It is one of the great mysteries of our time. How can Australia, the world’s largest iron exporter by far, not understand how the market and business works? We’ve see the RBA and Treasury stake our entire futures on ludicrous notions of permanent high plateaus for prices. We’ve seen our equity markets and sell side research consistently mis-price miners for recoveries. We’ve seen the miners themselves massively mal-invest on the preposterous notion that iron ore had an astounding $120 price floor when the historical average price is $60 with much of the time spent at half of that and below. We’ve see our media cheer lead punter’s money investment into all of it as it just keeps on falling.

The latest mis-uderstanding comes from Stephen Cauchi, who appears to be on mission to mis-inform about iron ore, and Adam Boynton of Deutsche, who has recently appointed himself iron ore soother-in-chief to the nation:

At $US36, “that’s the point where if you were sustained under there for a while you’d start to lose the first chunk of Australian production”. At $US26, “most Australian production is uneconomic”.

“Australia is ‘the’ low cost iron ore producer, so if we’re uneconomic at those levels, why is anyone else producing?”

To sustain those levels would be “highly surprising”, said Mr Boyton, as it would require non-traditional uneconomic producers of iron ore to be still producing at significant volume.

“The prospect that that’s where you end up, and it’s ultimately Australian production that comes out of the market, is very small.”

“The biggest impact on an iron ore price in the high $US30s remains the implications for federal government finances,” Mr Boyton said.

“Much of the impact of lower commodity prices has been absorbed by the federal government via larger deficits and a higher level of net debt.”

“The hit to the real economy from lower commodity prices will come if the federal government decides it can no longer … continue to absorb this balance sheet pressure.”

However, “we don’t expect to be at that point for a few years yet”.

“We also wouldn’t expect the Australian dollar to ‘automatically’ fall in response to lower iron ore prices unless the market prices a greater risk of rate cuts from the RBA.”

Come now, Mr Boynton. You are using all-in break evens here not cash costs. And it is the latter that will determine when mines close. At $36, FMG may be losing money in an accounting sense but unless it is forced to cut production by its creditors, it won’t. It will assume that the price is going to rebound and keep pumping, for years. Shutting a mine is quite expensive so there’s no hurry to do it. And when you have a highly leveraged balance sheet, lower revenue and equity is the last thing you need. FMG’s cash cost is, in fact, $16-20. And that’s where the price will need to approach for it to unilaterally shut-in mines.

We can extend the same logic to the majors. They aren’t going to shut-in production until their cash costs are hit at an even lower price.

There really is no absolute low for iron ore. It just keeps falling until enough production is cut at cash costs.

One possible scenario for a higher price floor is that the majors decide to cut production ahead of junior bankruptcies to establish a price that that leaves them profitable but is low enough for long enough to make FMG’s creditors pull the plug. That price could be in the low $30s.

But even that is a very troubled idea. There is still so much new production coming from Roy Hill, Sino, Vale and India that their production cuts would have to continue and the market share losses would be big unless they could all collude on it, which is both illegal and seems pretty unmanageable to me. As well, even if creditors take control of the mines, they might decide to keep cutting costs and pumping!

It’s time to stop thinking about the iron decline as a rational cost curve shakeout that’s burying higher cost miners one by one. We appear to be on the verge instead of an outright crash in the iron ore market that will force a singular collapse in supply as the entire cost curve falls into the red. Right now the dynamics of the iron market actually make it more likely than not. How could this happen?

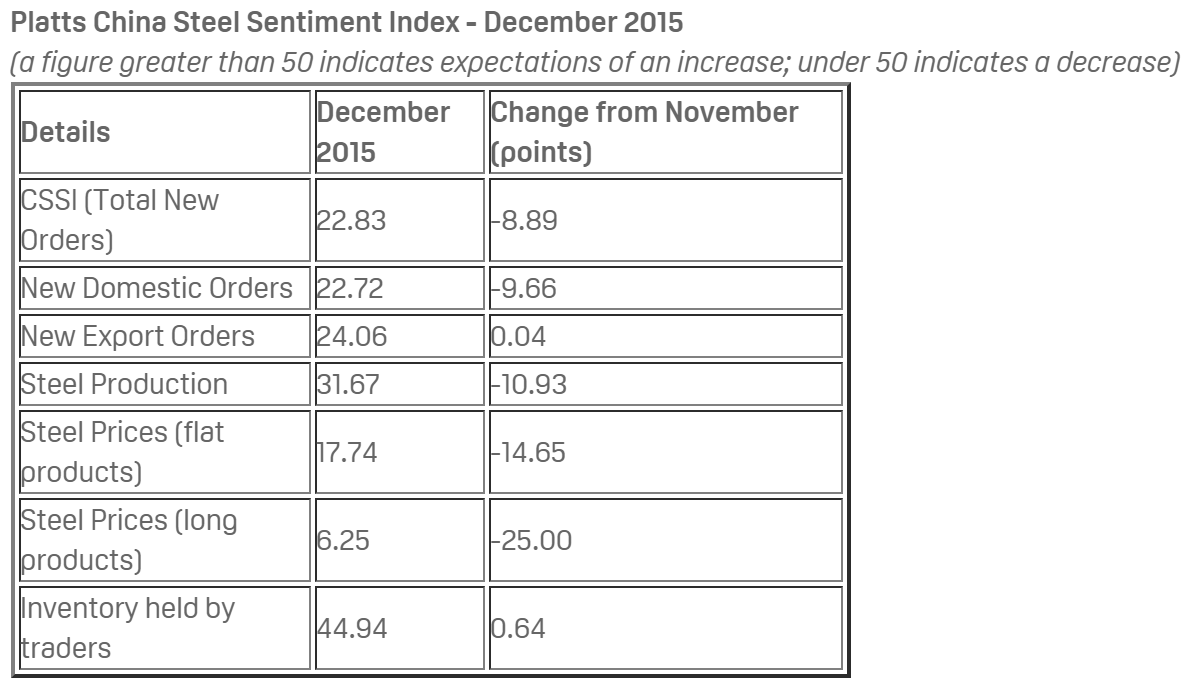

First let’s assess steel. Steel mills are massively over-producing and crashing steel prices. They can’t stop lest they never restart because cash flow is now so constrained that loss-making liquidity is better than bankruptcy. Yet, steel output is still slowly falling, just not fast enough to keep pace with plummeting demand. We know demand is terrible from the Platts survey:

Both internal and external demand is shocking. Domestically, some of this is seasonal as the northern winter shuts in construction but a lot of it is also this:

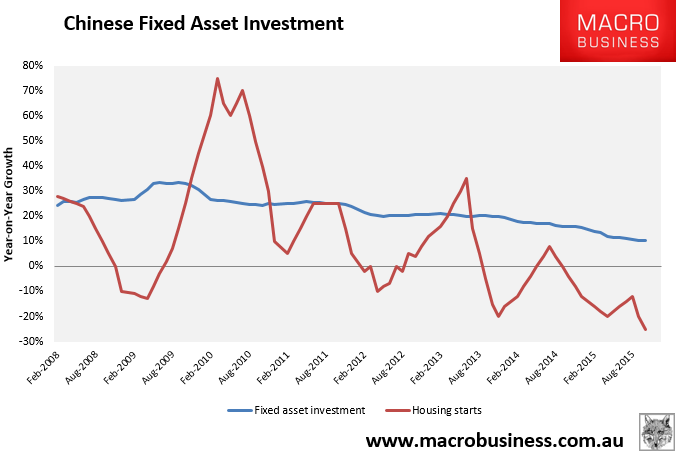

Chinese housing starts are down 15.2% on a rolling annual basis and if they constitute 40% of consumption (some say higher, some lower) then demand is off 6.1% over the year. This is more than the 2-4% apparent in steel production figures with the difference until now made up by exports. But with the export growth outlet stalling, the full domestic falls are coming through now and that equates to an impressive 50 million tonnes (mt) less steel consumption at an annualised rate than in 2014. Some of this will be seasonal weakness for Chinese steel but that return seems likely offset by further shut downs in production anyway. Manufacturing (which makes up 30% of consumption is also shrinking but infrastructure (another 30%) is growing so let’s cancel those two out.

As such mills can also destock raw material inventories and resell ‘take or pay’ contract cargoes that they don’t need at ports. These volumes are accumulating fast in China as a kind of strategic reserve that protects mills from any sudden shortages brought on by miners or anything else. Thus they can keep this pattern of trading up indefinitely or at least until enough of them go bankrupt that it stabilises steel prices, but that is very far away.

Now to iron ore. Through the middle of this year it was widely thought that surplus capacity was around 70mt. Since then both RIO and BHP have hit the accelerator. In the September quarter RIO sold 73mt of ore. But to make its volume targets it has to sell at 90mt for each of the next three quarters. Thus, since October it has added nearly 70mt of annualised capacity to the market.

BHP has also been growing fast but not since the September quarter and Samarco has been taken out removing 40mt from the global markets.

There have other smaller departures and arrivals but those are the big ones so where does that leave the market balance?

- mid-year surplus 70mt

- China demand fall 81mt (50mt steel / .62 iron ore)

- RIO 68mt

- Samarco -40mt

That adds up to annualised seaborne surplus capacity of a staggering 179mt or 15mt per month.

So, if we add the tactical set up of the market to this structural oversupply, we get a situation in which only the closure of a lot of iron ore supply is going to stabilise prices. Where will that come from?

Some will be Chinese. Let’s say another 13% this year or 30mt. With the yuan now officially devaluing there’ll be no more than that. Some of it will be the Australian junior sector or 40mt. But that still leaves us with 109mt that needs to be rationalised and once the juniors are gone we are left with Kumba (50mt) and Fortescue (165mt) both with all-in breakevens around $4o per tonne. As said, cash costs are much lower and that’s where the price will need to go to get them to even consider shutting production. Sure they have troubled balance sheets but it seems unlikely to trigger loan covenants at this point. If iron ore fell to $20, for instance, FMG could still survive for a year as it chewed through its $2 billion in cash.

You will notice that I have not included the 15mt that arrives from the Roy Hill “whale” next year, nor roughly the same from Vale’s 90mt S11D monster, nor a resumption of Indian production, nor the return of Samarco ore. I’m only discussing what needs to come out of the market right now.

The entire iron ore cost curve is on the verge of total submersion in a sea of red ink and it may not come up for years. It is entirely possible, indeed likely, that we will not see the bottom until we are in the low teens.

As for the impact on Australia, Boyton is also wrong. There are three large channels for falling iron ore to hit the economy not one.

First, you can’t remove the investment bust from the fallout. It is still changing and central to the economic outcome. The RBA currently reckons the bust is halfway through but with the iron ore in the $30s and $20s that means much more cost-out carnage across the sector ahead and deeper falls for investment than anyone is expecting. The difference between mining investment-to-GDP falling to 3% or 1% is enormous.

For instance, the entire junior sector is about to go under shedding roughly 5,000 direct jobs plus 3x mutlipliers. As well, major second tier miners will go bust in the $20s, doubling that fallout. Exploration, capex, opex and headcount will be shredded across the major miners as well. None of this is expected.

The second dimension missed by Deutsche is the stock market hit. All dividends will be gone, hitting income. And does Deutsche really think that BHP, RIO falling another 50% will have no impact on household confidence via both their super portfolios and just the sheer sticker shock of it?

The third impact is right in various budgets but is again under-played. Wrecked Budget outlooks have contributed directly to the ruin of two consecutive Federal governments. Turnbull is about to lose his sheen as first his MYEFO then his first Budget shocks the nation anew. Australians know that the Budget in some way supports their income and debt servicing capacity so even if the Government absorbs much of the blow initially they also know that it won’t last and that will contribute to a stronger deleveraging pulse. I’m not usually a fan of Ricardian equivalence but in Australia’s contemporary economy the linkages are so clear that it holds some water.

As for when the Government will be forced to stop running bigger deficits, it may or may not be a few years yet, depending upon how swiftly the mining GFC progresses into sovereign spreads. The credit rating agencies still have stupid iron ore price assumptions and when they’re cut the question must be asked about the AAA rating.

When you throw in the basic structure of the Australian economy – that we earn income via dirt and leverage that up for house prices to juice services spending – the loss of the largest and by far the most profitable sources of the underpinning income is fatal to the structure.

Australia is iron ore and as the income plunges towards zero so will Australia’s economy.