From the AFR:

Ben Silluzio, the chief investment officer and CEO of start-up investment firm, Qato Capital, thinks shares in BHP Billiton could fall 30 per cent by the time the mining giant reports its half-year results in February.

Mr Silluzio arrived at this view on the basis of its “Q-Score”– its proprietary named output of an algorithm he designed to rank and invest in companies.

…While fundamental analysis formed the basis of the Q-Score – inputs such as changing return on equity, earnings per share growth, free cash flow forecasts and the like – its “secret sauce” is derived from its ability to model market behaviour as those fundamentals shift, Mr Silluzio explained.

“Australia is in love with BHP. When we look at numbers we see a company with increasing debt, a dividend that if they earn what they are forecast to earn they won’t be able to pay, and ratings agencies breathing down their neck if they decide to raise debt,” Mr Silluzio said.

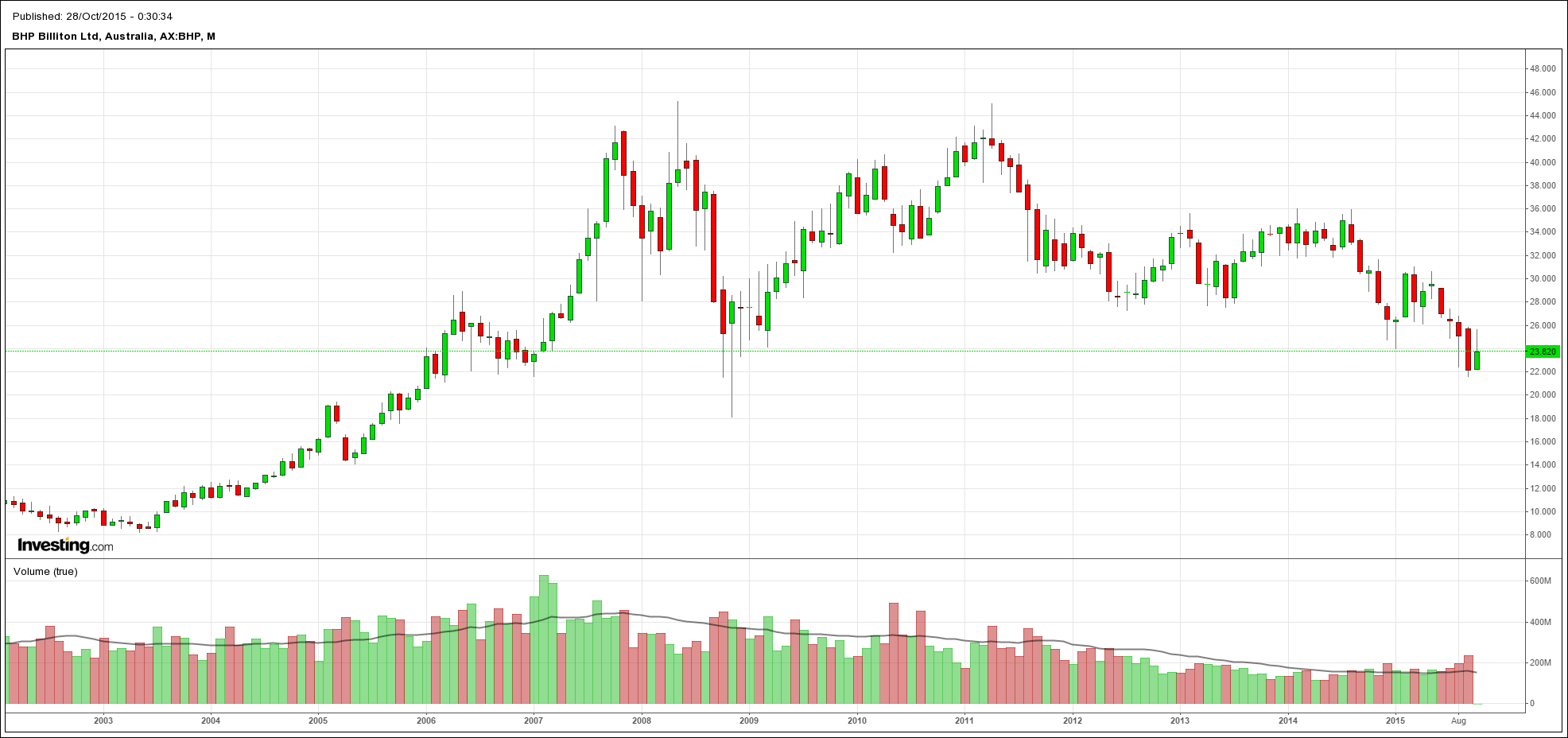

My own target for BHP is a return to the 2003 price under $10 though not in the next three months:

I arrive at that conclusion given:

- iron ore is headed back into the $20s;

- oil is going to take years to shakeout and won’t get back above $60;

- the dividend is going to be cut;

- after years of price erosion I expect the big Australian will crash during the end of cycle accident, and

- sentiment is going to get so deeply depressed around commodity stocks that you couldn’t give them away.

Super cycle=super bust.