Slower growth in China and a downturn in the mainland property market have seen falling demand for iron ore, as might be expected. However, demand for Australian iron ore has continued to rise. The reason is that Australia is the lowest cost producer in the global market. Australian iron ore export volumes to China have risen by 8% y-o-y, while China has cut back on its own higher cost domestic production, which has fallen 8% y-o-y. Steady demand for higher grade/lower cost iron ore, largely from Australia, has seen the iron ore price remain steady at around USD50-60 a tonne for the past three months. We are forecasting the iron ore price to remain around this level over the next year or so. Although the overall iron ore story is a challenging one, Australia is faring reasonably well.

Falling commodity prices have taken their toll on a range of commodity-producing countries, with GDP declining in Canada, Brazil, Russia and South Africa in recent quarters. The Australian story has, so far, been a bit different, with GDP continuing to rise. A large part of this reflects that growth in Australia has been rebalancing towards the housing and services sectors, in response to looser financial conditions (we have written about this extensively, see: ‘Australia’s next growth driver: the rise of the services sector’, 10 July 2015).

But Australia’s commodity story is also a bit different to some other nations. One factor at work is that Australia is the lowest cost producer for many of the commodities it produces. This is in contrast, for example, to the oil story in Canada, where tar sands oil production is further up the cost curve and the large Middle East producers are at the bottom end of the cost curve.

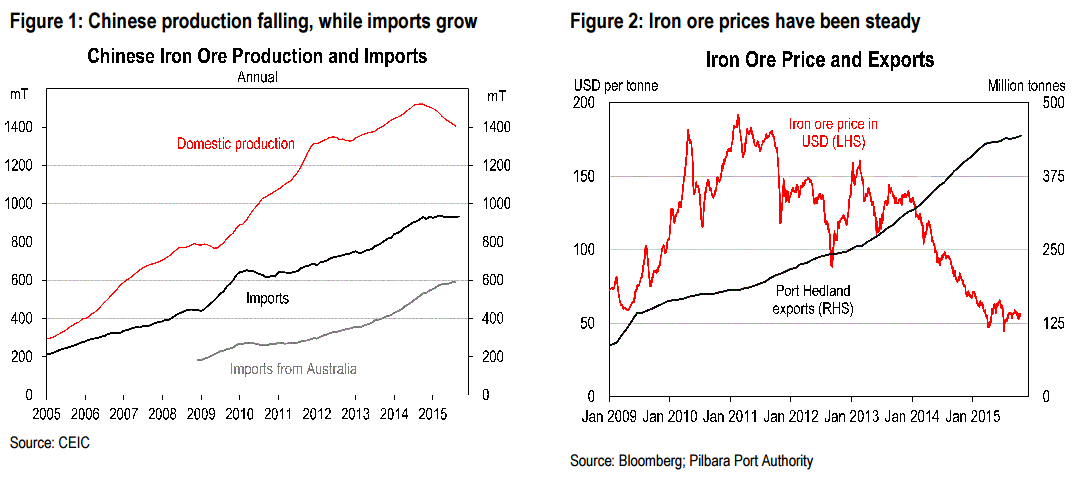

Most importantly, Australia is the lowest cost producer of iron ore, which is its single largest export, accounting for 17% of total exports (by volume). Being the lowest cost producer has meant that demand for Australian iron ore has continued to rise while other producers have been forced to cut back.

Australia produces around 55% of globally traded iron ore and over 90% of Australia’s iron ore is produced at a cost that is below the current spot price of USD55 a tonne. By comparison, China produces around 20% of global iron ore, but the cost of production is estimated to be between USD80-110 a tonne. As the iron ore price has fallen, China has cut back on its own production, but has continued to buy more from Australia (Chart 1 and 2). Port inventory numbers from China have also fallen over the past year, suggesting that the imported iron ore is being used rather than stock-piled.

Although the overall iron ore story is a challenging one, the trends are generally quite positive for Australia. If China continues to cut back its own production, in favour of lower-cost Australian iron ore imports, then Australia should continue to gain market share. These trends should also help to support the iron ore price even in the face of more iron ore mines coming on-line and ramping up their production in coming months. We are forecasting the iron ore price to remain broadly steady, averaging USD58 in 2015 and USD52 in 2016.

All so maddeningly orthodox. No understanding that it is the income that matters not the volumes. No understanding that the production ramp up in volumes will continue to destroy the income. No understanding that that income is the principal support to the services economy “rebalancing” that he so champions.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.