The perversity of the Chimerican unwind is on display again today as an excellent US jobs report is only more fuel tossed upon the Mining GFC bonfire. Friday night’s BLS report was excellent and well above expectations:

Total nonfarm payroll employment rose by 292,000 in December, and the unemployment rate was unchanged at 5.0 percent, the U.S. Bureau of Labor Statistics reported today. Employment gains occurred in several industries, led by professional and business services, construction, health care, and food services and drinking places. Mining employment continued to decline.

… The change in total nonfarm payroll employment for October was revised from +298,000 to +307,000, and the change for November was revised from +211,000 to +252,000. With these revisions, employment gains in October and November combined were 50,000 higher than previously reported.

…In December, average hourly earnings for all employees on private nonfarm payrolls, at $25.24, changed little (-1 cent), following an increase of 5 cents in November. Over the year, average hourly earnings have risen by 2.5 percent.

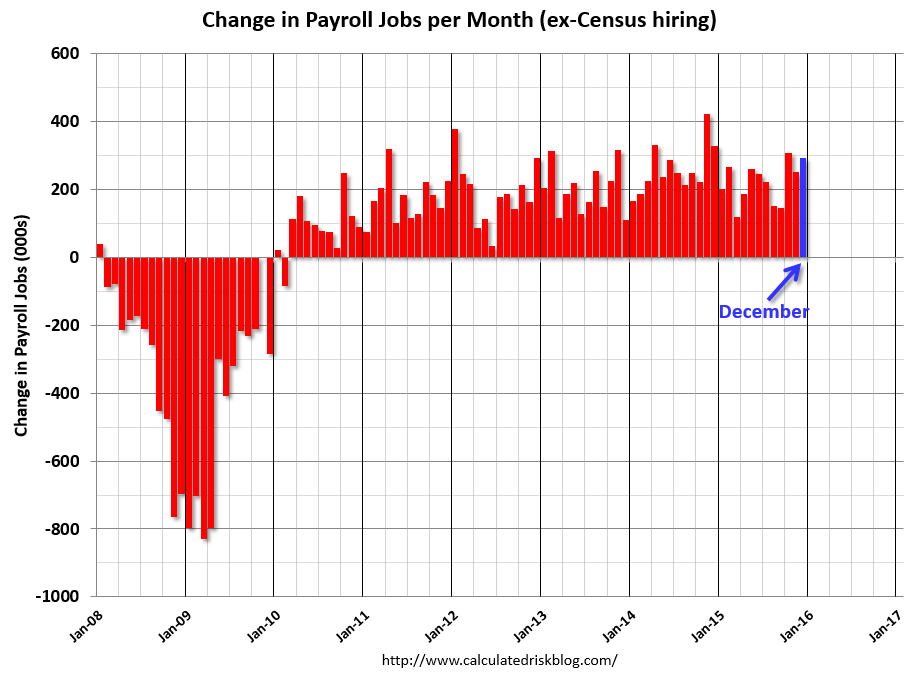

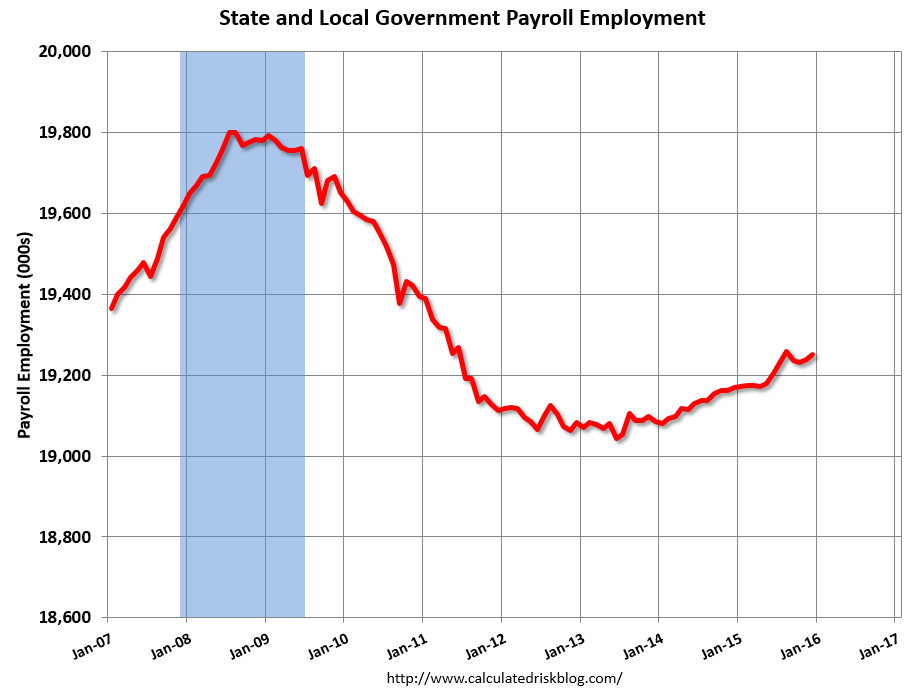

Here’s the headline number (charts from Calculated Risk):

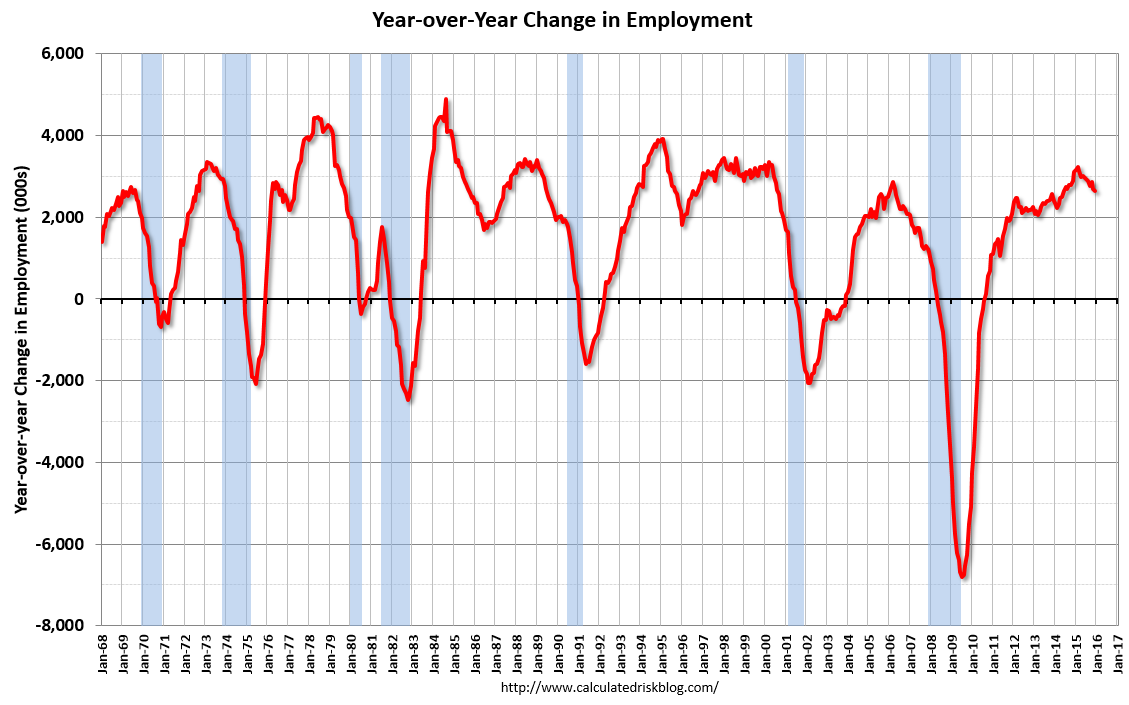

The annual rate of growth is sliding but solid:

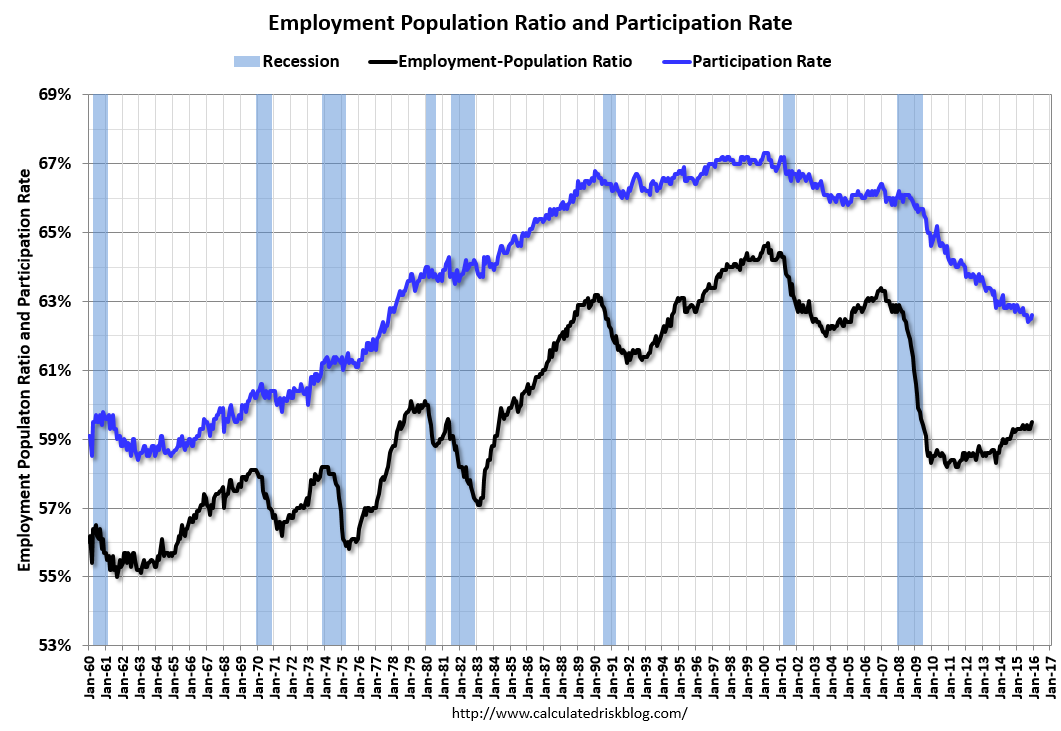

Analytical series are still mixed:

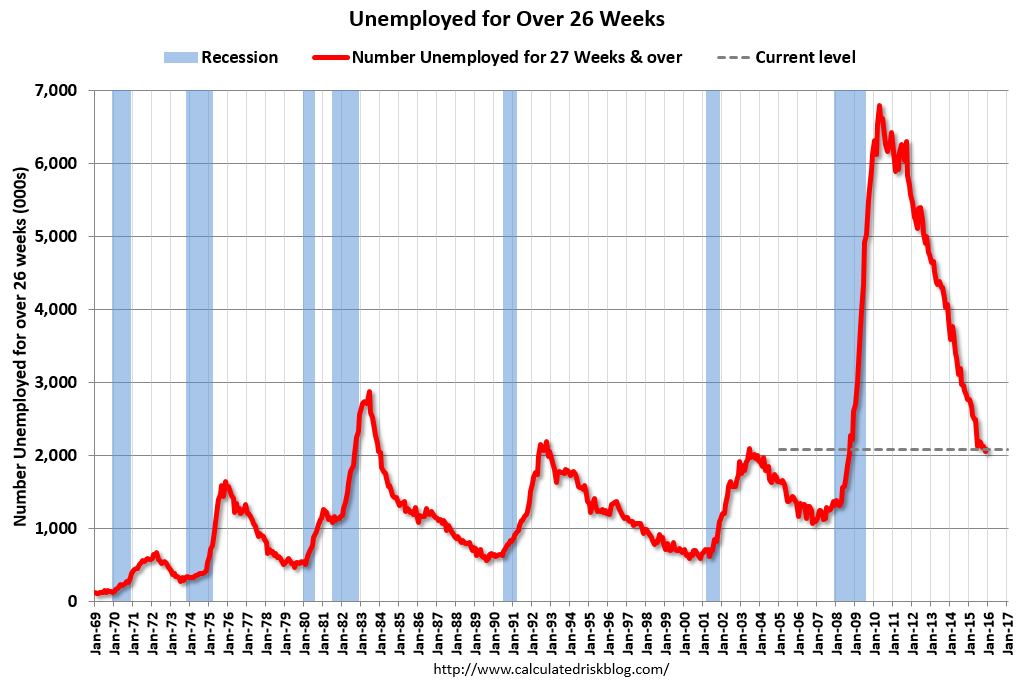

Shadow slack is again falling:

But has plenty of room yet:

‘

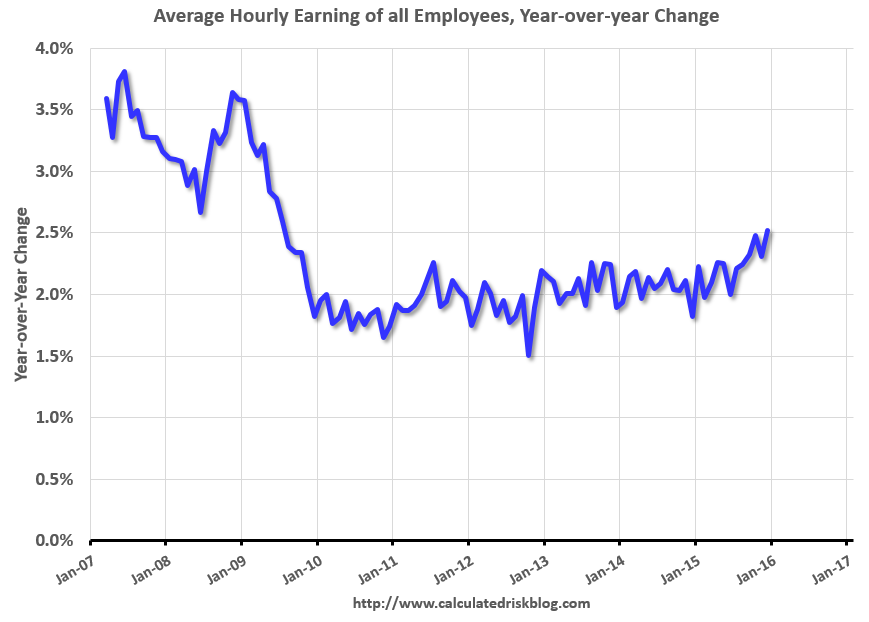

‘ And wages growth is finally trending slowly up:

It’s a very good report indicating a solid labour market.

Markets hated it with stocks hammered another 1%. This goes beyond “good news being bad news” because it suggests more US rate hikes. If we recall the very unusual set up in global macro right now, more US jobs exacerbates the building business cycle-ending accident that MB calls the Mining GFC. Rising US interest rates places upwards pressure on the US dollar, which rebounded on the night:

That in turn pressured oil again:

And hit base metals:

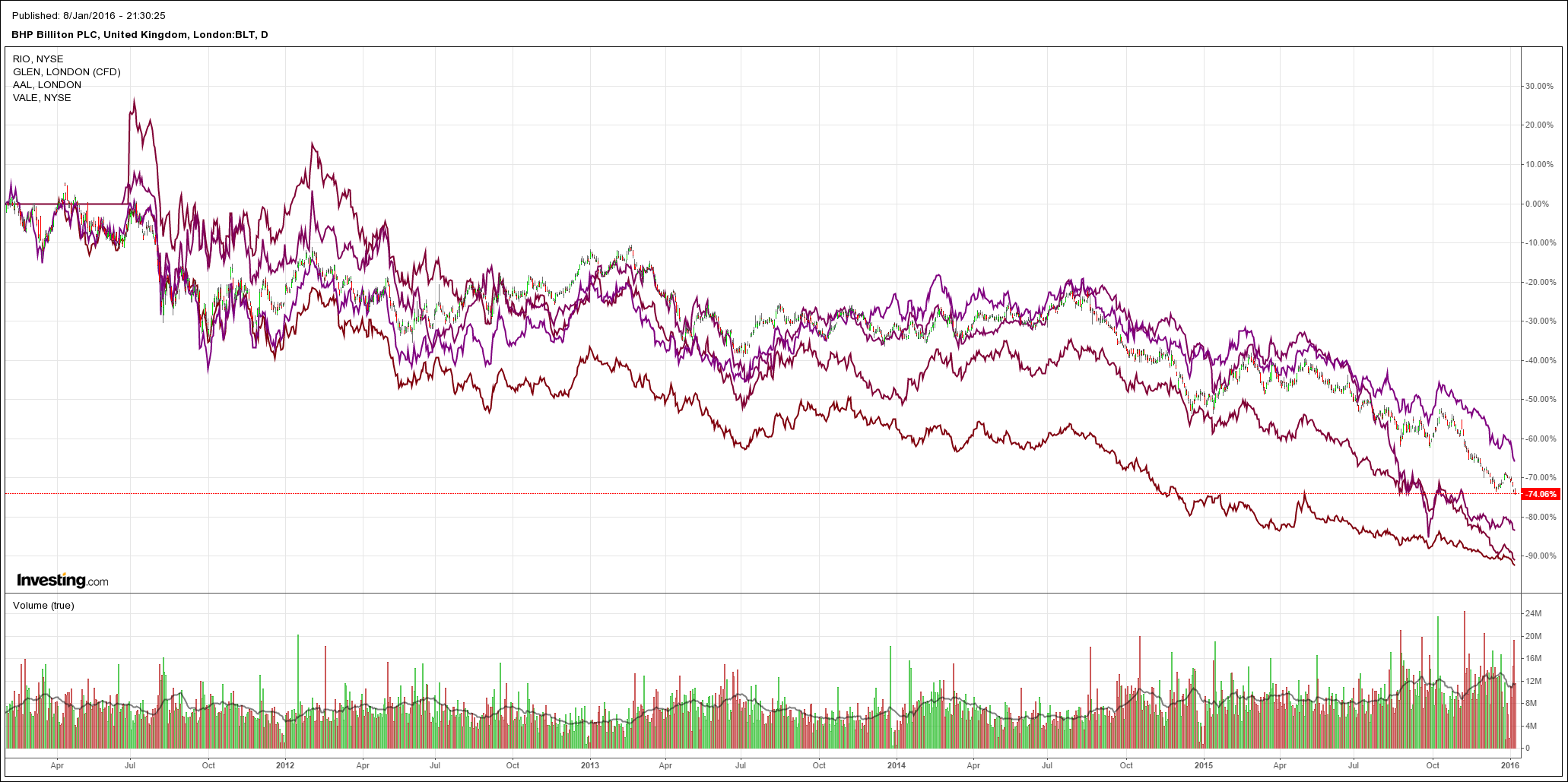

Which hammered big miners:

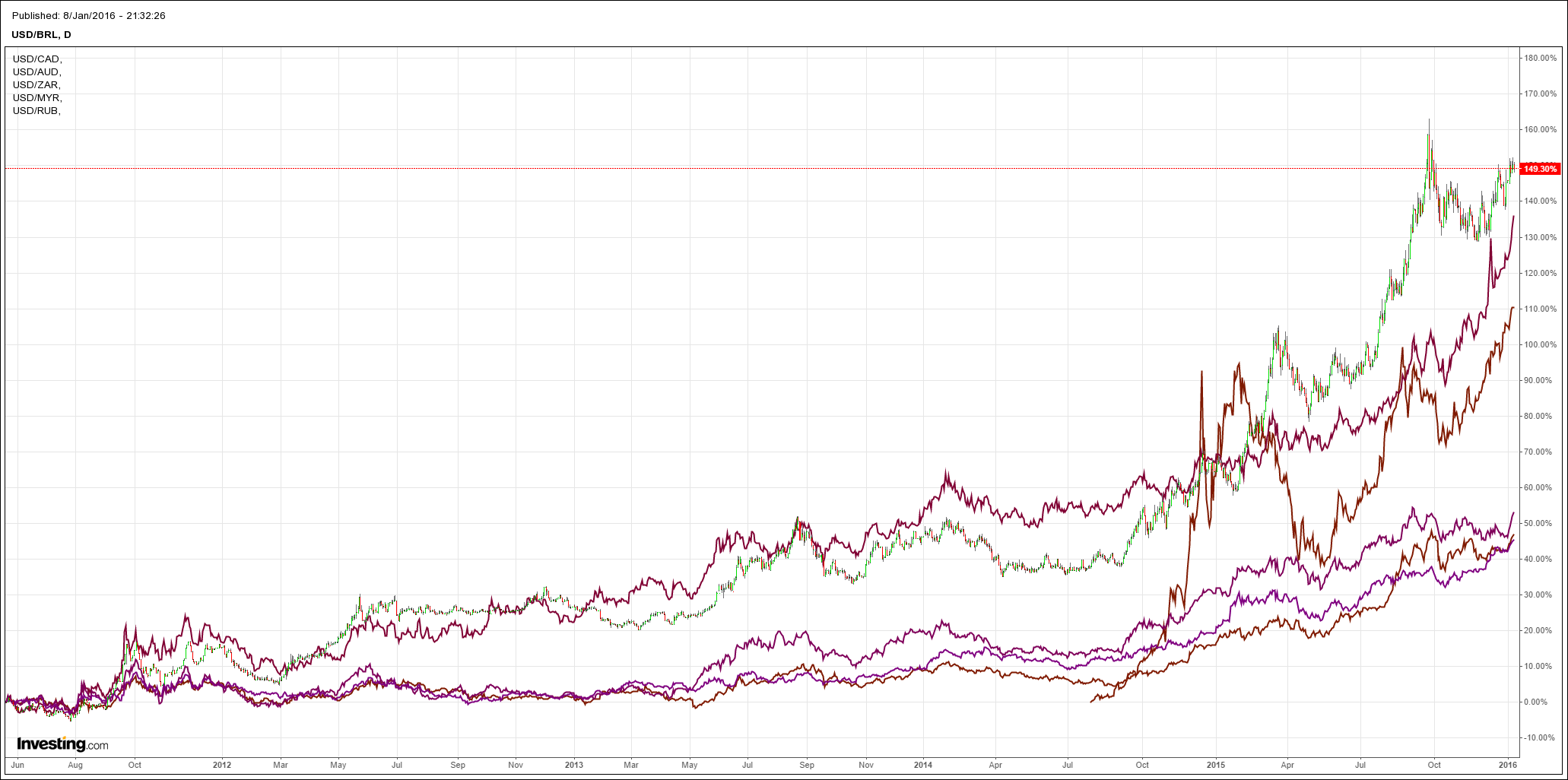

And smashed commodity currencies:

Hitting high yield and emerging market debt again:

The stronger the US economy gets, the weaker everywhere gets as the commodity super cycle unwinds all the quicker. An unusual cycle indeed!