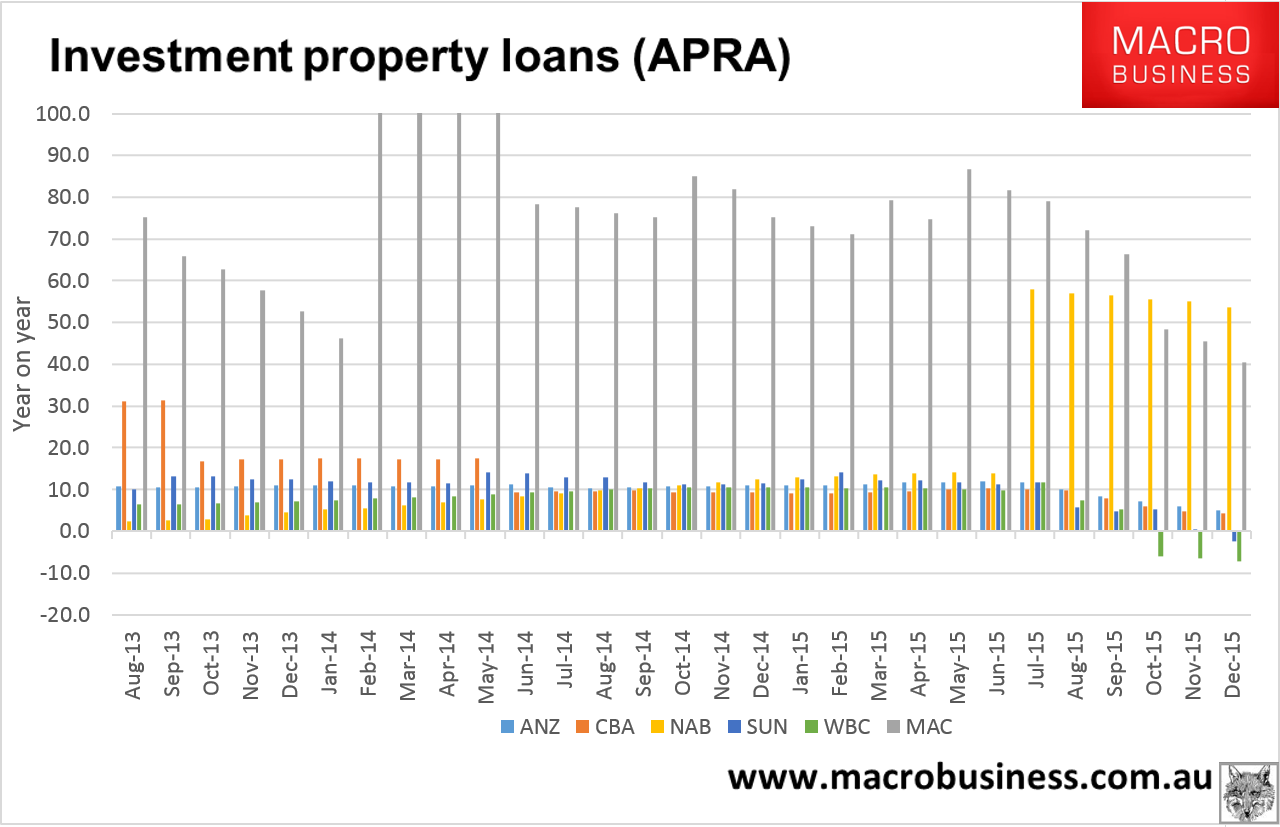

Glenn Stevens for one. Yet today’s credit data slaps him square across the face. APRA’s December bank breakdown has investor loans stalling out completely in annual growth rates:

| ANZ | CBA | MAC | NAB | SUN | WBC | |

| Dec-15 | 5.0 | 4.2 | 40.6 | 53.7 | -2.5 | -7.2 |

| Nov-15 | 6.0 | 4.9 | 45.5 | 55.1 | 0.5 | -6.4 |

| Oct-15 | 7.1 | 6.1 | 48.5 | 55.6 | 5.2 | -6.0 |

| Sep-15 | 8.4 | 7.9 | 66.3 | 56.6 | 4.8 | 5.2 |

| Aug-15 | 10.2 | 9.7 | 72.0 | 57.0 | 5.6 | 7.3 |

| Jul-15 | 11.7 | 10.1 | 79.1 | 58.0 | 11.7 | 11.7 |

| Jun-15 | 12.0 | 10.2 | 81.6 | 14.0 | 11.1 | 9.9 |

| May-15 | 11.8 | 9.9 | 86.8 | 14.1 | 11.6 | 10.0 |

| Apr-15 | 11.7 | 9.5 | 74.8 | 13.9 | 12.1 | 10.3 |

| Mar-15 | 11.4 | 9.3 | 79.3 | 13.6 | 12.1 | 10.4 |

| Feb-15 | 11.1 | 9.2 | 71.0 | 13.3 | 14.1 | 10.2 |

| Jan-15 | 11.1 | 9.2 | 73.1 | 13.0 | 12.5 | 10.4 |

| Dec-14 | 10.9 | 9.4 | 75.2 | 12.4 | 11.6 | 10.5 |

And in chart form:

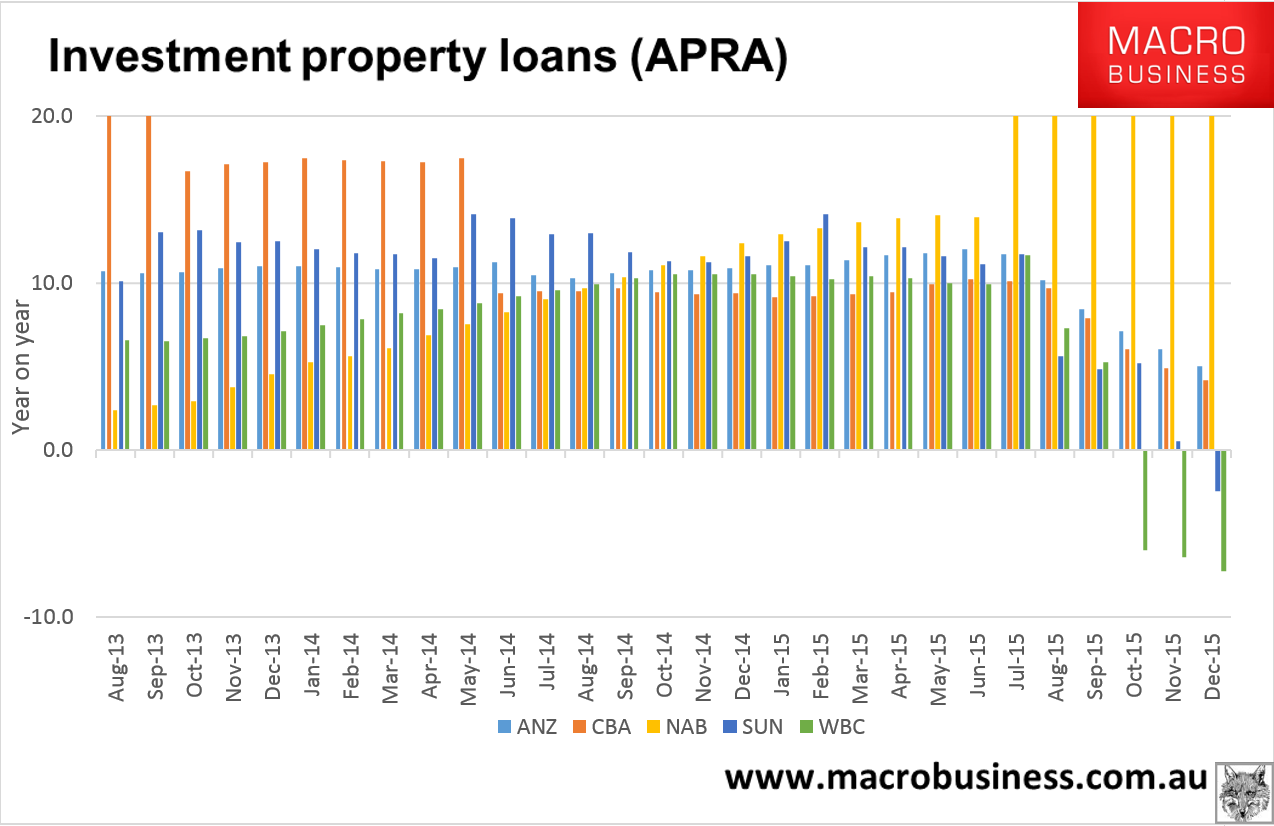

And closer up without MQG distorting the chart:

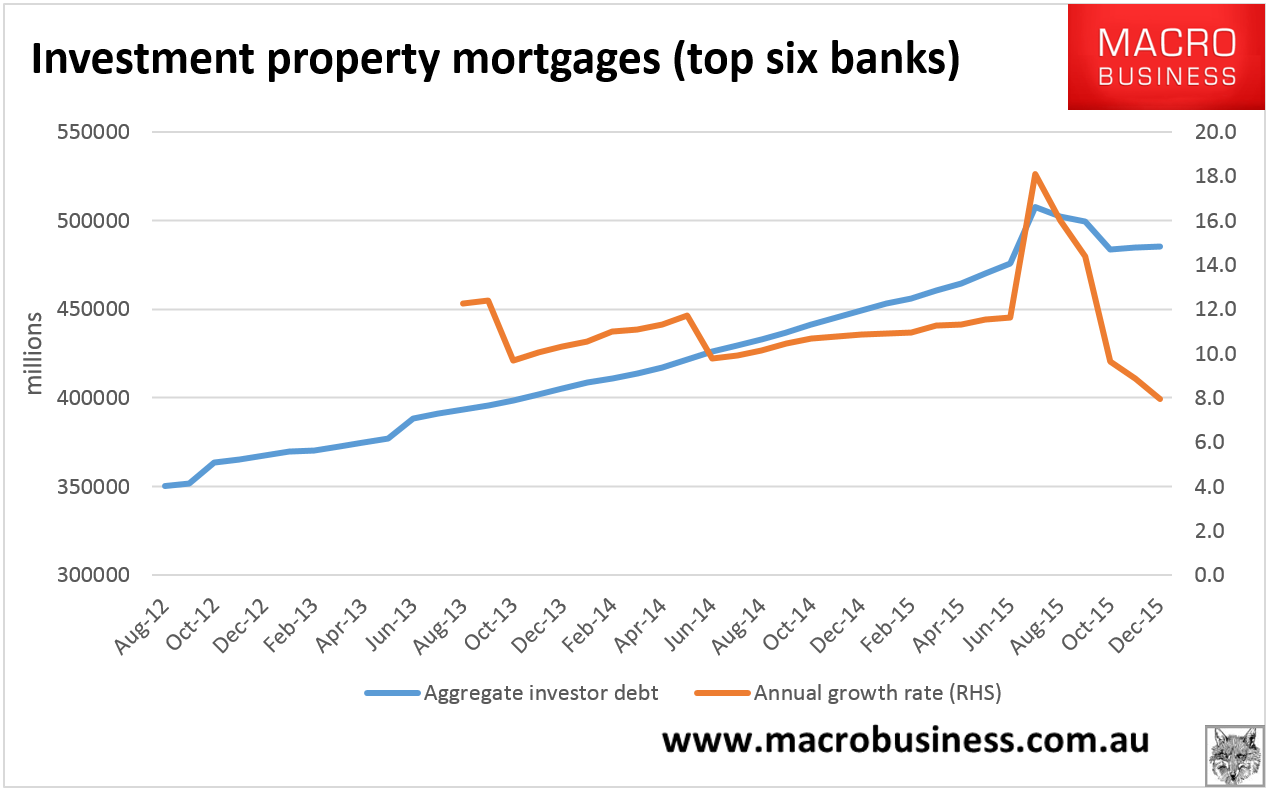

The big WBC falls and NAB rises are mortgage portfolio re-allocations and I accept that this data is distorted by such activity. Even so, other banks have been relatively unaffected by such bulk mortgage swaps and check out the deceleration. Here’s the total of the top six banks charted against the annual growth rate:

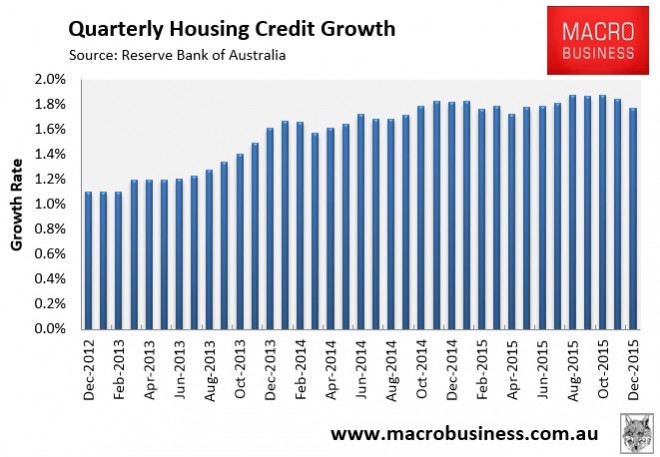

There is some switching going, as is obvious in the RBA’s credit aggregates today, but it is also clear that the growth rate has plunged below APRA’s 10% annual threshold:

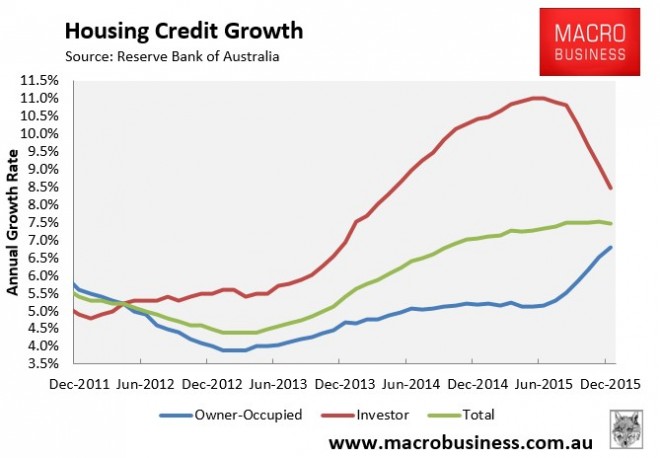

It is also clear that macroprudential has nicely tapped the breaks on the bubble without a rate rise:

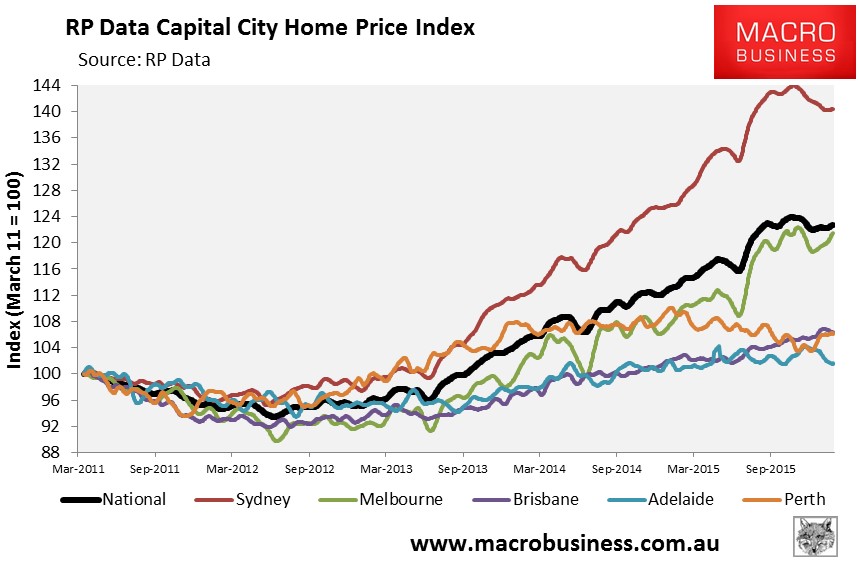

Flat-lining the runaway Sydney and Melbourne bubbles:

It should have been done three years earlier. The dollar would be at 55 cents now and would have been much lower throughout the commodities bust. Rates would be at 1.5% or lower. The Budget would be much better positioned with materially greater protection from the lower dollar across the period. House prices would be growing with income. Consumers would still be moving along. The residential building boom would still have happened. But growth would be more driven by tradables as we whipped the world in commodity market share with a services and agriculture tradables rebound that had a three year head start.

Instead we got this lunacy charging straight into a Mining GFC:

So, what idiot said macroprudential would never work? Pretty much all of the RBA hosed the idea from 2012. The good captain must shoulder the blame.