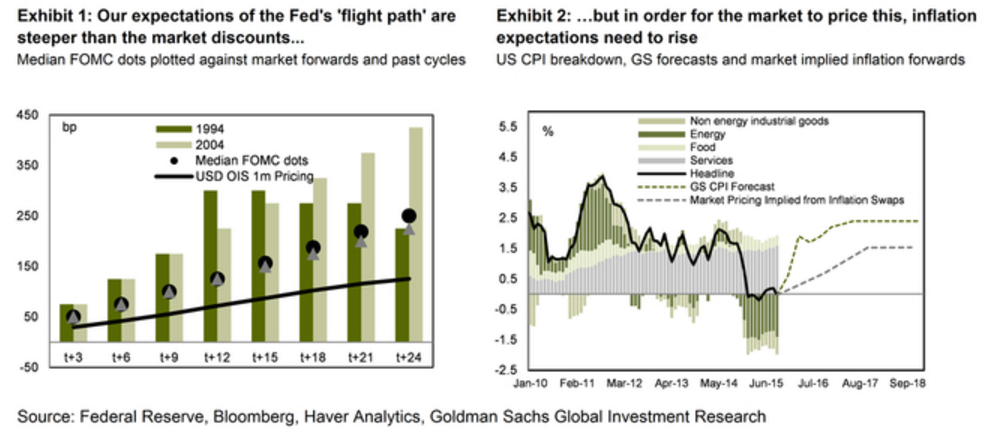

The market discounts that the Fed Funds rate will be at around 85bp by December 2016, implying an additional two hikes in the next calendar year. More interestingly, the forwards discount that in 2017 the pace of rate hikes will slow to a cumulative 50-75bp, leaving policy rates just below 1.5% by December 2017.

Our US Economics team’s modal forecast calls for 100bp cumulative hikes during 2016 (Fed Funds would end the year at 1.4%) and a further 100bp tightening during 2017 (at the end of which Fed Funds would stand at 2.4%). The gap between our baseline projections and the forwards grows over time (around 40bp at end-2016, 80-90bp at end-2017, over 100bp by end-2018, as shown in Exhibit 1).

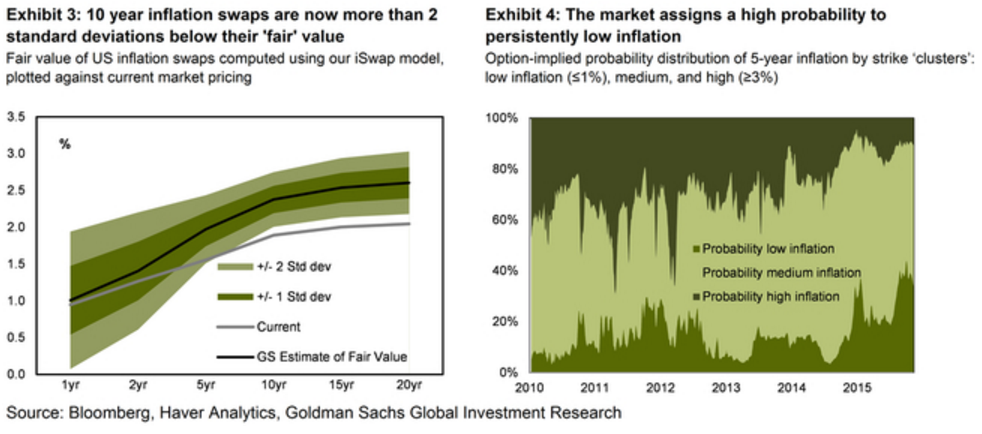

One of the main reasons why we see a higher trajectory for policy rates is that, with the economy expected to continue to expand faster than its 1.75% potential rate of growth, pressures on wages and core inflation (particularly in services components) will build, as illustrated in Exhibit 2. The market, however, does not appear to be pricing this.

Core CPI inflation is already trailing just below 2% at an annual rate, with the persistent price dynamics in service ex-energy category contributing 210bp to the readings. Yet, US inflation swaps price annual inflation rate at around 1.0% by December 2016, climbing to 1.6% in both December 2017 and 2018.

Based on the current forward curve for crude oil, this tells us that the market is either pricing that underlying core inflation will decelerate or that the distribution of risks around the inflation outlook is skewed to the downside. The inflation option market would support the latter interpretation: the market currently assigns around a 35% probability to a scenario in which US CPI inflation averages less than 1% over the next 5 years.

In both cases, the market prices that policy rates will at best hover close to zero in real terms over the coming three years. If we take our US Economics team’s projections for headline CPI over these same horizons, which are 60-80bp above the inflation forwards, and subtract them from the market-implied path for Fed Funds, real policy rates are set to be negative to the tune of 80-100bp by end-2017.

Given where the US economy is now and where we think it is heading, we find it hard to believe that real policy rates will be zero in two years’ time, let alone negative 1%.

Your basic Phillips Curve jibber jabber and wrong:

the last thing the Fed wants to do is squash a little belated income growth for households;

it won’t pass through to inflation expectations anyway given still large shadow labour market slack and broader commodity deflation, and

a couple of rate hikes will be enough to push the US dollar so high that the commodity deflation pulse will develop into a crisis for EMs, threatening global debt market volatility and the US stock market.

There may be more US rate hikes after December but they will be paced to manage the above triptych of risks, just as they have so far.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.