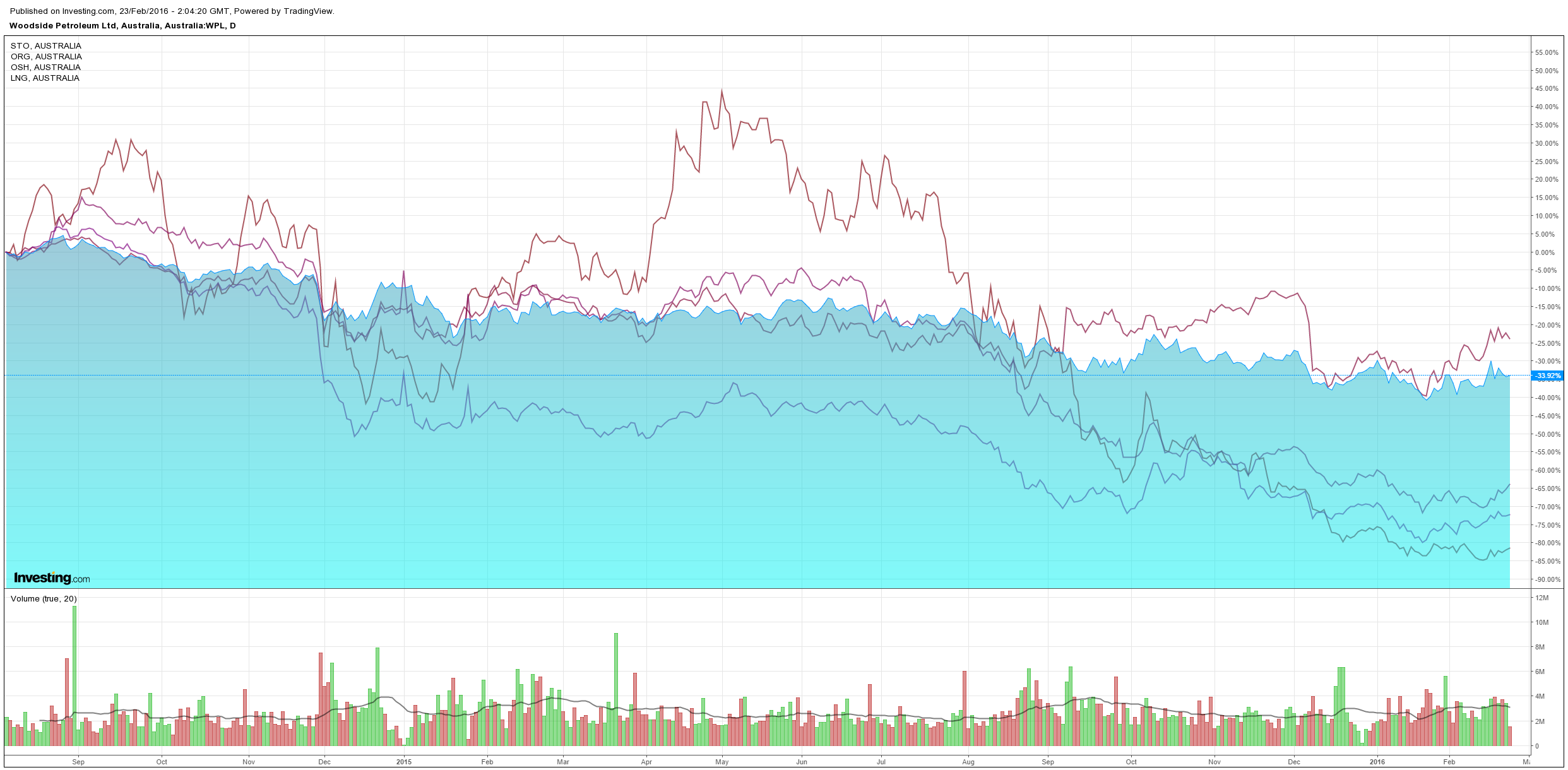

Big gas is mixed as oil fades with WPL flat, OSH -2.5%, ORG 3.5%, STO 1.2% and LNG 3.2%:

Not surprising we’re seeing some exhaustion after the lunacy.