Today’s research note from Elliot Clarke at Westpac puts the multi factor risks and problems the Fed face going into 2016 into focus. Westpac is still eyeing four interest rate hikes this year – which would send the USD into the stratosphere and emerging markets into the pits of hell.

On the one hand, core inflation is near-enough to its medium-term target and employment continues to experience strong growth, justifying multiple hikes in the year ahead. Against this however, market participants are focused on the many risks, believing instead that the FOMC will (at most) only raise rates once in 2016.

Starting with the real economy, while Q4 now looks set to post annualised GDP growth of 1.0% or below, this has more to do with reduced inventory accrual in the quarter than the strength of end demand. The drag from net exports is also not a major concern for the FOMC at present, with firmer global growth to help (in time).

Focusing then on domestic demand, underlying momentum is robust. Annual growth is expected to remain healthy around 2.5% in Q4 and should then firm back to 3.0% in 2016. This will be supported by continued strength in consumption and a greater willingness amongst firms to invest in real capacity.

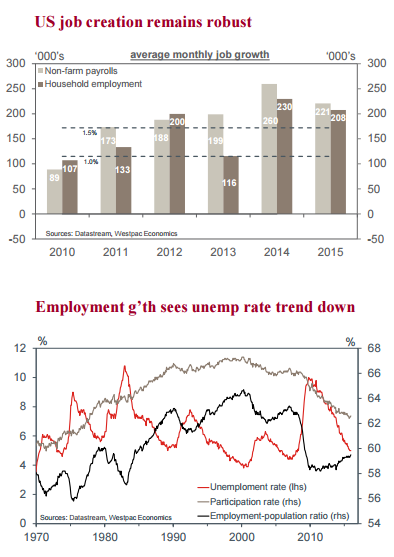

The robust outlook for the consumer that we and the FOMC hold is built on persistent employment gains. Simply, at 1.9%, annual nonfarm payrolls growth continues to print well in excess of labour force and population growth, which are both nearer 1%. This divergence between job and labour force growth has now driven the unemployment rate down to 5.0%. A continuation of this trend will see the unemployment rate below its full-employment level in 2016 and (theoretically at least) produce a build-up of wage pressures. Low unemployment; strengthening wages; and historically low oil prices should give strong support to discretionary spending amongst main street USA (despite equity market losses).

That then brings us to inflation. On both a CPI and PCE basis, there are strong core inflation pressures emanating from housing. This is primarily a function of rapid growth in rents, which has become an enduring force in recent years. Price gains for insurance and health are another key part of the core inflation trend.

Policy guidance from FOMC members clearly places the onus on core inflation pressures not headline as the latter continues to be impacted by temporary disinflationary distortions that will revert in 2016. To look through these distortions, Chair Yellen’s late-2015 estimate of “underlying” inflation is helpful: at 1.50–1.75%, it is near-enough to the medium-term target to push forward.

This leaves the ‘wildcard’ policy considerations: the global economy and financial markets. At the December meeting, Committee members took a constructive view, noting that “downside risks to U.S. economic activity from global economic and financial developments, although still material” were believed to have “diminished since late summer”.

A month on, it is much more difficult to make such a statement. But solely considering the impact of global angst on US financial markets to date, there is arguably not (yet) justification to ignore the robust real economy signal and hold fire on further rate hikes pending market calm.

All things considered, we remain of the view that the FOMC is intent on focusing on the real economy when determining policy. On the basis of the information to hand, we still expect four rate hikes in 2016, well in excess of market expectations.

For us to alter this view would require: the FOMC to materially upweight the importance of ‘transitory’ disinflation and/or the implications for the US of global market developments; and/or evidence of an abrupt slowing in domestic demand. Some instability during normalisation is inevitable; while confidence in the FOMC is on the line.