I’m not sure what Trevor Sykes’ high reputation is based upon given recent poorly reasoned endorsements of Aussie banks, including another today from the AFR:

The gurus have been pointing out that the Australian economy is likely to slow, the housing boom is peaking, and the banks’ performances will be crimped because they’ve had to raise more capital to meet Basel III requirements for common equity Tier 1 (CET1) ratios, with possibly tougher Basel IV rules to be announced next year.

All true enough, but in practice what can a retail investor do?

…BHP, Rio, Woollies and Telstra would have been dangerous foxholes, and Wesfarmers has been jaggedly down. Outside them you’re getting into Australia’s second rank.

A cautious investor could have switched into bank deposits or cash management trusts where the (taxable) interest rate would be between 1 and 2 per cent.

And? The banks are either a good investment or they are not. Cash always generates less than equity so this is a nonsense argument, unless you don’t give a hoot about return of capital.

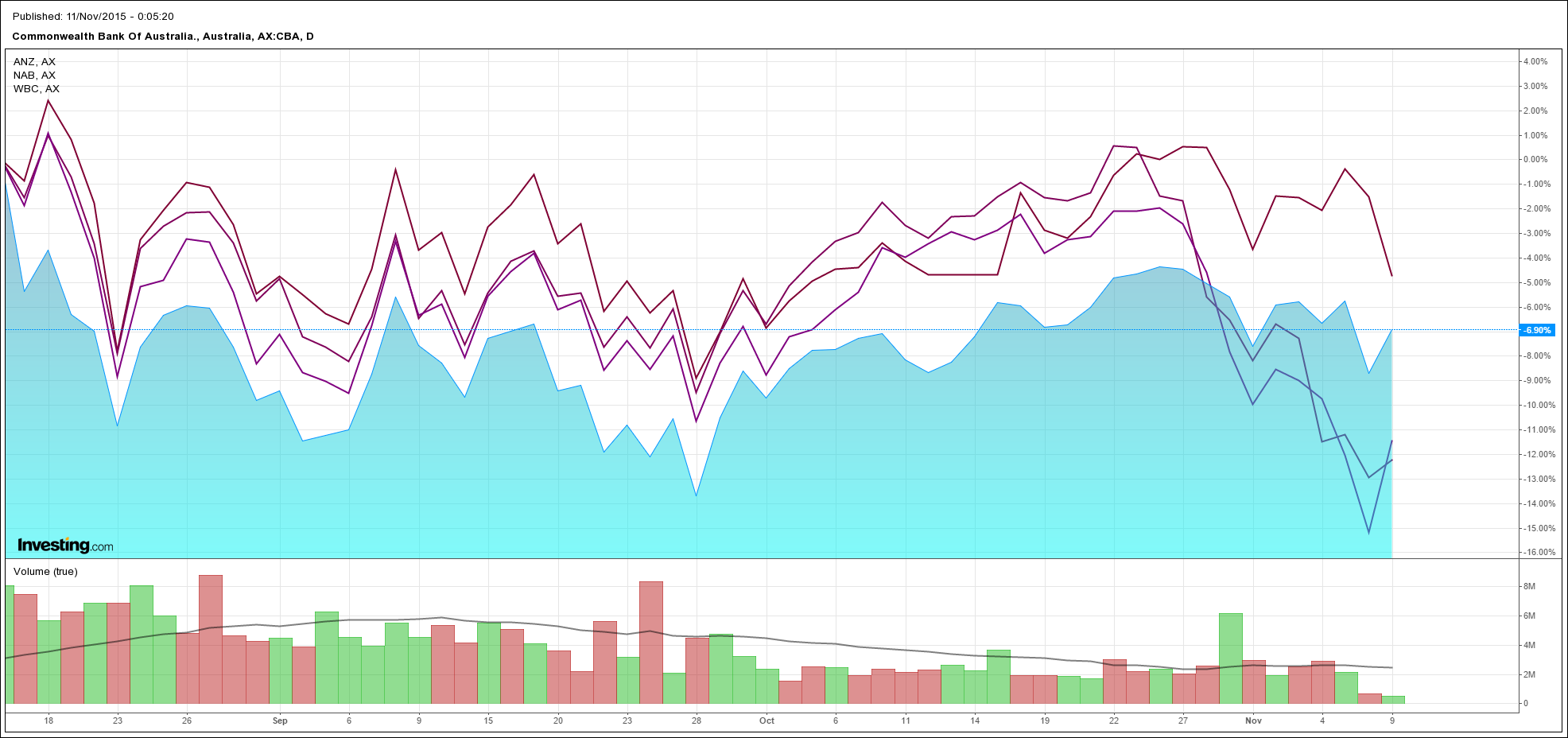

Sykes first put this rather thin analysis in early August and had you taken it you’d be down at a very good clip despite receiving half a dividend:

That’s not to illustrate the stupidity of Sykes, that would be obviously ludicrous over a couple of months, it’s to make the point that return of capital matters, to everyone other than Mr Sykes and The Pascometer anyway, and you may find somewhere down the track that you want to get your money out because returns no longer look so hot only to find you can’t without crystallising large losses.

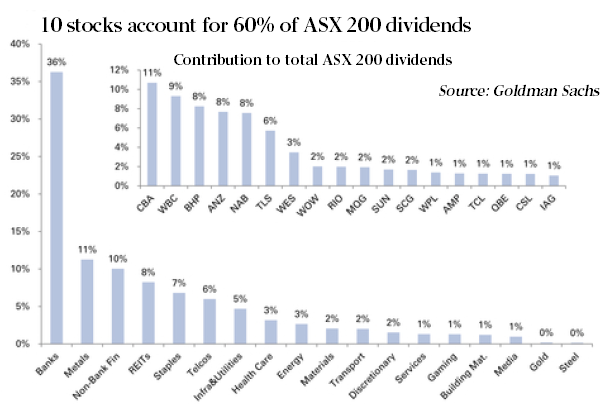

The Aussie banks are moving out of their dream run in a global low interest rate environment and into a much more challenging period of low growth, crimped margins and declining asset quality even as they’re running super lean on huge payout ratios. You don’t have to be terribly bearish to conclude that that is a position from which markets will continue to discount risk so your capital may well continue to erode even as payouts erode. I mean, seriously, does this look like a well-balanced economy to you, from Goldman:

If you are more sensibly bearish given the point of the cycle then you should be considering when to short these sitting ducks not get more long.