From fastFT, with news just in that BHP Billiton is making a $7.2billion writedown on its US shale assets:

An impairment charge by the Anglo-Australian miner, a big player in US onshore oil and gas, had been expected but the amount makes it the largest announced by BHP during the mining downturn. The writedown equates to $4.9bn after tax, writes James Wilson in London.

In a statement Andrew Mackenzie, chief executive, said oil and gas markets had been significantly weaker than the industry expected.

“We responded quickly by dramatically cutting our operating and capital costs, and reducing the number of operated rigs in the Onshore US business from 26 a year ago to five by the end of the current quarter.

While we have made significant progress, the dramatic fall in prices has led to the disappointing write down announced today. However, we remain confident in the long-term outlook and the quality of our acreage. We are well positioned to respond to a recovery.”

Saudis finally get a small taste of blood in their losing war with the US shale oil operators. The writedown pales into insignificance how much the barbaric Kingdom has lost in oil revenue – and foreign exchange reserves, not to mention their bloated welfare budget – by maintaining production levels.

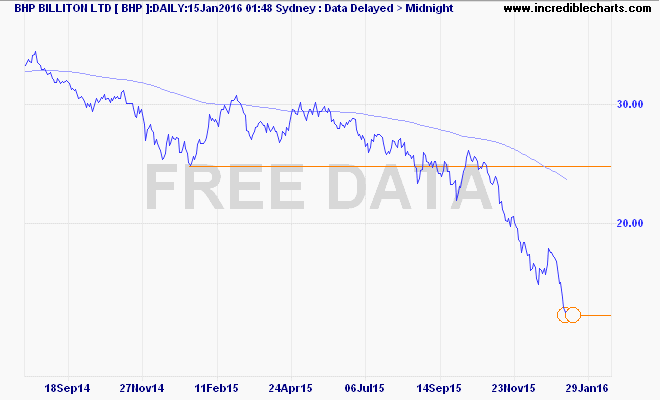

As for the share price, the news is probably already baked in:

Last night it lifted 6% on the London markets, BHP has lifted over 4% on the open today – but is this the bottom? Writedowns will have to be made elsewhere as the once nicely diversified company has been up-risked unnecessarily into focusing on four pillars that look shakier than a politicians promise.