The Chinese New Year will be upon us in a few weeks, plus a week long Spring festival that has the dual effect of clearing some air pollution but also possibly giving some relief to risk markets.

Not so for iron ore though, as Chinese steel mills rebuild inventory, with ANZ out today reckoning that spot prices will come under more pressure.

From AFR:

The key reason for the expected price drop is their forecast for increased steel output in China after local New Year holidays, the analysts wrote in a comment published late on Tuesday.

“We believe inventory levels will rebound strongly after the third week of February (post the Chinese New Year), once steel mills return to normal production rates. Weak domestic demand and rising trade barriers will further aggravate the demand situation and reduce the buying interest in iron ore,” the analysts said. “This should see iron ore prices test the recent low.

“In fact, we expect prices to remain weak throughout Q1 2016, ranging between $US35-40/tonne. However, the probability of prices breaking below this range in the short term is rising daily.”

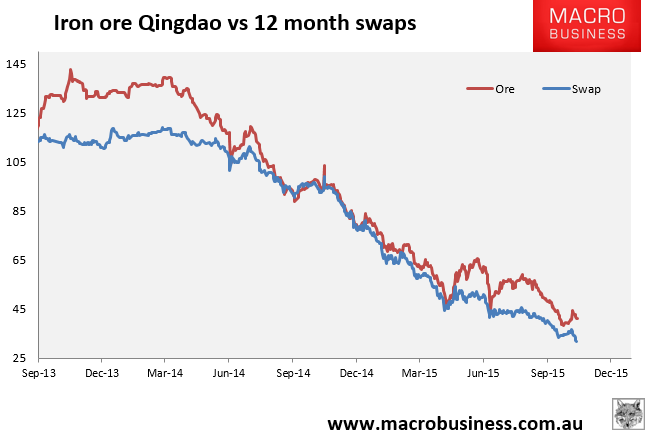

Indeed. The Western New Year saw a rally in iron ore price, with a bottom just above $38USD per tonne, but that has been almost retraced with the latest market volatility as we get back on trend.

Macquarie Research adds to the malaise with a “weak start” for exports, especially Brazil which last week exported the least since mid-February 2013:

Meanwhile, Rio’s shipments from Dampier look to have been the lowest since mid-August, at an annualised rate below 300mtpa. Q1 is seasonally weak for exports, with Australia and Brazil volumes often down 10-15% QoQ, however there has been no notable weather issues affecting last week’s performance

Port Hedland cargo statistics however, show a huge increase with a near 8% expansion for the total year in 2015 – around 446 million tons, vs 413 in 2014 and 318 million in 2013.

Back to ANZ on the seaborne supply, particularly now that Gina Rineharts Roy Hill project is underway:

ANZ analysts Hynes and Soin said the fundamentals in the global iron ore market will “remain poor in 2016” as the huge supply response triggered from extraordinary price levels in 2010-11 will still be in process, although past the biggest gains made in 2013-14. In saying that, the commencement of shipments from the Roy Hill iron ore project saw exports at Port Hedland rise in December, increasing inventories at Chinese ports.

This all feeds into reducing steel demand this year with the China Iron and Steel Association (CISA) explaining to all and sundry – except the folks at Rio and BHP – that it will fall for years to come as excess domestic capacity chokes the sector.

From SCMP:

Zhang Guangning, chairman of China Iron and Steel Association, presented a grim outlook for the world’s largest steel manufacturing industry at the industry body’s first executive committee meeting.

“As our nation’s economy enters a ‘new normal,’ the steel-intensity of our economic output will continue to fall,” the online edition of state-backed China Metallurgical News quoted him as saying. “In years to come, apparent consumption will see a slow reduction trend … resulting in severe imbalances among production capacity, output and consumption.”

Crude steel apparent consumption – defined as the sum of production, net import and net decline in inventory – has fallen 5.5 per cent year on year to 645 million tonnes in last year’s first 11 months, after declining 3.3 per cent in 2014.

China Metallurgical Industry Planning and Research Institute last month forecast China’s steel output to fall 3.1 per cent this year to 781 million tonnes, after a 2.1 per cent decline last year.

Prepare for more pain, more mine closures and lower export revenue.