Australia continues its economic muddle-through. There remain good reasons to expect a recession in 2016, but investors shouldn’t make that their base case until the labour market starts to crack – and it hasn’t yet. Australian equities will likely continue to under-perform even in the muddle-through scenario. The problem is the ASX200 is overweight the past: it is dominated by mining and banking, sectors that have a great future behind them.

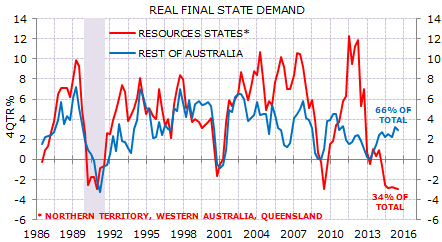

Australia continues to struggle with the end of the mining super-cycle. In three years spending in mining-dominated states has gone from faster-than-China growth rates to now slower-than-Japan. There has been a rebalance of sorts with some slack picked up elsewhere (Exhibit 1).

But that rebalance faces challenges next year: mining capex will continue to fall; the domestic car producers will wind down; residential investment is unlikely to contribute as much to growth next year as this year; and there’s a serious risk of drought.

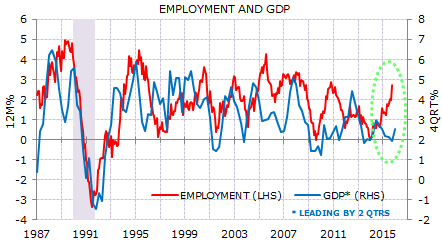

However, I won’t make recession the investment base-case until there are warning signs on employment. Now, remarkably, employment growth has accelerated even as GDP growth has slowed (Exhibit 2).

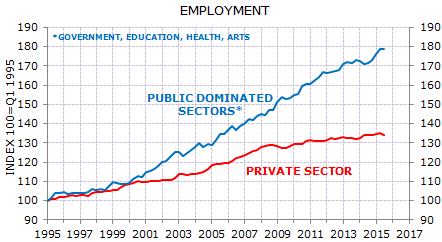

Industry-level jobs data, available to August, show that much of the employment growth has been in public-dominated sectors (Exhibit 3).

This undoubtedly has a structural component, but growth has been particularly strong over the past two years.

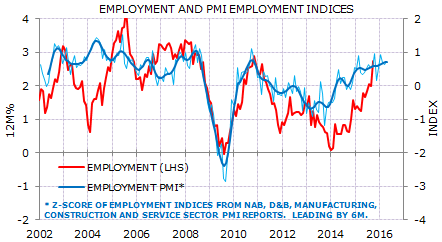

It remains a moot point whether that employment strength can be sustained. However, for now the broad range of labour indicators remain reasonable, even if there are issues with the Bureau of Statistics’ monthly job numbers. I am watching corporate hiring intentions. They remain solid, so recession, on a 6 month view, seems unlikely (Exhibit 4).

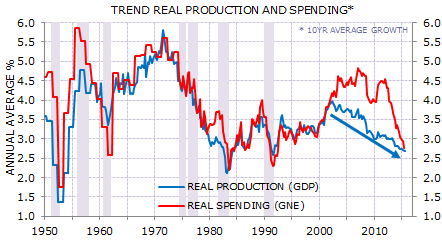

Recession or not Australia continues to face a long period of structural adjustment. First, trend GDP is falling. In fact, trend GDP growth has been falling for a decade. The bigger issue for business is that an even larger adjustment is likely for domestic spending, and that spending drives revenue growth. The commodity boom allowed Australia to enjoy an unprecedented period where trend growth in spending (gross national expenditure) exceeded trend growth in production (GDP). Rising export prices meant that a given volume of production could fund a higher volume of consumption. With the terms of trade falling, this income effect swings into reverse. After a decade where the trend growth in spending was above the trend growth in GDP, Australia will likely face a decade where spending has to rise less than GDP – and that GDP growth rate is itself falling (Exhibit 5).

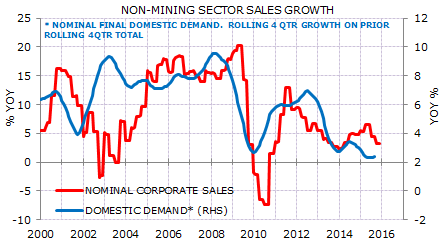

This is a big deal for domestic business. Excluding miners, the listed sector enjoyed 15%-plus annual sales growth last cycle; now nominal sales growth is less than one-third that pace (Exhibit 6).

This is the new normal for domestically-focused business.

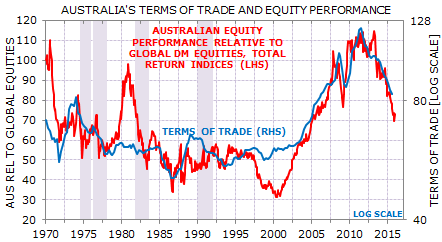

Structurally lower domestic sales, combined with the stress in the resource sector – which, in my view, is not at its lows – points to further under-performance of Australia equities versus other developed markets. This will maintain the historical correlation between Australia’s terms of trade and the relative performance of Australian equities (Exhibit 7).

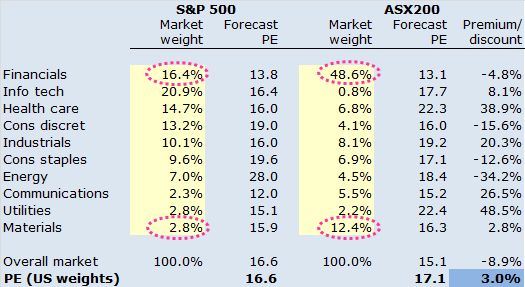

There are reasons to be positive about the medium term outlook for Australia. But the problem for investors is that increasingly the equity market does not reflect the economy. Australia’s listed market has a much larger exposure to financials and materials (which includes miners) than other markets – and these sectors’ share of market capitalisation are much larger than their share of the domestic economy (Exhibit 8). Put simply, Australia’s equity market is overweight two sectors at the end of their super-cycles; it is overweight the past and underweight the future.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.