From Fairfax:

RBC Capital Markets has raised its call to outperform.

JPMorgan more than halved its target for Origin shares, to $6.40 from $13, after cutting earnings estimates as a result of lower oil price assumptions. It kept its recommendation at overweight.

The planned issue of 636 million new shares at $4 apiece means earnings per share estimates have been cut more severely.

UBS reduced its 12-month price target for Origin shares to $6.57 from $9.67, while retaining a buy call. UBS analyst David Leitch told clients that he expected Origin to trade at a 23 per cent discount to its peers amid a lack of confidence in the company after several written-off investments in power generation and the change of tack on the need for a capital raising.

UBC analyst Paul Johnston also slashed his price target for Origin, to $6.50 from $10, but pointed to “significant upside from these depressed levels” given guidance for earnings given by the company on Wednesday for the next two financial years.

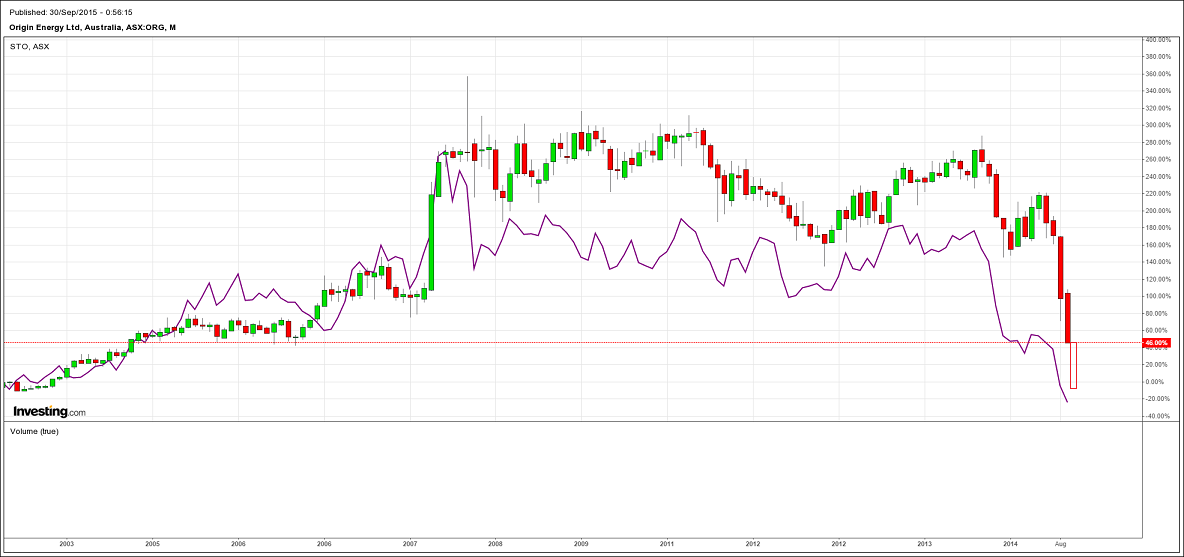

Having missed the entire bubble then bust with absurd price targets:

We’re supposed to listen now?

The MB position on the commodity sector is unchanged. The percentage play is building shorts on rallies and awaiting the great final cleansing that could very well cost Origin its life.