Brent oil eased again Friday night to $34.13 and Henry Hub firmed a little:

The action was despite a renewed plunge in the US rig count down down -31 to 467.

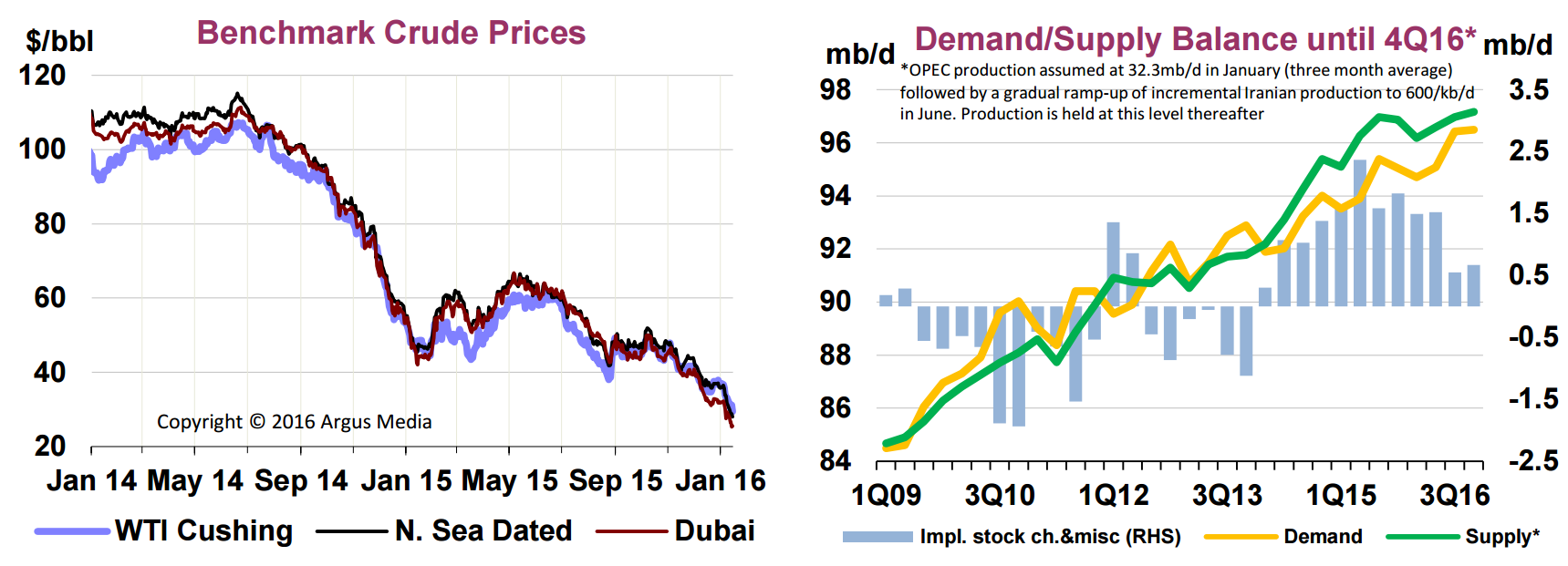

So, with rigs plunging again, where are we on the market balance question? The IEA’s January Oil Market Report is now available to the public and sees it this way:

Advertisement