I’ve noted recently the number of upgrades raining upon Fortescue and another one arrives today from Deutsche, though this time it is only from “sell” to “hold”:

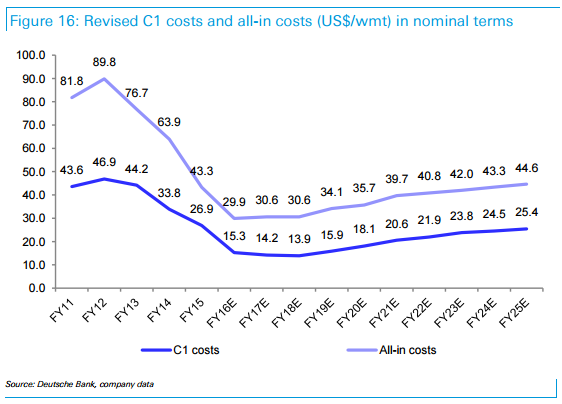

Costs are sustainable over the medium term. Upgrade to HOLD A recent visit to FMG’s operations highlighted the plant (OPF) upgrades that have allowed a big drop in strip ratios at the Chichester Hub. These upgrades have not only offset a fall in head grade but have lifted recoveries. Combined with the continued automation of the Kings mining fleet and now the OPFs, we think C1 costs can fall below US$15/wmt in FY17 and sustaining capex can remain at $2-3/wmt for some time. However the visit also confirmed our prior views that group strip ratios, costs and capex will climb over the long run and product grades will decline. We have increased our earnings estimates significantly and have upgraded our NPV to A$2.77/sh and rating to HOLD.

Strip ratios still climbing, but off a lower base FMG’s group strip ratio will average just 1.3:1 in FY16, down from 1.9:1 in FY15. Most of this drop is associated with moving the pit high walls up-dip, mining along strike, and mining lower grade inferred resources at the Chichesters. The change in mining strategy at the Chichesters has been made possible with upgrades to the OPF classification circuits (in particular the screens and cyclones). These upgrades have not only offset a 0.5-1% drop in head grade at Christmas Creek but have actually lifted yields by over 5%. We think yields can increase further when all the OPF upgrades and also automation is completed. From FY17-FY20 though, strip ratios at Kings are set to double, lifting group strip ratios to above 2:1. However due to the OPF upgrades, group strip ratios will now climb off a lower base.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.