Yesterday I had a go at Trevor Sykes and his “back in my day banks only went up” analysis of banks. Happily today I can offer a few more charts on why this view is so very deeply troubled. Morgan Stanley is onto it:

Banks continue to under perform : Our chart of the week shows that the under performance of the Australian Banks sector has continued since the breakout in April this year – down 11% relative. Our chart also compares this period of under performance to other periods of sustained weakness in the last 15 years. There were three such occasions: (1) June 2003 to Dec 2004 – the last time markets feared an organically grown recession; (2) Nov 2006 to June 2008 – Resource boom ending in GFC;and (3) July 2010 – Jan 2011 – GFC Redux/Reflux anxiety. On all occasions the period of under performance vs. the ASX 200 lasted more than 18 months. The 2015 version has run eight months.

Banks’ defensive traits challenged: We are often asked why would we not be attracted to the defensive yield characteristics of the banks now that forward P/Es are 11.8x and net yields are 6%+.This would be pertinent were banks displaying a utility-like investment case.The issue from a portfolio standpoint is that the risks to those defensive pillars are building. Forecast EPS is already flat for the sector and should DPS downside out size earnings declines, the pressure on stock ratings will be down, not up.

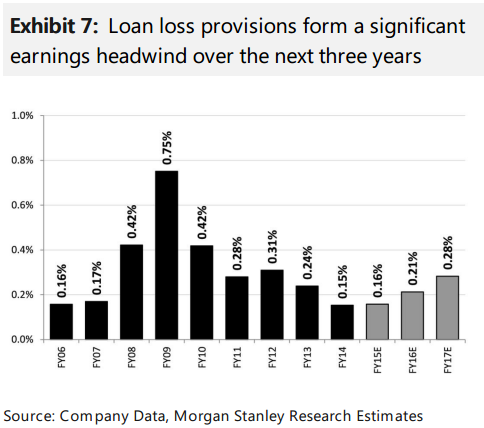

Risk of dividend cuts? Our banks team highlighted this week the risk to banks’ dividend payout ratios, with capital and macro headwinds creating a “grey” area for dividend cuts. They point out that payout ratios have increased since FY11, despite the lift in capital requirements and recent decline in ROE. As such, the probability of dividend cuts is rising. FY15 results suggest that ANZ and NAB have less margin for error than CBA and WBC. This, pressure on ROE from ongoing capital requirements, and the risks to EPS from a deteriorating loan loss cycle underpin our conviction in retaining an active UW position on the sector.

That is outstanding analysis, not something I get to say very often. The terrifying payout ratio is the smoking gun as even the slightest deterioration in economic circumstances will trigger dividend cuts as bad loans rise:

And EPS falls:

And remember that this analysis is conservative, not especially bearish. If you believe as I do that we’re headed into something more like a 1991 event then the above scenario is simply your short insurance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Banks continue to under perform : Our chart of the week shows that the under performance of the Australian Banks sector has continued since the breakout in April this year – down 11% relative. Our chart also compares this period of under performance to other periods of sustained weakness in the last 15 years. There were three such occasions: (1) June 2003 to Dec 2004 – the last time markets feared an organically grown recession; (2) Nov 2006 to June 2008 – Resource boom ending in GFC;and (3) July 2010 – Jan 2011 – GFC Redux/Reflux anxiety. On all occasions the period of under performance vs. the ASX 200 lasted more than 18 months. The 2015 version has run eight months.

standpoint is that the risks to those defensive pillars are building. Forecast EPS is already flat for the sector and should DPS downside out size earnings declines, the pressure on stock ratings will be down, not up.