The International Energy Agency (IEA), often referred to by coal producers due to its bullish outlook, today released their Medium-Term Coal Market Report to 2020. They have cut their total global 2020 demand for coal by 500Mtce to 5.8bn Mtce and slashed their 5 year growth in Chinese coal demand from 2.6%pa to 0.8%pa.

Global demand outlook cut: This release marks a major pull-back from the IEA’s prior numbers, and supports our general outlook that demand for thermal coal is in structural decline. Despite this, the IEA are still forecasting seaborne trade of thermal coal of 1.06bn Mt in 2020, 275Mt above our own estimates for 2020!

Chinese growth target slashed: From their 2.6%pa 5 year growth target, the IEA have now pulled back to 0.8%pa with a 2020 total thermal coal Chinese demand target of 3.5bn tonnes for 2020. For thermal coal imports in 2020 they are forecasting 128Mt, almost triple our own estimates of 46Mt mentioned in our recent forecast.

Coal outlook likely to continue to deteriorate: On top of their already weakened outlook, the IEA stated “the golden age of coal in China seems to be over.” For the first time they have included a peak China coal scenario in their forecast in which coal demand in China would only reach 2.15bn tonnes by 2020 with 36Mt of imports, a figure much more closely aligned with our own.

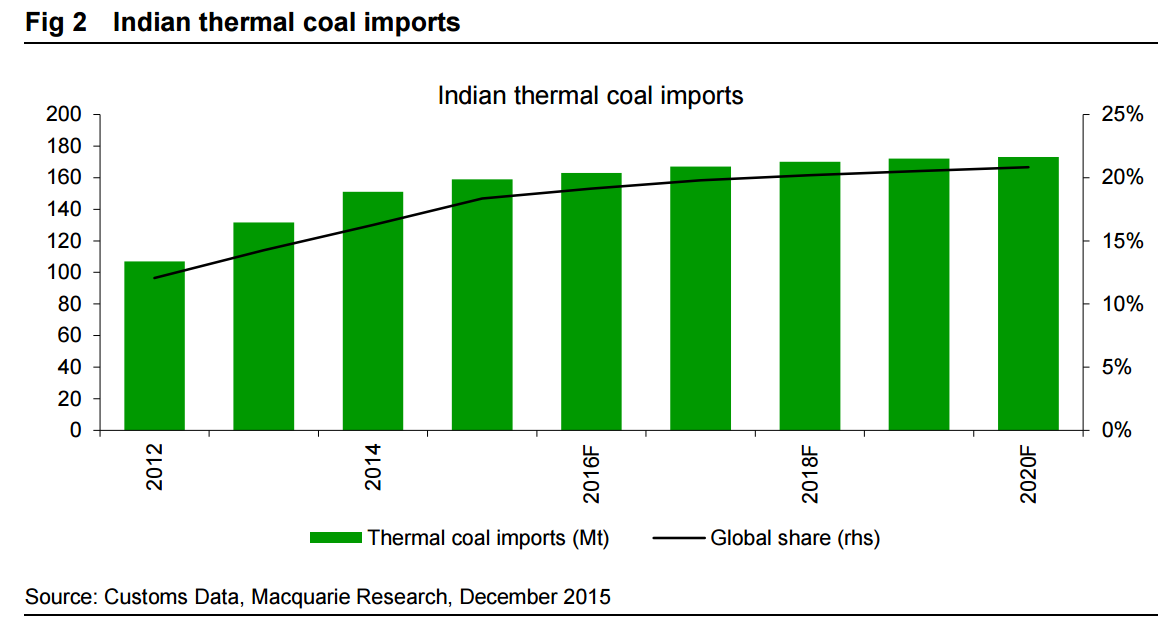

India can’t save producers either: The IEA is forecasting that India will increase its thermal coal imports to 204Mt by 2020, a staggering 73Mt increase over their estimate of imports for 2014. Though we certainly think India will increase production, it will come primarily from domestic sources as Coal India looks to increase production. More importantly, we expect that seaborne demand in 2020 will only grow by 14Mt from 2015 to 173Mt. This means there is limited upside for Australian producers already on the cusp of sustained low prices and project developers looking to build new thermal coal projects reliant on export prices.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.