We’re off to the races again, it seems, with the S&P500 launching 1.6% last nigth. There were all sorts of triggers none of which seems to be directly responsible, but that’s what we got:

- superficially good Chinese lending data, though actually still trending down;

- whispers of further ECBQE, which is also bad given it puts upwards pressure on the US dollar;

- weak Empire and Philly Fed indexes could point to delayed Fed hikes;

- a stronger than expected US inflation print with a core reading up slightly to 1.2% suggesting the Fed could hike, and

- oil up on falling US production despite a massive inventory build.

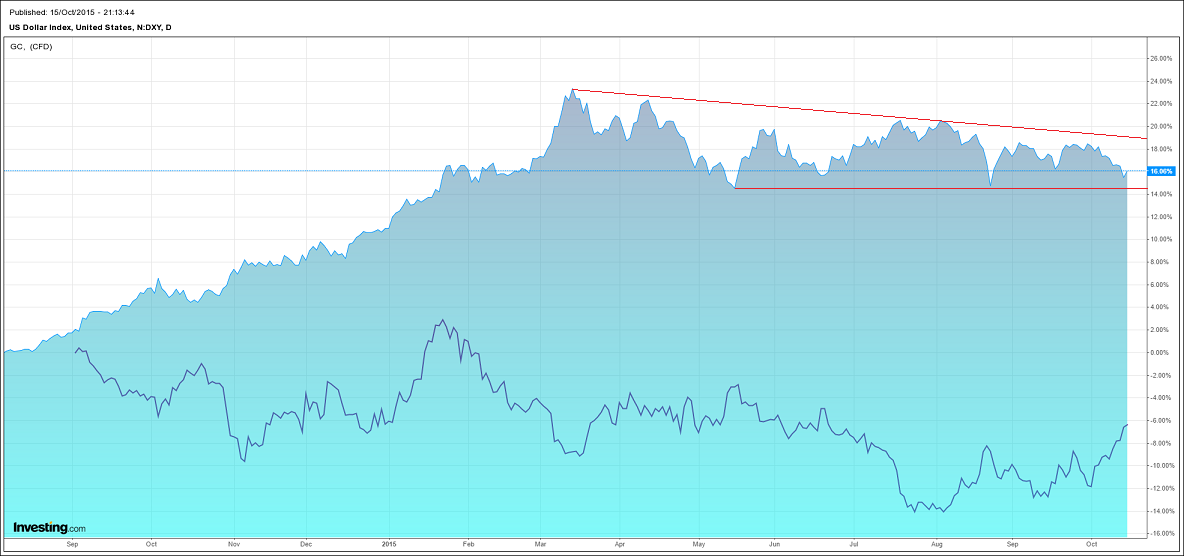

If you can find a reason for runaway stocks in there then you’re a better man than I am. Perhaps it’s still buying from yesterday’s weak US retail report as markets digest a longer Fed pause. But bonds were flogged and the US dollar firmed. Even so, the driving force is likely still Fed pauses which are threatening to derail the US dollar rally. Here is the Dollar Index versus gold:

The index has a bearish descending triangle pattern forming and if it breaks lower that will lift all risk markets while is lasts.

If that’s the cyclical set up, there is also the secular trend consider and the following video does a good job of telling you what is still coming down the longer term pipe in my view: