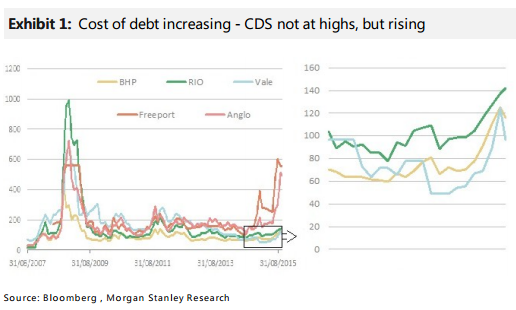

Rising CDS spreads point to balance sheets coming into focus: A recent creep in Credit Default Swaps (CDS) spreads for the miners is indicating an increased focus by the debt markets on the balance sheet for miners, quality of earnings and cash flow viability. We note a near doubling (up 83%, 142bps to 261bps) in the average CDS spreads for the chosen 6 major miners in the past year. Focusing on the 3 major iron ore miners, the average CDS Spreads are up ~50% (75bps to 112bps) over the same period. Although liquidity in CDS markets can drive spreads, the main factors are company and industry fundamentals, suggesting the debt market has a concerns about earnings sustainability.

A rising cost of debt for miners may impact bottom line and cash flow: Although the CDS spreads are far below those experienced during the 2008 Financial Crisis (seeExhibit 1) for RIO, BHP and Vale, the average cost of debt is rising. This can contribute to be a bottom line and cash flow impact when debt is replaced. The upside of a reduction in the availability of “cheap debt” should be more disciplined capital allocation through the industry – we consider this a positive outcome given oversupply in most commodities.

As commodity prices keep falling I expect this and emerging market debt to become the key shakeout driving the next global recession.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.