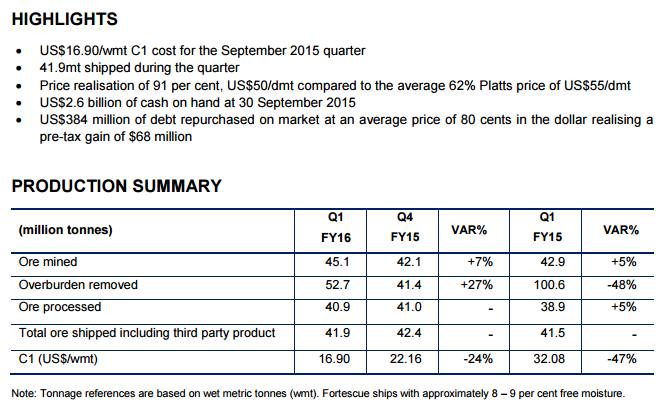

Fortescue is out with its third quarter production report and it’s a barn burner:

That’s well ahead of $18wmt cost per tonne guidance, is on tack with volume, is a 4% improvement on discounting for its sub-par ore, a $200 million rise in cash on hand and it bought back $384 million in debt for a profit. That is a blue chip quarter.

It’s a real shame that this business is doomed.

Advertisement