Right on cue, Domainfax’s spruiker-in-chief, Doc Andrew Wilson, has come out in defence of Sydney’s housing affordability, which the latest Demographia Housing Affordability Survey claimed costs on average 12.2 times median household incomes:

[Wilson] said the modelling was “misleading” because income was only important when considering the cost of repayments, which are at manageable levels due to low interest rates.

“Home ownership levels are largely stable across Melbourne and Sydney, while mortgage defaults are among the lowest on record,” he said…

The nature of housing market dynamics is idiosyncratic to parts and sub-sectors of capital cities, let alone countries,” Dr Wilson said.

Rather than bother responding to Doc Wilson’s comments directly, I’ll instead leave it to Residex’s (On-The-House’s) market analyst, Eliza Owen, who noted the following in October 2015:

Advertisement

Australian’s have high levels of private debt, with housing debt sitting at approximately $1.5 trillion dollars[1]. Australia’s GDP is only $1.453 trillion, meanings housing debt currently represents approximately 103% of GDP.

Given Australia has a low cash rate, it is relatively easy to service large amounts of debt. Furthermore, interest rates are likely to stay low for a long time, as other countries have set precedent (the US official cash rate has remained unchanged from 0.25% since 2008). However, interest rates will not stay low forever.

APRA has recommended the use of stress testing home loan rates of up to 7%. It is important to consider whether, especially for owner occupiers who do not receive rental income, dwellings are truly affordable.

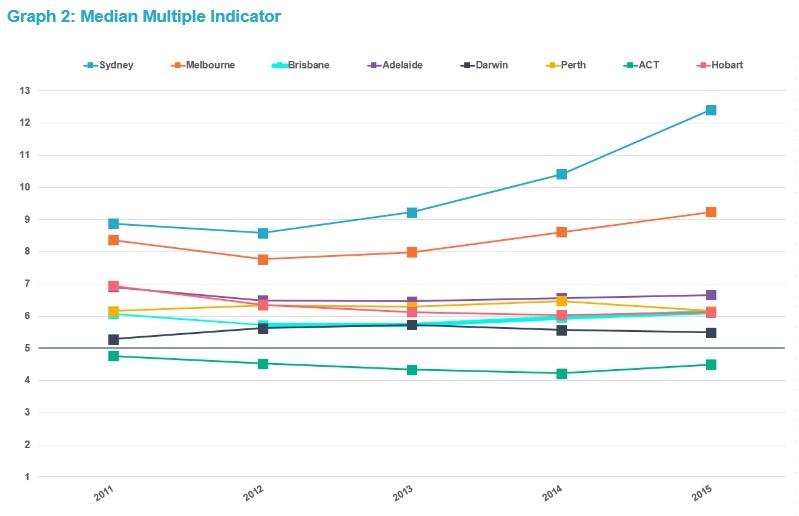

The international standard of affordability is a measure called the ‘Median Multiple’, designed by the World Bank. It is found by dividing median dwelling prices by gross, annual median household income. An indicator of 5 or more is considered to be highly unaffordable.

Graph 2 shows the Median Multiple Indicator for each capital city market for houses. To create our own version of this measure, I have used median house values from Residex, divided by median household incomes for each capital city[2].

For each region, with the exception of the ACT[3], houses in capital city markets are highly unaffordable relative to incomes. If wage growth continues to fall and interest rates rise in the long term, it will be harder for households to repay large amounts of debt. Further exacerbating the situation are subdued commodity prices, which the International Monetary Fund expect to hover around the current low prices for the next 5 years…

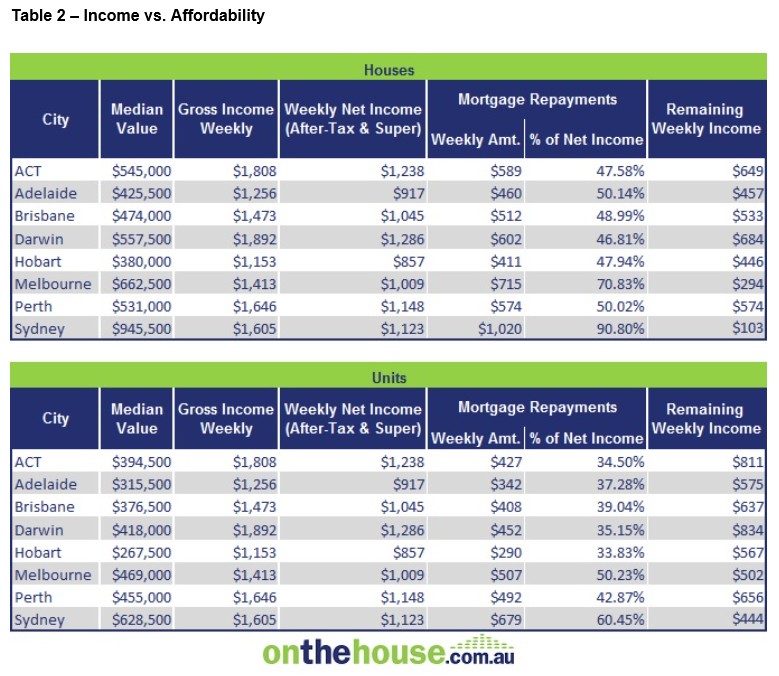

Ms Owen also described Sydney housing affordability as “a tad ridiculous” back in May 2015, in that “if the median household in Sydney were to purchase the median value house, they would be spending over 90% of their net income”, whereas a typical Melbourne household would spend a whopping 71% on a median value house (see below table).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.