The Australian Treasury has confirmed that reform of the superannuation concession system is well and truly on the agenda, revealing that it is examining implementing the Henry Tax Review’s recommendations to tax superannuation contributions at a progressive but concessional rate of 20%. From The AFR:

Superannuation contributions would be taxed at 20 percentage points below each individual’s marginal income tax rate under a plan being considered by the Coalition…

Treasury officials have told a range of industry players that the 20 per cent formula would be “revenue neutral”, which means it wouldn’t raise additional tax to be used to help repair the budget or reduce other taxes…

This would also allow the government to argue it was reducing effective tax rates on superannuation for millions of ordinary workers on the 32.5 per cent marginal tax rate, potentially allowing them to save more for their retirement and rely less on future pension payments…

The idea of overall revenue neutrality rather than increasing taxes would make it easier to limit superannuation industry complaints about the risks of more “tinkering” with the system.

Separately, The Australian is reporting that the Australian Treasury is also examining imposing a lifetime cap on superannuation savings, whereby tax concessions would be removed for amounts over the threshold:

The Association of Superannuation Funds of Australia has suggested a lifetime cap of $2.5 million for every super fund… The Australian has learned that Treasury officials have rejected this concept and are instead examining the idea of a cap on the amount that can be put into a super fund over time.

Applying a new benchmark to the future contributions over a worker’s career is favoured within the government because it has no retrospective impact on the money already saved.

There is no proposal so far on the value of the threshold, amid furious disputes over how much is needed to fund a comfortable retirement…

ASFA research shows about 24,000 of the richest account holders, each with more than $2m in their accounts, receive about $5.2bn in tax-free income every year.

The option favoured by the government would not change the treatment of those existing funds but would seek to impose a fairer tax scale for future contributions.

It is great to see the discussion on superannuation reform shift from “whether it should be done” to “how it should be done”, with all sides of politics seemingly now on the side of reform.

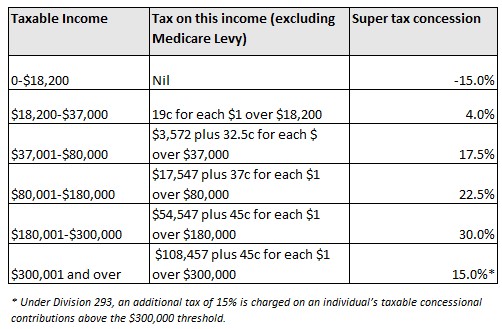

As illustrated countless times before, the current superannuation concession system is hugely inequitable because the amount of tax concession received grows as one moves up the income tax scale. For example, a very low income earner earning up to $18,200 effectively pays 15% on their superannuation contributions, whereas a high income earner earning $300,000 receives a 30% tax benefit (see below table).

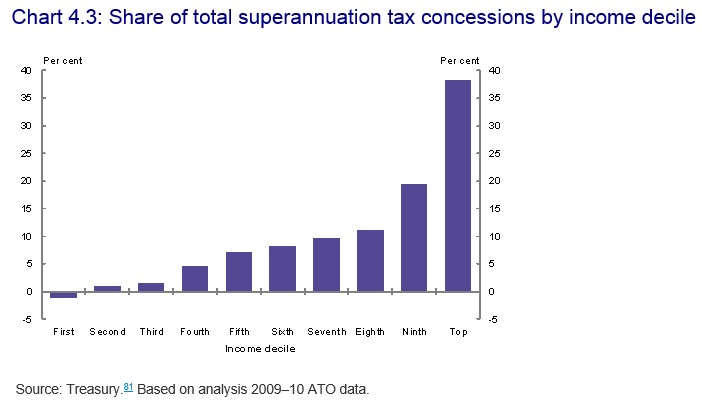

This system has led to a situation whereby the lion’s share of concessions flow to high income earners, while the poorest workers are penalised, thereby reducing the progressiveness of the tax system and blowing a big hole in the Budget (see next chart).

In this regard, the Australian Treasury’s proposal to tax superannuation contributions at a progressive but concessional rate of 20% is a marked improvement, as is the implementation of a lifetime cap.

That said, I am surprised that the Treasury has backed a concession rate of 20% rather than Deloitte’s (and my) proposal of 15%. A 20% concession rate would be revenue neutral, whereas a 15% rate would save the Budget some $6 billion per year. Given that the Budget is in structural deficit, and this is likely to get worse as the population ages, I would have thought that raising an additional $6 billion via superannuation concession reform is appropriate.

Certainly, bringing the Budget back into balance via revenue increases is more desirable than slashing services to Australia’s most vulnerable citizens.

unconventionaleconomist@hotmail.com