Alas for Glenn Stevens his time has come. He should neither be reappointed nor allowed to drift heroically into retirement.

The Governor of the Reserve Bank is currently embarked on a national lap of honour claiming victory over the mining boom and bust. If he paused for moment in this plumping of his legacy narrative he would notice that the bust is only half over and that the job of the RBA and broader policy-makers is about to turn a lot harder not easier.

I have been great fan of Glenn Stevens over time. His first term as Governor was excellent. But his second term has been a disaster and in public policy one should only be as good as one’s last game. Not least because if you’re going to take the salary of a private sector CEO then a little shareholder accountability comes with it.

Let’s examine the ledger.

When Stevens inherited the RBA’s top job in 2006, 10 years of firm inflation was baked into consumer expectations. As the mining boom took off, so did the economic party. Stevens showed a determined, some might say old-fashioned, drive to take away the punch bowl. The bank started behind the curve but hiked hard into 2007.

It rightly ignored criticism from all quarters in doing so, hiked during an election campaign, and was winning the battle before the GFC struck in late 2008.

In the post-GFC environment, Stevens continued his hawkishness. As Australia’s terms of trade rebounded in 2009 and the mining boom resumed, the Stevens RBA was quick to begin normalising interest rates. It also choked off a second coming of Australia’s irrepressible housing bubble that had been fired up by fabulously generous fiscal policies.

Another of Stevens’ strengths was evident at this point. As the Labor government flailed about with the politics of recovery, eventually blowing itself up in the RSPT debacle, the RBA chief led the nation’s understanding of its new normal. He kept a cool head and offered a strong and understandable narrative for the nation about the need to prevent further debt accumulation in households, the need to reform the financial sector, the need to prevent further accumulation of offshore debt and the need to free up resources for the mining boom in what became known as the “structural adjustment”.

From the perspective of its mandate to modulate inflation, Stevens’ RBA has absorbed a global financial crisis and 150 year mining boom. No small achievement.

However, as is often the case in the human condition, great strength cab be paired with its opposite vulnerability. This is where we come to the question over Stevens’ second tenure at the Bank. Under Stevens, the central bank has produced the most singularly bullish forecasts for Chinese growth and its impact on commodity prices of any institution in the world (with perhaps the exception of the Australian Treasury and the Bureau of Resources and Energy Economics).

This assumption led the monetary strategy of “structural adjustment”, using high interest rates and a consequent high dollar to crush non-mining tradeable sectors so mining could grow at super-fast rates without causing inflation. But it had a big downside. It “hollowed out” other tradeable sectors — manufacturing, tourism, education and rural goods — and now that the commodities boom is going bust thirty years earlier than the RBA planned, we find ourselves with some very overpriced and underperforming holes in the ground and not much else.

In short, the RBA sought to turn Dutch Disease into a virtue and has been proven to be wrong to have done so. Stevens could rightly argue monetary policy could have done little to combat Dutch Disease. Most remedies are fiscal. But the ongoing currency war has opened up a conservative space — supported by the International Monetary Fund, Ben Bernanke and others — where measures to address the capital flows that cause overvalued currency can be addressed. Tobin taxes are now acceptable as are macroprudential tools or even printing money for foreign central banks.

The Stevens RBA refused to publicly countenance any of these. Indeed it openly stood in the way of all of them. Instead, as it became apparent that the mining boom was not going to last forever as it had expected, it slashed interest rates and egged on a housing price boom to fill the growth gap.

And here’s the kicker. By doing so, Stevens quietly back-flipped on every lesson in economic sense he’d just taught the nation post-GFC.

Let’s recall what he told Parliament in 2010:

We have looked at households in other countries getting into serious trouble. I think we have all thought, ‘We ought to be a bit careful about rate of borrowing and maybe we should be saving more of our current income as opposed to allowing an assumed rise in asset values to, in effect, do our saving for us.’ I think that is a tendency that was there a few years back in many countries. My guess is that there has been akind of sea change in people’s attitudes that we would expect to persist for a while.

Pretty much every supervisor in the world is telling their banks to rely less on wholesale funding because it is risky. The rating agencies say it. My suspicion would be that, if the financial institutions could have got away with continuing the old pattern, they would have because they found it attractive and profitable, but they did not have that choice. They certainly took decisions to try to raise more deposit funding but it was a decision on which I am not sure they had a great deal of choice in taking.

In many areas it is probably the case that more competition is always better for consumers, but in banking more competition is good to a point but beyond a point more competition is not good, because the bankers can be led to do things that ultimately cause a lot of subsequent damage. I think we have to understand that. That is not to say that the current amount of competition we see in any particular market is necessarily enough, but there is a point beyond which extreme competition in lending money leads to problems.

They [the banks] have sought to do that to increase the share of their book funded from domestic deposits and to lessen the share funded through wholesale sources. It is pretty obvious why that happens and I think it is prudent of them to do it. What we have seen in the past several years is that those wholesale funding sources, which for some years up to the middle of 2007 were very available, very inexpensive and, apparently, quite reliable and quite stable, changed dramatically after the problems began in 2007 and especially after the Lehman failure in September 2008.

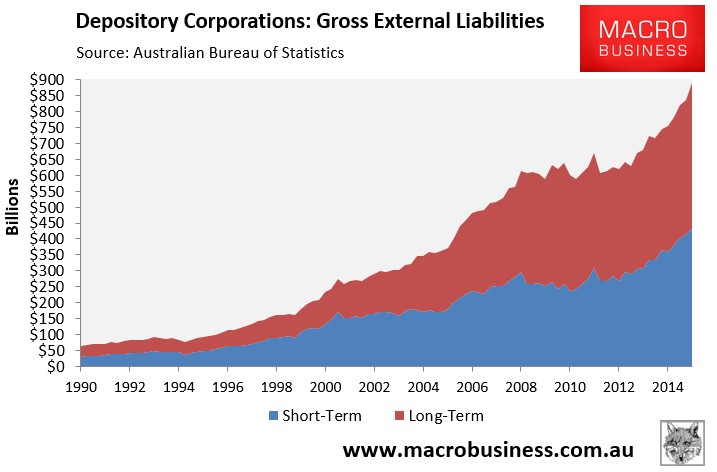

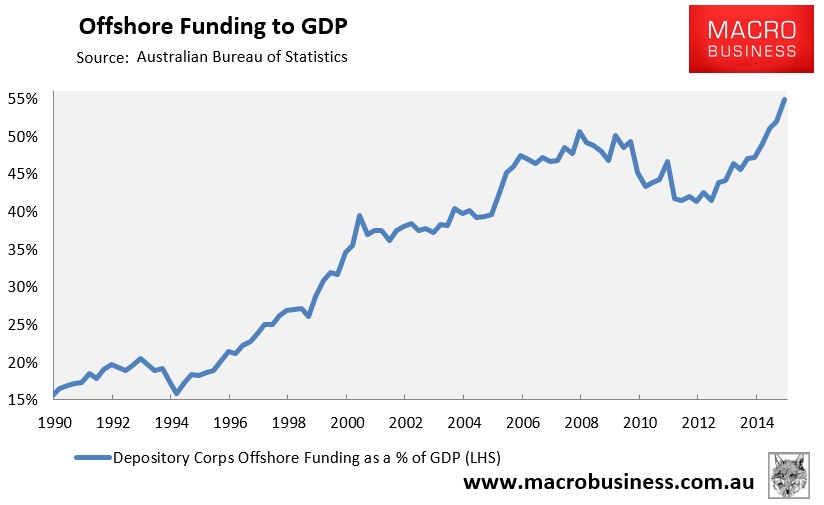

Yet, as the Stevens RBA scrambled to cover its mining boom blunder after 2011 with its crazy hosing bubble, this is what it has done to the “risky” wholesale debt to which it was averse previously:

Yes, the proportion of bank deposit funding is still higher than it was before the GFC but the above is a clear and present danger to the nation if and when another external funding freeze transpires.

It was not the only path the Stevens RBA could have taken. Had Stevens supported monetary and prudential policy innovation earlier, Australia would have had a lower dollar years earlier and would now be enjoying a tradables boom and solid housing recovery without this extreme rolling of the dice.

For his part, Glenn Stevens gambled the Australian economy on China and lost. Having done so he made an inconceivably reckless bet on house prices in the post-GFC context and is in the process of losing.

That is why Glenn Stevens should be sacked.