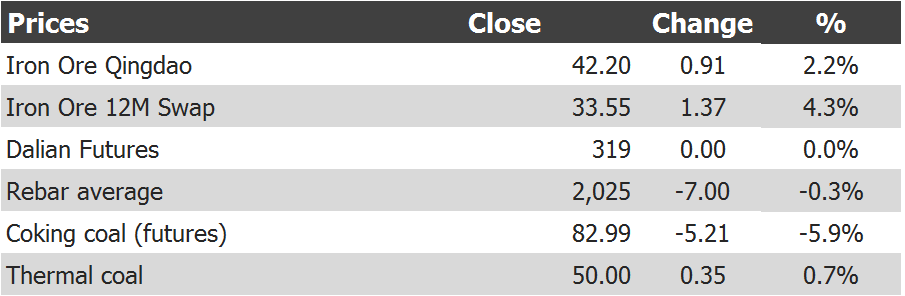

Here are the iron ore price charts for January 22, 2016:

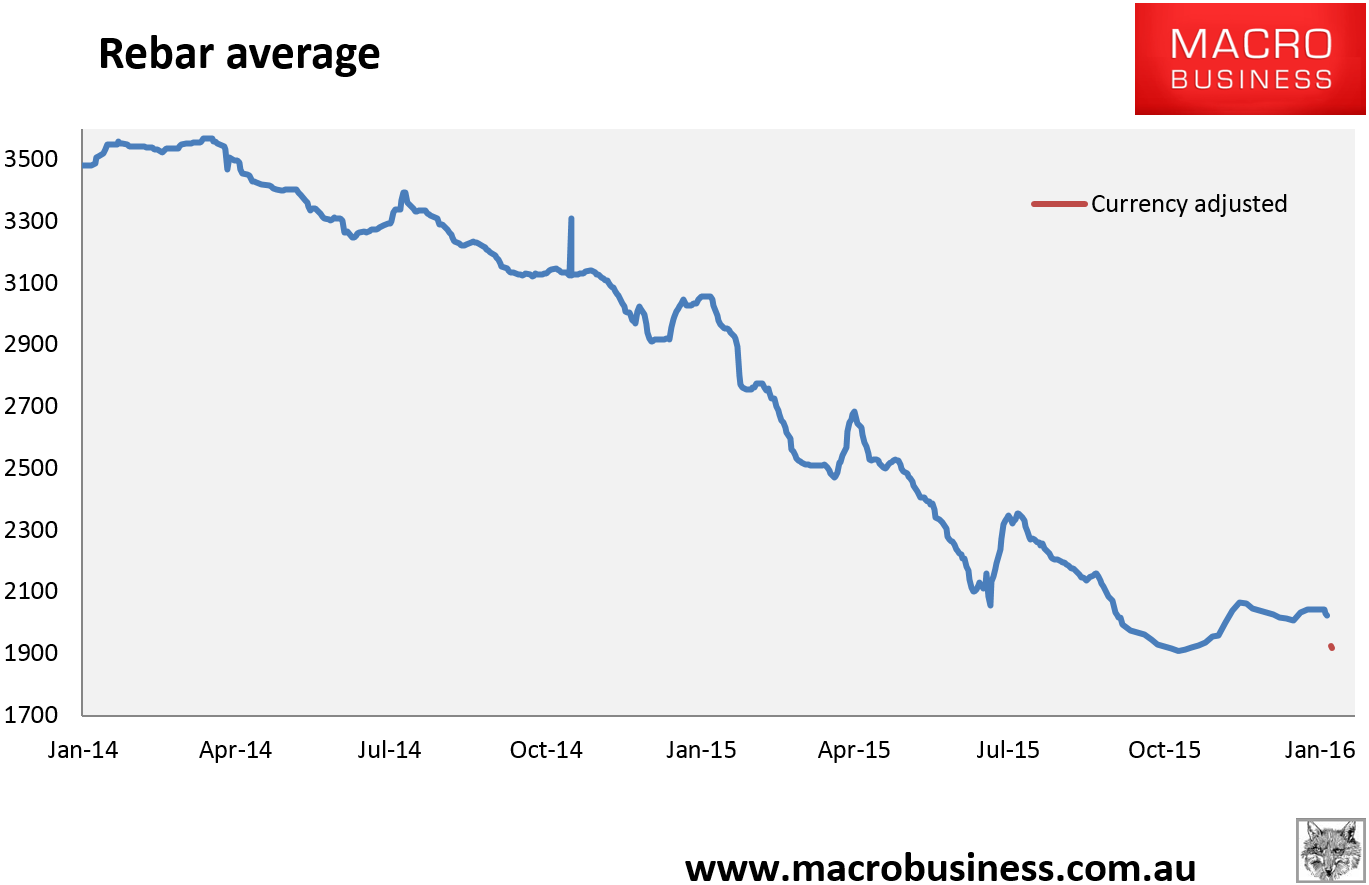

Welcome back and thanks to Chris for holding the fort. Where are we? Alas, nowhere good. Tianjin spot rose 1.9% to $41.30, paper is bouncing around without much purpose, rebar is rolling and in currency adjusted terms remains very weak.

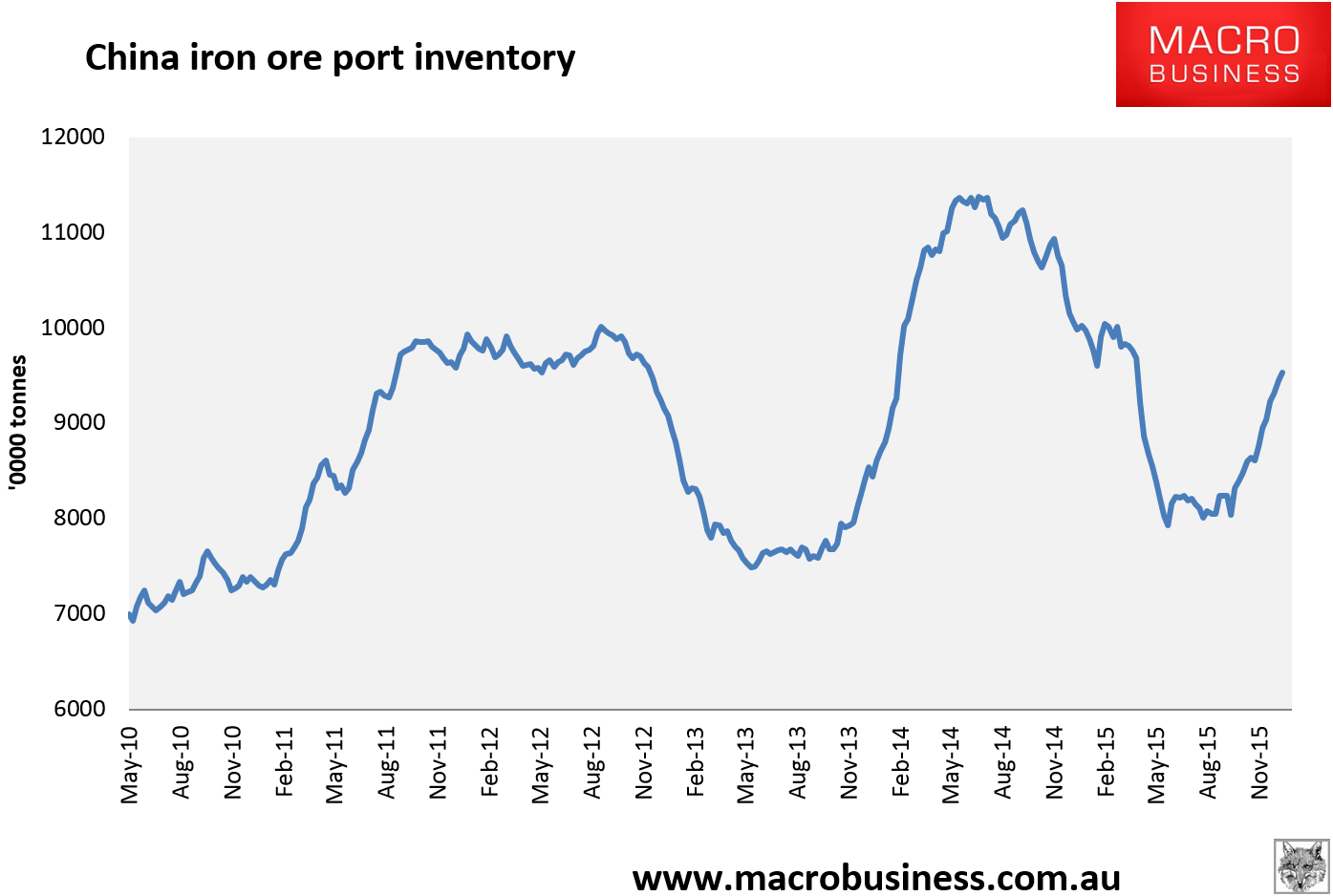

Prices have been firmer in my absence for one simple reason: restocking. There is no fundamental change in China, no evidence of a turn in demand, no sudden rationalisation of supply. The current demand impulse is that of rising inventories at Chinese steel mills and ports and when it has run its course, relatively shortly in my estimation, we will resume the price crash. The restock at Chinese ports (up another 800k tonnes last week to 95.35 million tonnes (mt)) is especially looming as a formidable risk for much lower prices before mid-year given that that stockpile acts as strategic reserve enabling mills to stare down miners: