Cross-posted from the comic genius The Idiot Tax.

Just over six months ago, up a Sydney alley way that looked like a urine thoroughfare, a young man named Doi bought his first house. Over the next few days the internet gasped with horror. Doi, assisted by mother, Gina, paid 840k at auction. 140k over the reserve to secure what he termed at the time “a beautiful little house.” Online real estate listing site Domain termed it “derelict”. Anonymous internet respondents screamed “shithole”. And those were the diplomatic assessments.

You be the judge.

It was 63 square metres of the Australian dream. 1 bedroom and an external laundry plus crapper. Yep, drink one too many beers during a storm and you’d need to pee in the kitchen sink. As the agent said, “The kitchen along with the combined living & dining area are the neater parts of the home but ready for the next transformation. Joining the laundry bathroom to the home is a cute but quaint central paved courtyard.” A fixer upper, you could say.

Externally it looked like this.

Yesterday Doi and Gina were back at 7 Little Bloomfield Street, Surry Hills. Their fingers crossed for greater fools because Doi was keen to offload his March purchase. The reason? Like most of us who’ve bought $800k crack shacks, Doi had a healthy dose of buyers’ regret and came to his senses“after realising just how small the property was he decided to sell.”How lucky was Doi? This is Australia! Doi found a plumber willing to go 60k higher than he’d paid six months earlier. Below the auction reserve, but supposedly covering Doi’s arse.

The $900,000 sale price was cause for relief, not celebration. After paying $840,000 Mr Kim spent $34,000 on stamp duty, $6500 on obtaining development approval to add another level, $3000 on painting . He also had other rates and fees. “I broke even,” he said after the auction.

A 2% sales commission meant Doi likely would have lost a few bucks, but that’s neither here nor there under the circumstances.

With backing from his mother, Gina Lim, he has since bought a larger terrace around the corner on Crown Street.

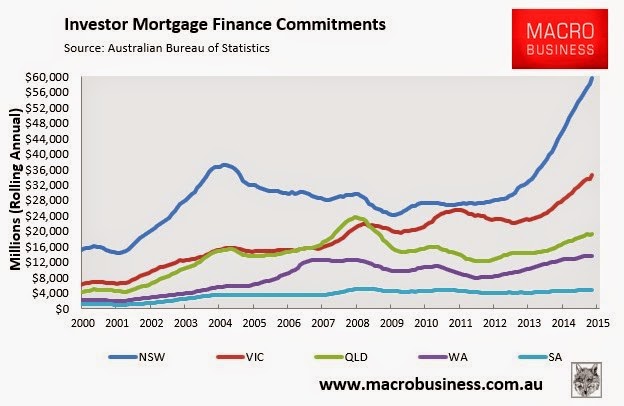

As noted back in March, the orgy that has drawn in momma’s boys and plumbers, while leaving the rational scratching their heads, can be laid at the feet of Australia’s financial regulators. Sydney property prices ripped upwards 14% in 2013 and another 12% in 2014, after the Reserve Bank cut interest rates 1.25% in 2012 and another 0.5% in 2013. In February this year, the RBA saw fit to cut another 0.25% into this lunacy without any lending restrictions in place, the result was another 12.6% gain in Sydney prices by July 30, 2015.

But this was totally cool because in their words, “the Bank is working with other regulators to assess and contain economic risks that may arise from the housing market.” Back then all we knew of Australia’s mortgage regulation was by December 2014 APRA or the Australian Prudential Regulation Authority had used all of their authority to write Australia’s banks a letter.

While plumbers might be unaware as yet, some lending standards and bank capital requirements are finally being implemented. Only years too late. This week we found out from APRA head buffoon, Wayne Byers, that APRA was either asleep at the wheel or a financial terror organisation that had for years recklessly ignored Australia’s mortgage standards, turning parts of Australia’s real estate market into a speculative casino for highly leveraged property investors.

The banking regulator has criticised the mortgage lending standards some banks had in place before it stepped up scrutiny of the sector earlier in 2015, saying some standards had fallen to “horribly low levels” that lacked “common sense”. The chairman of the Australian Prudential Regulation Authority, Wayne Byres, also conceded that the regulator would have liked to uncover the poor lending standards earlier than it did.

APRA’s partner in crime, the RBA, after a four year interest rate slice and dice, also finally figured out that cheap money with little regulation in place has unintended consequences. Namely sleazeballs shoveling money out the door to maniacs who have no hesitation borrowing nearly 100% on interest only terms to lose rental money so they can speculate on housing capital gains.

The Reserve Bank of Australia has cracked the whip at banks, saying their lending standards have not been sufficiently robust and that as a result the mortgage market presents a “higher than average risk” to the stability of Australia’s financial system.

In an unusually tersely worded bi-annual financial stability review, the RBA said investigations by regulators revealed lending standards had been weaker than thought and in some cases breached prudential standards. Several banks had under-reported the amount of lending to property lenders and in some cases banks had breached consumer lending laws aimed at ensuring people only borrow as much as they can afford. “In particular, poor documentation and verification by lenders in many instances suggests that some borrowers may have been given interest-only loans that were not suitable for them,” the RBA said.

Yeah, you know that douche in your Facebook friends list who was talking about buying a house and bragged he used his credit card to front the deposit. It was probably true. Significant interest rate cuts that provoked a viagra like response in investor lending didn’t raise any concerns from APRA for several years.

And while the crackdown has come, banks raising capital, some expecting higher deposits, many independently jacking interest rates, first on investors, then this week across the board a second time on all borrowers, APRA is left sheepishly kicking the dust around the stable door while the RBA wonders if the horse will come home of its own volition. That’s what the RBA calls, “working with other regulators to assess and contain economic risks that may arise from the housing market.”As macrobusiness, who’ve been calling for macroprudential policies for the past four years so this situation might be avoided, put it:

It is APRA’s job to be “interventionist” and prudently manage risk. This necessarily involves preventative policies rather than the types of reactive policies we are experiencing currently, which are inherently pro-cyclical and risk exacerbating the downside as the Great Australian Housing Bubble bursts.

Finally, the speculative incentive that turbo charged this whole mess, negative gearing, was given a kick this week. Australian politicians usually line up to defend the madness of investors putting as little down as possible, taking an interest only mortgage because rent still won’t cover their costs and claiming a tax deduction on that loss at the end of the financial year with the eventual hope that capital gains make up for those rental losses, but not this week. Like all brave heart Australian politicians, future ambassador to the US, Joe Hockey lined up to hit negative gearing when the word “former” became part of his official title. Former Treasurer, Joe Hockey:

In that framework, negative gearing should be skewed towards new housing so that there is an incentive to add to the housing stock rather than an incentive to speculate on existing property

Echoing the words of most unconflicted or half-way intelligent people. Shamefully, Hockey, a fat bastard who had 70% of his stomach removed to lose weight instead of walk around the block, spent years defending and lying about negative gearing. Scaremongering multiple times on the potential impact on rents were it removed, and consistently asserting that negative gearing was primarily usedby middle income earners when the top the top 40% of income earners held nearly 80% of all investor mortgage debt.

With the ability to regularly lie through his teeth then completely change his tune when he longer needed to shill for votes, Joe should be right at home in Washington. Importantly he won’t be around to sweat bullets when the whole thing comes apart.

The final word to Doi, who has noticed belated regulation has caught up to Sydney’s real estate market four years too late.

When asked if he could go back six months would he do it all again he promptly responded “no”. “The market is getting too slow,” he said.

And thank god for plumbers.