By Alpha Beta Strategy and Economics, republished with permission

One size doesn’t fit all

Imagine that instead of the Reserve Bank of Australia setting a single interest rate for the whole country, each state could set its own rate based on local economic conditions. Think of a ‘Reserve Bank of NSW’ located somewhere on Macquarie Street setting interest rates for New South Wales, a ‘Reserve Bank of Victoria’ on Collins Street applying a different interest rate below the Murray, and so on for every state across the country.

This scenario is impossible to achieve in practice (each state would need its own currency), but it’s thought-provoking to calculate what the interest rate would be if set by separate central banks in each state.

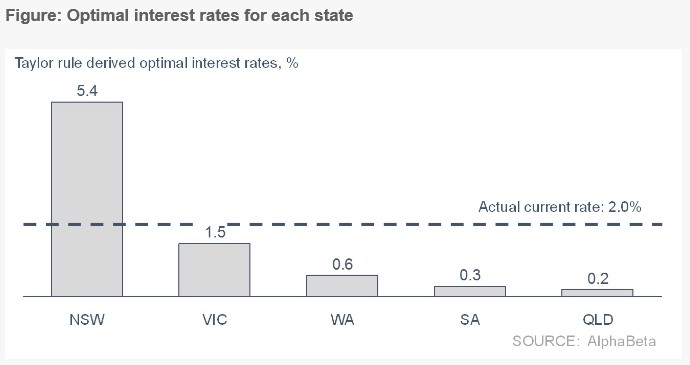

Using a simple Taylor Rule*, we calculate that the ‘Reserve Bank of NSW’ would be setting an interest rate of around 5.4% reflecting its strong economic growth and higher than average inflation, while the Reserve Banks of Queensland, South Australia and Western Australia would all be setting interest rates below 1%, reflecting the need to stimulate their flagging economies.

This figure shows the dilemma facing the RBA this week. Glenn Stevens must set an interest rate for the whole country, but each state actually requires very different monetary policy to reflect very different economic conditions.

This means that strong states are enjoying lower interest rates than necessary and weaker states are being slugged with interest rates that area too high to boost growth. For example, NSW is receiving a huge and unnecessary monetary policy stimulus of around 3.4 percentage points. On the other hand, Queensland should have interest rates at 0.2% but actually has them at 2.0%, so monetary policy in the Sunshine State is potentially 1.8 percentage points too tight.

Of course, this is not the first time Australia has faced regional economic disparities. But the size of the state variation is unusual today, caused by the sharp drop in resources prices currently punishing the mining states.

NSW is being overstimulated

The NSW economy today is being overstimulated by excessively low interest rates designed to support the mining states. On a stand-alone basis, current economic conditions in NSW warrant much higher interest rates (5.4%) than the RBA is currently setting for the whole economy (2.0%).

This goes a long way towards explaining the forest of cranes across the Sydney skyline, the roaring house price appreciation, the rivers of stamp duty flowing into the state budget and strong consumer spending.

But these boom conditions might be a case of short-term gain that risks long-term pain. Asset bubbles and construction booms can create imbalances that must ultimately be unwound over the longer term.

What does this mean for business?

Businesses need to think beyond the short term when planning their investment decisions. Just because a state is booming today, doesn’t mean those conditions are sustainable, especially if part of the boom is being caused by artificial monetary stimulus.

Over the longer term, booms caused by excessively loose monetary policy can lead to instability and slower growth. NSW may ultimately face a period of flat (if not falling) house prices, softer construction activity and slowing consumer spending. The eventual slowdown will be all the more severe thanks to the artificial ‘sugar hit’ of low interest rates. And when the slowdown begins, the RBA may not be in a position to cut interest rates (because rates are already very low), and if anything, may need to raise interest rates as the weak mining states begin to emerge from their trough.

Of course, different industries will be impacted in different ways as this cycle unfolds (click for more information).

What does this mean for governments?

Of course, the problem of one-size-fits-all monetary policy is not unique to Australia. In the United States, economic conditions have frequently differed dramatically across regions. The Federal Reserve does not set different monetary policies for different parts of the country. Similarly, the European Central Bank sets monetary policy for nations as diverse as Germany and Greece.

Governments should work to ensure that their non-monetary policy levers contribute to rebalancing divergent regional economies. In Australia the Commonwealth government should use the budget to help to smooth regional economic shocks. And it must work to improve inter-state mobility of labour and capital by harmonising regulation and reducing barriers to inter-state movement of workers.

The implication for state governments is that they must play a more active role in the economy. In particular state governments should consider leaning against the wind of monetary policy: if monetary policy is too lax (as it may be in NSW) then the NSW government should consider countercyclical policies to ensure that growth is sustainable.